|

|

|

|

|||||

|

|

|

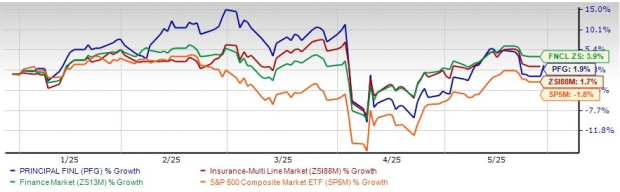

Shares of Principal Financial Group, Inc. PFG have gained 1.9% in the year-to-date (YTD) period, outperforming the industry’s growth of 1.7% and the S&P 500 composite’s decline of 1.8%. It, however, underperformed the Finance sector’s return of 3.9% in the YTD period.

This multi-line insurer has been trading above its 50-day simple moving average (SMA), signaling a short-term bullish trend. Its share price, as of May 27, 2025, was $78.89, down 14.2% from its 52-week high of $91.98.

The 50-day SMA is a key indicator for traders and analysts to identify support and resistance levels. It is considered particularly important as this is the first marker of an uptrend or downtrend.

With a market capitalization of $17.68 billion, the average volume of shares traded in the last three months was 1.5 million.

The insurer’s shares are trading at a price-to-earnings multiple of 9.34, higher than the industry average of 8.74. Also, it has a Value Score of A.

PFG is also expensive compared with Enact Holdings, Inc. ACT, MGIC Investment Corporation MTG and Radian Group Inc. RDN.

The Zacks Consensus Estimate for Principal Financial’s 2025 earnings per share indicates a year-over-year increase of 15.6%. The consensus estimate for revenues is pegged at $16.19 billion, implying a year-over-year improvement of 3.5%.

The consensus estimate for 2026 earnings per share and revenues indicates an increase of 11.8% and 4.3%, respectively, from the corresponding 2025 estimates.

Principal Financial’s revenue growth is expected to improve in the long run, riding on higher premiums and other considerations, fees and other revenues, and improved net investment income across its segments.

Principal Financial continues to benefit from its strength and leadership in retirement and long-term savings, group benefits and protection in the United States, retirement and long-term savings in Latin America and Asia plus global asset management, which help it deliver solid operating earnings.

PFG estimates solid revenue growth as well as margin expansion across all its segments over the long term.

The Specialty Benefits Insurance business should continue to gain from record sales, strong retention and employment growth. Growth in the business, favorable claims and disciplined expense management should benefit its pre-tax operating earnings.

Strong institutional flows across equities, real estate and specialty fixed income, highlighting the value of diversified distribution through its institutional, retail and retirement channels, are likely to drive positive net cash flow.

Principal Financial’s extensive distribution footprint, strategic buyouts and operational discipline should enhance the assets under management growth.

PFG boasts a strong capital position, with sufficient cash generation capabilities and liquidity. To reflect the business mix and risk profile, PFG revised the RBC target to a range of 375% to 400%. For 2025, PFG remains well-positioned to deliver on enterprise long-term financial targets, with 9% to 12% growth in earnings per share and 75% to 85% free capital flow conversion.

Principal Financial’s wealth distribution through share buybacks and dividend payments looks impressive. In the second quarter of 2025, PFG raised the dividend for the seventh consecutive quarter, aligned with the targeted 40% dividend payout ratio and demonstrated confidence in continued growth and overall performance. It was a 7% increase over a year-ago quarter and a 9% rise for the full year. It also boasts a solid dividend yield of 3.4%, higher than the industry average of 2%. The insurer continues to expect to deliver on the targeted 75% to 85% free capital flow for 2025.

PFG targets $1.4 billion to $1.7 billion of capital deployments in 2025. It intends to spend 35-45% of its net income on share buybacks and about 10% on strategic M&A activities to enhance capabilities and support organic growth.

Principal Financial's financial stability and favorable growth estimates bode well for growth. PFG should benefit from strategic buyouts, strong retention, higher single premium annuity sales, effective capital deployment and positive net cash flow.

Given the premium valuation, investors should wait for a better entry point for this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-03 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite