|

|

|

|

|||||

|

|

|

Limbach Holdings, Inc. (LMB) remains a Zacks #1 Rank (Strong Buy) stock after a huge triple digit earnings beat in the first quarter of 2025. Earnings are expected to grow doubled digits this year.

Limbach is a building systems solutions firm that partners with building owners and facilities managers who have mission critical mechanical, which includes heating, ventilation and air conditioning, electrical and plumbing infrastructure.

It works in six vertical markets: healthcare, industrial and manufacturing, data centers, life science, higher education and cultural and entertainment.

Limbach has 20 offices across the eastern United States with 1,400 team members.

On May 5, 2025, Limbach reported its first quarter results and blew by the Zacks Consensus Estimate by $0.82, or 273.3%. Limbach posted earnings of $1.12 compared to the Zacks Consensus of just $0.30.

It was the 10th earnings surprise in a row.

Revenue rose 11.9% to $133.1 million from $119 million a year ago.

The company has a strategy of growing its higher margin Owner Direct Relationships (“ODR”) business. The ODR revenue was up 21.7% to $90.4 million in the quarter. That was 67.9% of total revenue up from 62.4% last year.

Typically, the first quarter is the company’s softest due to weather and customer budget seasonality, but Limbach still found momentum in March.

Total gross profit percentage rose to 27.6% from 26.1% in the quarter mainly driven by the mix of higher margin ODR segment work and the company being more selective when pursuing General Contractor Relationships (“GCR”) work.

Limbach gained traction in key end markets like healthcare.

As of Mar 31, 2025, cash and cash equivalents were $38.1 million. Also as of Mar 31, 2025, current assets were $204.5 million and current liabilities were $131.7 million, representing a current ratio of 1.55x.

Limbach expects its ODR mix shift for the year to be between 70% and 80%.

ODR revenue growth is expected to be between 23% and 46% with total growth margins between 28% and 29%.

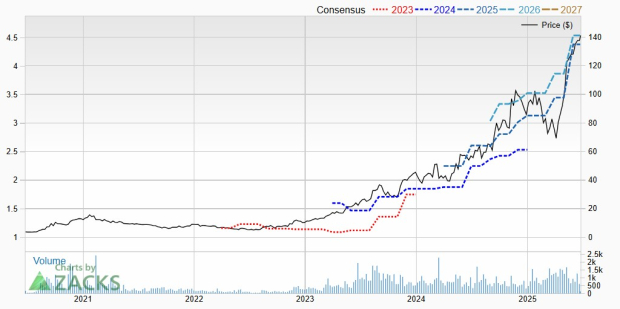

Analysts are bullish on Limbach. 2 earnings estimates were raised after the earnings report in May which pushed the Zacks Consensus Estimate up to $4.39 from $3.45. That’s earnings growth of 21.9% as the company made $3.60 last year.

2 estimates are also higher for 2026 in the last 60 days, but analysts aren’t looking too far ahead. They are projecting earnings growth of just 3.5% to $4.54 for 2026.

With double digit earnings growth expected, and Limbach being in the mission critical building systems solutions industry when data centers are hot, it’s not surprising that the shares have soared.

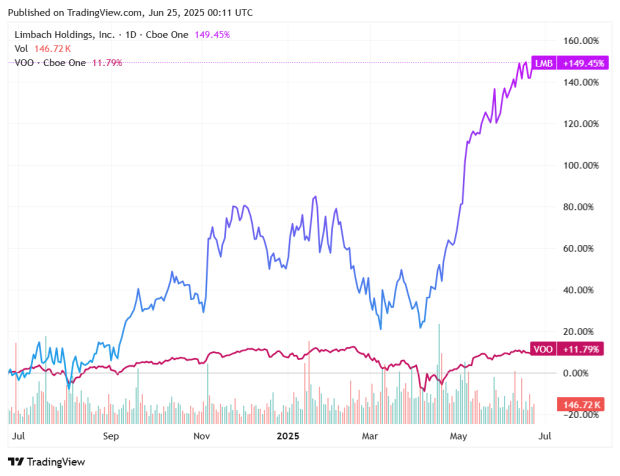

Here’s the 1-year chart of Limbach compared to the Vanguard S&P 500 ETF (VOO).

Limbach is not a cheap stock. It now has a forward P/E of 32. But you are investing in it for the strong growth.

Earnings growth for the next 3 to 5 years is forecast at 12%.

If you’re looking for a growth and momentum stock in the building systems solutions industry, Limbach should be on your short list.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Jul-14 | |

| May-27 | |

| May-18 | |

| May-06 | |

| May-05 | |

| May-05 | |

| Apr-30 | |

| Apr-14 | |

| Mar-17 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite