|

|

|

|

|||||

|

|

|

The Hershey Company HSY is facing mounting pressure from soaring cocoa prices and tariff-related impacts, with up to $100 million in potential unmitigated costs per quarter in the second half of 2025. Two-thirds of that risk is tied directly to cocoa and Canada’s retaliatory tariffs, making this one of the most critical cost headwinds for the company. Rather than rely entirely on price hikes to protect margins, Hershey is leaning into a more nuanced and consumer-centric approach, demand shaping.

This strategy includes shifting focus toward lower-cocoa segments such as sweets and salty snacks, where the company has already seen strong growth. Hershey is also activating pricing levers through price pack architecture, resizing products to improve value perception without overt price increases. This is particularly effective in value-conscious channels like convenience stores, where demand is recovering alongside increased car travel.

Moreover, the company is rolling out innovation pipelines that reduce reliance on cocoa-heavy inputs. While the upcoming Reese’s in novation is expected to support growth in chocolate, Hershey is also advancing other areas of the portfolio that are less exposed to cocoa-related cost pressures. Management noted that no further upside from travel or merchandising initiatives has been built into current forecasts, indicating cautious guidance despite tactical progress.

While demand shaping provides Hershey with a potential tool to manage input cost inflation, its effectiveness will depend on consistent execution across pricing strategies, innovation and consumer response. The company is also exploring mitigation through sourcing efforts and tariff engagement. With cocoa costs elevated and external conditions still evolving, the outlook remains uncertain. Hershey’s current approach indicates a measured response to ongoing pressures, though visibility into the second half of the year remains limited.

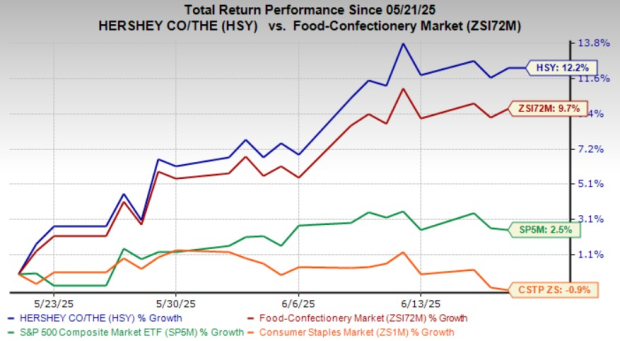

Shares of this Zacks Rank #3 (Hold) company have risen 12.2% in the past month compared with the industry’s 9.7% growth. HSY outperformed the broader Consumer Staples sector, which declined 0.9%, and the S&P 500 index, which rose 2.5% during the same period.

Closing yesterday’s trading session at $169.72, HSY stock is trading 18.4% below its 52-week high of $208.03 attained on Dec. 9, 2024. The stock is trading above its 50-day SMA (simple moving average) of $163.45, highlighting a continued uptrend. This technical strength, along with sustained momentum, indicates positive market sentiment and investors’ confidence in HSY’s financial health and growth prospects.

Hershey currently trades at a forward 12-month P/E ratio of 27.68 compared with the industry average of 22.55 and the sector average of 17.47. This valuation places the stock at a premium relative to peers, indicating broader market expectations around its business stability and ability to navigate current cost and demand dynamics.

Reflecting cautious sentiment around Hershey, the Zacks Consensus Estimate for EPS has seen downward revisions. Over the past 30 days, the consensus estimates for both the current and next fiscal year have declined 2 cents to $5.97 and 3 cents to $6.31 per share, respectively. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Nomad Foods NOMD, which manufactures frozen foods, sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

NOMD delivered a trailing four-quarter earnings surprise of 3.2%, on average. The Zacks Consensus Estimate for Nomad Foods’ current financial-year sales and earnings implies growth of 4.6% and 7.3%, respectively, from the year-ago number.

Oatly Group AB OTLY, an oatmilk company, provides a range of plant-based dairy products made from oats. It presently has a Zacks Rank of 2 (Buy). OTLY delivered a trailing four-quarter earnings surprise of 25.1%, on average.

The consensus estimate for Oatly Group’s current fiscal-year sales and earnings implies growth of 2.3% and 63.8%, respectively, from the year-ago figures.

BRF S.A. BRFS raises, produces and slaughters poultry and pork for the processing, production and sale of fresh meat, processed products, pasta, margarine, pet food and other products. It currently carries a Zacks Rank #2. BRFS delivered a trailing four-quarter earnings surprise of 5.4%, on average.

The Zacks Consensus Estimate for BRF S.A.'s current fiscal-year earnings implies growth of 11.1% from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite