|

|

|

|

|||||

|

|

|

DENTSPLY SIRONA XRAY is well-positioned for growth due to its new digital-implant workflowand continued focus on research and development. However, forex headwinds and demand softness in Europe remain a concern.

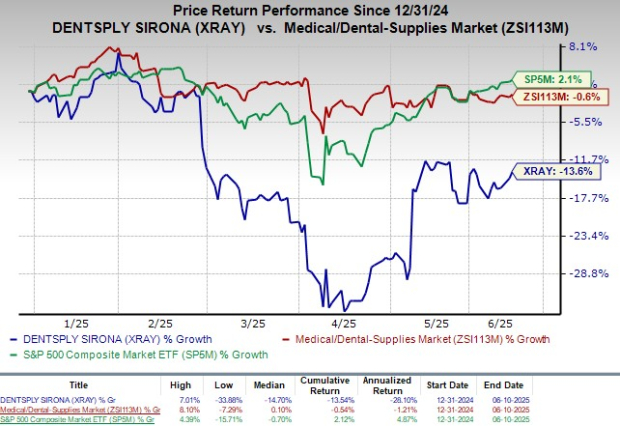

Shares of this Zacks Rank #2 (Buy) company have lost 13.6% year to date compared with the industry's 0.6% decline. The S&P 500 Index has gained 2.1% in the same time frame.

XRAY, with a market capitalization of $3.23 billion, is a global leader in the design, development, manufacturing and marketing of dental consumables, dental laboratory products, dental specialty products and consumable medical device products. It anticipates earnings to improve 7.4% over the next five years.

New Digital-Implant Workflow in Dentistry: DENTSPLY SIRONA's Azento solution is reshaping digital implant workflows by streamlining planning, purchase and delivery in single-tooth replacements, now also available in Canada and Europe. Backed by its strong X-ray, imaging and digital impression portfolio, the company is well-positioned in the growing $20 billion global tooth-replacement market. Demand is rising for 3D imaging and treatment centers, driven by tech upgrades and supply-chain recovery. DENTSPLY SIRONA’s rapid scale-up in clear aligners further strengthens its digital dentistry ecosystem.

R&D Boosts Product Innovation: DENTSPLY SIRONA’s overall growth strategy rests on product innovation. The company’s solid internal growth, despite challenging macroeconomic headwinds, is primarily driven by its innovative new products. XRAY pursues several R&D initiatives to support technological development. The company’s R&D has increased in 2024 as it is focused on delivering innovation and excellent solutions to customers.

In the first quarter of 2025, XRAY’s spending on R&D was $36 million. However, the momentum is anticipated to continue as 2025 progresses. This, in turn, will enable DENTSPLY SIRONA to focus on a more significant and sustainable innovation.

Decent Q1 Results: DENTSPLY SIRONA ended the first quarter of 2025 with better-than-expected results and bottom-line growth. The strength in the Wellspect Healthcare segment in the quarter was encouraging. The expansion of the adjusted operating margin bodes well for the stock.

Adjusted operating profit totaled $72 million, reflecting a 46.9% increase from the prior-year quarter. The adjusted operating margin in the first quarter expanded 305 bps to 8.2%.

Demand Softness in Europe: A softness in demand for CAD/CAM products in Europe, especially in Germany, has led to a decline in sales during 2024. Germany is the second-largest dental market in the world after the United States. The deterioration in demand for capital equipment and overall patient volumes is likely to continue in the next couple of quarters. A continued softness in demand does not bode well for DENTSPLY SIRONA.

XRAY’s Estimate Trend

The Zacks Consensus Estimate for 2025 revenues is pegged at $3.65 billion, indicating a 3.7% decrease from the level of 2024.

The consensus mark for adjusted earnings per share is pinned at $1.90 for 2025, indicating a 13.8% year-over-year improvement.

Some other top-ranked stocks in the broader medical space that have announced quarterly results are CVS Health Corporation CVS, Integer Holdings Corporation ITGR and AngioDynamics ANGO.

CVS Health, carrying a Zacks Rank of 2, reported first-quarter 2025 adjusted earnings per share (EPS) of $2.25, beating the Zacks Consensus Estimate by 31.6%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Revenues of $94.59 billion outpaced the consensus mark by 1.8%. CVS Health has a long-term estimated growth rate of 11.4%. Its earnings surpassed estimates in each of the trailing four quarters, with an average surprise of 18.1%.

Integer Holdings reported first-quarter 2025 adjusted EPS of $1.31, beating the Zacks Consensus Estimate by 3.2%. Revenues of $437.4 million surpassed the Zacks Consensus Estimate by 1.3%. It currently sports a Zacks Rank of 1.

Integer Holdings has a long-term estimated growth rate of 18.4%. ITGR’s earnings surpassed estimates in three of the trailing four quarters and missed once, the average surprise being 2.8%.

AngioDynamics, currently sporting a Zacks Rank #1, reported a third-quarter fiscal 2025 adjusted EPS of 3 cents against the Zacks Consensus Estimate of a 13-cent loss. Revenues of $72 million beat the Zacks Consensus Estimate by 2%.

ANGO has an estimated fiscal 2026 earnings growth rate of 27.8% compared with the S&P 500 Composite’s 10.5% growth. AngioDynamics’ earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 70.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite