|

|

|

|

|||||

|

|

|

Selective Insurance Group, Inc. SIGI shares are trading at a premium to the Zacks Property and Casualty Insurance industry. Its price-to-book value of 1.69X is higher than the industry average of 1.55X. However, its shares are trading lower than the Finance sector’s 4.12X and the Zacks S&P 500 Composite’s 8.01X.

Selective Insurance has a market capitalization of $5.31 billion. The average volume of shares traded in the last three months was 0.3 million.

Shares of other property and casualty insurers, such as Palomar Holdings, Inc. PLMR and Cincinnati Financial Corporation CINF, are also trading at a multiple higher than the industry average, while NMI Holdings Inc. NMIH is trading at a discount.

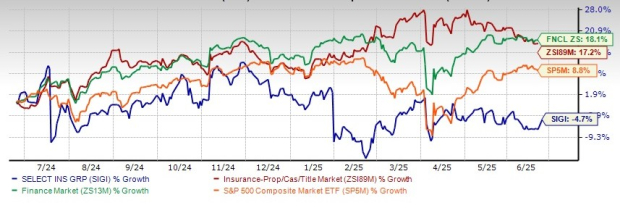

Shares of Selective Insurance have lost 4.7% in the past year, underperforming its industry, the sector and the Zacks S&P 500 composite’s growth of 17.2%, 18.1% and 8.8%, respectively, in the same time frame.

Closing at $87.44 in the last trading session, the stock stands 15.5% below its 52-week high of $103.56. The stock is trading below the 50-day and 200-day simple moving averages (SMA) of $87.75 and $90.59, respectively, indicating downward momentum. SMA is a widely used technical analysis tool to predict future price trends by analyzing historical price data.

The Zacks Consensus Estimate for Selective Insurance’s 2025 earnings per share indicates a year-over-year increase of 122%. The consensus estimate for revenues is pegged at $5.33 billion, implying a year-over-year improvement of 9.5%. The consensus estimate for 2026 earnings per share and revenues indicates an increase of 13.9% and 7.7%, respectively, from the 2025 estimates.

Three of the five analysts covering the stock have lowered estimates for 2025, and two analysts have lowered the same for 2026 over the past 60 days. The Zacks Consensus Estimate for 2025 earnings has moved down 2% in the past 60 days, while the same for 2026 has moved down 0.6% in the same time frame.

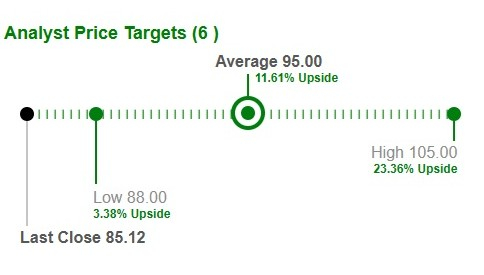

Based on short-term price targets offered by six analysts, the Zacks average price target is $95 per share. The average indicates a potential 11.6% upside from the last closing price.

Exposure growth, solid retention rates and higher new business gains in standard commercial and excess and surplus (E&S) lines should drive premium growth.

Steady betterment of premiums, improved net investment income and higher other income have resulted in top-line improvement. Over the past seven years (2017-2023), total revenues witnessed a CAGR of 8%.

The E&S Lines segment of Selective Insurance is likely to improve because of renewal pure price increases, higher direct new business and favorable E&S lines marketplace conditions.

Given impressive investment results, Selective Insurance continues to expect after-tax net investment income of $405 million in 2025. Higher income earned on fixed-income securities portfolio due to improved book yields received from the investment of operating and investing cash flows over the past year in the higher interest rate environment is likely to drive the metric.

Riding on a solid capital position, Selective Insurance has been hiking dividends, which registered a nine-year CAGR (2015-2023) of nearly 8.8%. It had $56.1 million remaining under authorization as of March 31, 2025. Riding on strong financial and operating performance, the board has approved a 9% hike in the quarterly cash dividend in the third quarter of 2024. Such steadfast endeavors buoy confidence among investors, making it an attractive pick for yield-seeking investors. Its dividend yield of 1.7% appears attractive compared with the industry average of 0.2%.

Return on equity in the trailing 12 months was 8%, better than the industry average of 7.8%. This highlights the company’s efficiency in utilizing shareholders’ funds.

While Selective Insurance remains well-positioned to gain from strong renewal, fuel price increases, favorable E&S lines marketplace conditions and higher income earned on fixed-income securities portfolio, the specific challenges facing the company, like exposure to catastrophe loss and escalating expenses, cannot be ignored.

Despite its premium valuation and bearish analysts’ sentiment, SIGI should benefit from favorable growth estimates, higher return on capital and prudent capital deployment. It is, therefore, wise to hold on to this Zacks Rank #3 (Hold) stock at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-08 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite