|

|

|

|

|||||

|

|

|

Doximity DOCS is gradually transforming from a physician-focused social network into a broader healthcare technology platform. This shift is increasingly anchored in enterprise offerings — workflow tools, integrated programs and AI-powered solutions — which now play a central role in the company’s growth narrative.

On its fourth-quarter FY2025 earnings call, management emphasized strong traction in workflow tools, such as telehealth, secure fax, scheduling and its fast-growing AI documentation assistant. These offerings reached over 620,000 unique prescribers in the quarter, with AI usage growing more than fivefold year over year. CEO Jeff Tangney described these capabilities as part of a longer-term evolution, positioning enterprise tools as Doximity’s “second act,” following its original focus on pharmaceutical marketing.

Enterprise offerings bring multiple strategic advantages — stickier revenues, larger contracts, and better visibility. For instance, integrated, multi-module are now being launched in January instead of later in the fiscal year, boosting predictability. Doximity’s client portal helps pharma clients track real-time ROI and discover upsell opportunities more efficiently, contributing to its 119% net revenue retention and 20% full-year growth.

While advertising remains a core business, management is actively shifting focus to clinical utility and platform value. Point-of-care and formulary tools, still in early adoption, are expected to become nine-figure revenue drivers.

However, this pivot is not without risks. Enterprise solutions involve longer sales cycles, more complex implementations and a different go-to-market approach. Yet, Doximity appears committed, upskilling its teams and retooling processes to support the transition.

With high engagement, expanding AI capabilities, and enterprise offerings gaining momentum, Doximity’s evolution looks more of a foundational shift than a tactical diversification. As healthcare continues to digitize, the company is increasingly positioning itself not just as a physician network, but as an essential clinical infrastructure.

HealthStream HSTM is expanding its enterprise portfolio by deepening integration across its SaaS-based workforce applications. In first-quarter 2025, the company closed a $14 million, five-year deal with a large health system, one of the biggest in its history, combining its learning, scheduling and credentialing suites. HealthStream’s emphasis is on mandatory, high-value functions such as workforce credentialing and competency development. Its hStream platform is evolving into a connective enterprise layer, enhancing interoperability across modules and delivering measurable ROI through reduced onboarding time and workforce optimization. Despite facing delays in some mid-sized deals, the company is confident in the long-term revenue visibility provided by multi-year enterprise contracts. CredentialStream and ShiftWizard, its core enterprise products, grew 25% and 19% year over year respectively, highlighting sustained demand amid macro pressure.

Amwell AMWL is positioning its Converge platform as a unified, enterprise-grade solution for virtual care. In first-quarter 2025, it achieved live deployment across five regions of the U.S. Military Health System, especially for automated and behavioral health programs. Software revenues now represent nearly half of total revenues, growing 30% year over year. Amwell is shifting from episodic telehealth toward platform-based care delivery, emphasizing scalability, AI-driven automation and data analytics. The company also integrates third-party care programs, enhancing stickiness and client ROI. Despite ongoing losses, Amwell is committed to achieving positive cash flow by 2026 through subscription-based enterprise contracts and cost realignment.

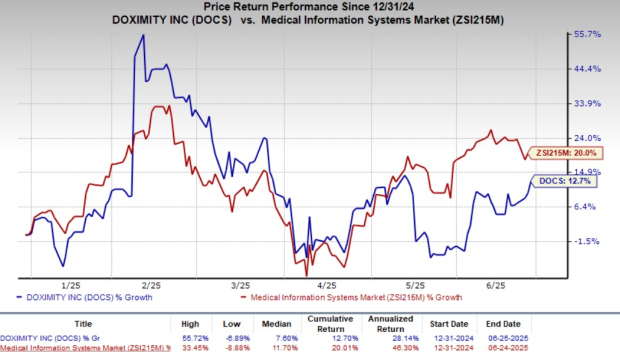

Shares of Doximity have gained 12.7% year to date compared with the industry’s growth of 20%.

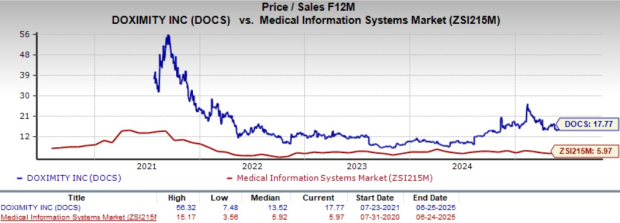

DOCS’ forward 12-month P/S of 17.8X is higher than the industry’s average of 6X. The figure is also higher than its five-year median of 13.5X. DOCS carries a Value Score of D.

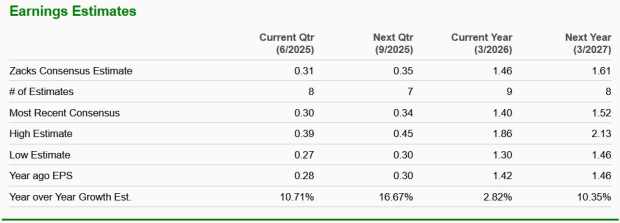

The Zacks Consensus Estimate for DOCS’ fiscal 2026 earnings per share suggests a 2.8% improvement from fiscal 2025.

Doximity stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-16 | |

| Jul-15 | |

| Jul-03 | |

| Jun-29 | |

| Jun-29 | |

| Jun-29 | |

| Jun-05 | |

| May-21 | |

| May-18 | |

| May-15 | |

| May-14 | |

| May-14 |

Doximity, 'LinkedIn For Doctors,' Hits A Record Low On AI Growing Pains

DOCS -23.00%

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite