|

|

|

|

|||||

|

|

|

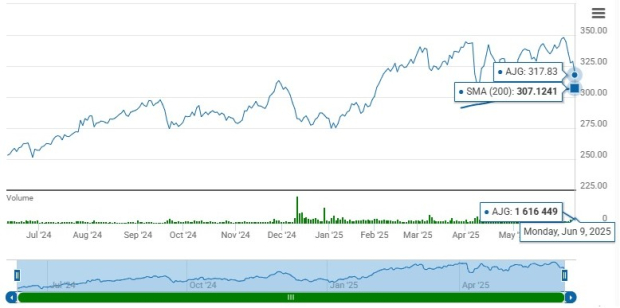

Shares of Arthur J. Gallagher & Co. AJG have gained 24.5% in the past year, outperforming its industry, the Finance sector and the Zacks S&P 500 composite’s return of 24.1%, 19.7% and 11.9%, respectively.

The insurer has a market capitalization of $81.38 billion. The average volume of shares traded in the last three months was 1.3 million.

Arthur J. Gallagher shares are trading well above the 200-day moving average, indicating a bullish trend.

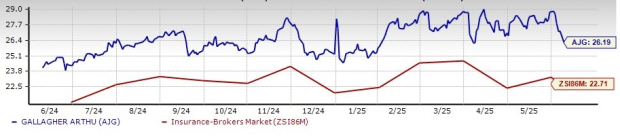

AJG shares are trading at a premium to the industry. Its price-to-book value of 26.19X is higher than the industry average of 22.71X. Shares of other insurers like Brown & Brown, Inc. BRO and Erie Indemnity Company ERIE are also trading at a multiple higher than the industry average, while Marsh & McLennan Companies, Inc. MMC is trading at a discount.

The Zacks Consensus Estimate for Arthur J. Gallagher’s 2025 earnings per share indicates a year-over-year increase of 9.4%. The consensus estimate for revenues is pegged at $13.75 billion, implying a year-over-year improvement of 20.9%. The consensus estimate for 2026 earnings per share and revenues indicates an increase of 22.5% and 22.9%, respectively, from the 2025 estimates.

Earnings of Arthur J. Gallagher grew 20.4% in the last five years, better than the industry average of 15.2%.

Arthur J. Gallagher’s bottom line surpassed earnings estimates in three of the last four quarters and matched in one, the average being 2.29%.

Five of the seven analysts covering the stock have lowered estimates for 2025, while three analysts have lowered the same for 2026 over the past 30 days.

The Zacks Consensus Estimate for 2025 earnings has moved down 1.2% in the past 30 days, while the same for 2026 has moved down 0.4% in the same time frame.

Based on short-term price targets offered by 15 analysts, the Zacks average price target is $345.00 per share. The average indicates a potential 4.9% upside from the last closing price.

Arthur J. Gallagher insurer remains focused on generating both organic (particularly international) and inorganic growth and is, thus, tapping into growth opportunities worldwide. This, coupled with solid retention and improving renewal premiums across all major geographies and most product lines, bodes well for growth.

Arthur J. Gallagher expects organic growth to improve in the second half of 2025 in the Risk Management segment. Looking forward, AJG expects 2025 adjusted EBITDAC margin to be 20.5%. It continues to expect the Brokerage segment’s organic growth in the range of 6% to 8% for 2025.

AJG’s revenues are geographically diversified with strong domestic and international operations. International contributes about one-third of revenues. Given the number and size of its non-U.S. acquisitions, AJG expects international contributions to its total revenues to trend upward.

Its inorganic growth story is impressive. Since Jan. 1, 2002, the company has acquired 761 companies so far. Revenue growth rates generally ranged from 5% to 17.5% for 2025 acquisitions. During the first quarter, AJG completed 11 new tuck-in mergers, representing around $100 million of estimated annualized revenues. Looking at the pipeline, AJG has more than 40 term sheets signed or being prepared, representing about $450 million of annualized revenues.

Banking on its capital position, AJG distributes wealth to shareholders through dividend hikes and share repurchases. In the first quarter of 2025, the dividend was raised by 8.3%, witnessing a six-year CAGR (2020-2025) of 7.6%.

However, Arthur J. Gallagher has been experiencing an increase in expenses due to higher compensation and operating expenses that have been eroding margins.

AJG continues to benefit from solid retention, improving renewal premiums, and organic and inorganic growth. The Risk Management and Brokerage segments should continue to witness significant growth. A robust capital position over the years reflects its financial flexibility. Its impressive dividend history, as well as solid growth projections, are other positives.

Given the escalating expenses, bearish analysts’ sentiment and premium valuation, it is better to stay cautious about this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-05 | |

| Aug-04 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite