|

|

|

|

|||||

|

|

|

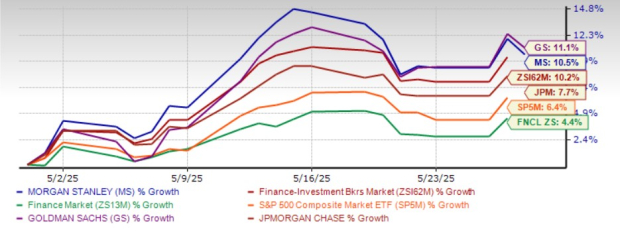

Over the past month, shares of Morgan Stanley MS, a leading global investment bank, have risen 10.5%. The stock has outperformed the S&P 500 index, the Zacks Finance sector and the industry. Meanwhile, it has underperformed its close peer, Goldman Sachs GS, while outperforming JPMorgan JPM.

Morgan Stanley’s One-Month Price Performance

However, lingering uncertainty around tariff policies continues to pose risks. Given this backdrop, let’s assess whether Morgan Stanley stock is a lucrative bet or not.

Entering 2025, a major rebound in mergers and acquisitions (M&As) was expected, with deal-making activities likely to grow in the mid-20s. This optimism stemmed from pent-up demand, stabilizing or declining interest rates, tightening credit spreads, and strong public market valuations. Also, the Trump administration was regarded as more business-friendly, with an expected rollback of stringent oversight that could mark the end of the prolonged regulatory scrutiny.

None of these has transpired till now. Deal-making activities have been muted as ambiguity over the tariff and ensuing trade war has resulted in extreme market volatility. These developments have led to economic uncertainty, data indicating a slowdown/recession in the U.S. economy, and rising inflationary pressure. Amid such a backdrop, companies are rethinking their M&A plans despite stabilizing rates and having significant investible capital.

The Morgan Stanley management expects M&A and underwriting activities to pick up in the second half of 2025, impacting its M&A advisory fees in the near term. Further, the delay in M&A rebound will impact other IB firms, including JPMorgan and Goldman Sachs, which generate billions in revenues from M&A advisory fees.

MS has lowered its reliance on capital markets for income generation. The company’s focus on expanding its wealth and asset management operations and strategic acquisitions, including Eaton Vance, E*Trade Financial, and Shareworks, is a step in that direction. These moves have bolstered its diversification efforts, enhanced stability and created a more balanced revenue stream across market cycles. Both businesses’ aggregate contribution to net revenues jumped to more than 55% in 2024 from 26% in 2010. For the first quarter of 2025, the aggregate contribution to net revenues was 50.3%.

In the first quarter, Morgan Stanley witnessed net outflows of $13.6 billion in the Investment Management division because of volatile markets. On the other hand, assets under management or supervision grew 9.4% year over year to $1.6 trillion as of March 31, 2025. Further, the Wealth Management division’s total client assets rose 9.5% on a year-over-year basis to $6 billion.

Morgan Stanley’s partnership with Mitsubishi UFJ Financial Group, Inc. MUFG is expected to continue supporting its financials. In 2023, the companies announced plans to deepen their 15-year alliance by merging certain operations within their Japanese brokerage joint ventures.

The new strategic alliance involves combined Japanese equity research, sales and execution services for institutional clients at Mitsubishi UFJ Morgan Stanley Securities and Morgan Stanley MUFG Securities. Also, their equity underwriting business has been rearranged between the two brokerage units. These efforts will solidify the company’s position in the lucrative Japanese market.

This helped MS to achieve record equity net revenues in the first quarter of 2025, particularly in Asia, through outperformance in prime brokerage and derivatives driven by solid client activity amid heightened volatility. Further, the company’s Asia region revenues jumped 34.5% year over year to $2.35 billion during the quarter.

As of March 31, 2025, Morgan Stanley had a long-term debt of $297 billion, with only approximately $23 billion expected to mature over the next 12 months. The company’s average liquidity resources were $351.7 billion as of the same date.

Moreover, the company enjoys investment-grade long-term credit ratings of A1, A-, and A+ from Moody’s, S&P Global Ratings, and Fitch Ratings, respectively, and a stable outlook allows easy access to the debt market. Thus, a solid balance sheet position supports its enhanced capital distributions.

Following the 2024 stress test results, the company announced an increase in its quarterly dividend by 8.8% to 92.5 cents per share

.

The company also reauthorized a new multi-year share repurchase program of up to $20 billion, effective the third quarter of 2024 and with no expiration date. As of March 31, 2025, approximately $17.5 billion worth of shares remained available under the authorization.

Over the past month, the Zacks Consensus Estimate for 2025 earnings has been revised marginally downward to $8.58. Nonetheless, the consensus estimate for 2026 earnings has been revised marginally upward to $9.27.

Estimate Revision Trend

The Zacks Consensus Estimate for Morgan Stanley’s 2025 and 2026 earnings implies year-over-year growth of 7.9% and 8.1%, respectively. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

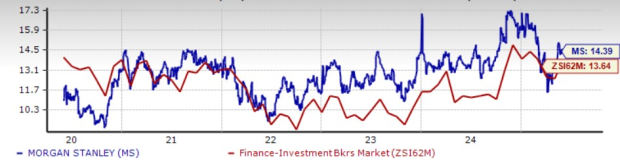

The MS stock is currently trading at a forward 12-month price/earnings (P/E) of 14.39X. This is above the industry’s 13.64X, reflecting a slightly stretched valuation.

Price-to-Earnings F12M

On the other hand, JPMorgan and Goldman Sachs have a forward P/E of 14.07X and 13.54X, respectively. This reflects that Morgan Stanley is expensive compared to its peers.

Morgan Stanley’s strong global presence and strategic focus on stable revenue streams provide a solid foundation for organic growth. Its diversified business model ensures resilience and growth potential, even in volatile market conditions. Resilient M&A pipelines and solid trading revenues are other positives.

However, the company has been witnessing a rise in expenses. Though expenses declined in 2022, the metric witnessed a five-year (ending 2024) CAGR of 7.8%. The rising trend continued in the first quarter of 2025. Expenses are likely to remain elevated given higher compensation costs, inflationary pressure and inorganic growth efforts.

Further, the likelihood of a significant IB rebound this year remains low amid concerns regarding tariff policies, making MS stock a cautious bet. Additionally, the stock’s premium valuation and mixed analyst sentiment warrant careful consideration before investing.

Current shareholders may benefit from holding for strong long-term returns, while potential investors should wait for greater macroeconomic clarity before taking a position.

Morgan Stanley currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite