|

|

|

|

|||||

|

|

|

Voice-driven artificial intelligence is emerging as a key battleground in tech, and SoundHound AI, Inc. SOUN and Cerence Inc. CRNC have positioned themselves at the forefront of this niche. SoundHound is a newer entrant leveraging its conversational voice platform across industries from automotive to restaurants, while Cerence is an established leader in in-car voice assistants for automakers. Both companies operate in the voice AI space, and a comparison is timely as generative AI amplifies demand for voice interfaces.

Despite their common focus on voice AI, SoundHound and Cerence differ in scope and strategy. SoundHound’s technology spans multiple industries, powering voice ordering in restaurants and voice-enabled customer service, in addition to automotive voice assistants.

In contrast, Cerence is focused on the mobility market, supplying voice assistant software to nearly every major car OEM. The broader market reach of SoundHound compared to Cerence’s auto specialization sets the stage for an intriguing comparison. Let’s analyze which voice AI stock offers better upside potential now.

SoundHound has emerged as a leader in voice AI by combining advanced speech recognition with large language models to power natural, voice-based interactions. Its Polaris AI engine delivers fast, accurate responses — even in noisy settings — supporting applications across industries. The company’s acquisitions of SYNQ3, Amelia and Allset have expanded its capabilities in restaurant ordering, customer service and voice commerce. Now operating with a three-pronged strategy — enterprise agents, automotive assistants and voice commerce —SoundHound is gaining traction among automakers and tech firms. Its innovation pace and platform versatility position it as a strong independent player in the voice AI space.

SoundHound’s broad industry reach opens up significant growth potential. It’s gaining traction in restaurants, with voice ordering in nearly 13,000 locations, and in automotive, powering voice AI for more than 20 car brands. Its enterprise solutions are used by top global banks, reflecting strong B2B adoption. This diversification limits dependence on any single customer. As generative AI demand grows, SoundHound’s independent, brand-friendly platform appeals to companies wary of Big Tech. Partnerships with firms like Lucid Motors and NVIDIA extend its footprint into luxury EVs and edge AI. Overall, SoundHound is well-positioned to scale across multiple high-growth sectors.

SoundHound’s first-quarter 2025 results highlight strong momentum, with revenues surging 151% year over year to $29.1 million, driven by organic growth and recent acquisitions. Key contributions came from restaurant and enterprise voice AI solutions, supporting diversification. While the GAAP gross margin fell to 37% due to integration costs, the adjusted gross margin stood at 51%, with management targeting margin improvements over the next 18 to 24 months. The company posted a non-GAAP net loss of $22.3 million but remains well-capitalized, holding $246 million in cash and no debt. The full-year revenue guidance of $157-$177 million implies a near doubling, and SoundHound is targeting adjusted EBITDA breakeven by year-end, signaling a focus on scaling efficiently toward profitability.

Despite operational momentum, SoundHound faces formidable competition from deep-pocketed tech giants. Alphabet GOOGL, Amazon AMZN and Apple AAPL dominate the AI-powered voice assistant market. Google Assistant powers Android Automotive and is well integrated into in-car experiences globally. Amazon’s Alexa, backed by AWS and a large developer community, is expanding into vehicles and has an entrenched smart home base. Apple’s Siri benefits from tight integration across its ecosystem, especially via iPhones and CarPlay. These larger players — Alphabet, Amazon and Apple — could leverage their ecosystems to challenge SoundHound’s growth. Another risk is the company’s heavy spend on R&D and marketing (up 66% year over year due to acquisitions), which must eventually translate into sustainable customer wins.

Cerence stands as the leading voice AI provider in the automotive industry, with its technology embedded in more than 500 million vehicles and powering roughly 51% of cars produced in the trailing 12 months ending the fiscal second quarter. Spun off from Nuance Communications, it brings decades of automotive voice expertise and serves nearly all major automakers, offering them white-labeled voice assistants that preserve brand identity and data control — an edge over Big Tech alternatives.

Despite undergoing restructuring, Cerence remains focused on innovation. Its upcoming Cerence XUI platform blends on-device processing with generative AI, while its proprietary CaLLM model (developed with NVIDIA) aims to enhance in-car voice capabilities. Integration with OpenAI’s ChatGPT via Microsoft Azure further strengthens its generative AI offerings. Beyond autos, Cerence is expanding into retail and mobility through partnerships with Code Factory and Tuya while defending its IP through active litigation. This combination of scale, neutrality and next-gen AI investment reinforces Cerence’s leadership in voice-driven mobility solutions.

Meanwhile, Cerence’s fiscal second-quarter results reflect progress in its turnaround strategy. Revenues rose 15% year over year to $78 million, slightly exceeding guidance due to a one-time $21.5 million fixed-license boost. The gross margin improved to 77% on a favorable software mix. Restructuring efforts paid off, and non-GAAP operating expenses dropped 32% to $34.1 million, fueling a sharp profitability rebound. Adjusted EBITDA surged to $29.5 million, well above guidance, while GAAP net income reached $21.7 million — a major swing from last year’s loss. Free cash flow remained strong at $13.1 million, and the company ended the quarter with $122.8 million in cash after partially repurchasing its 2025 convertible debt.

Cerence maintained fiscal 2025 revenue guidance of $236-$247 million, down from fiscal 2024 due to the loss of the Toyota contract and fewer license deals. Still, it expects adjusted EBITDA of $28-$34 million, showing a focus on profitability over growth this year. While the fiscal third quarter will face tough comps, Cerence’s leaner cost base positions it to stay cash-flow positive.

Cerence faces several challenges despite a strong fiscal second-quarter performance. The absence of fixed-license revenues in the second half will pressure margins and profitability. Auto OEMs are pushing for price reductions amid macro uncertainty and potential tariff impacts. Professional services revenues are declining faster than expected due to product standardization and OEMs’ internalizing integration. Legal disputes with Samsung and Microsoft add costs and risks. Lastly, Cerence remains exposed to global auto production trends, with volumes flat and China still a weak spot.

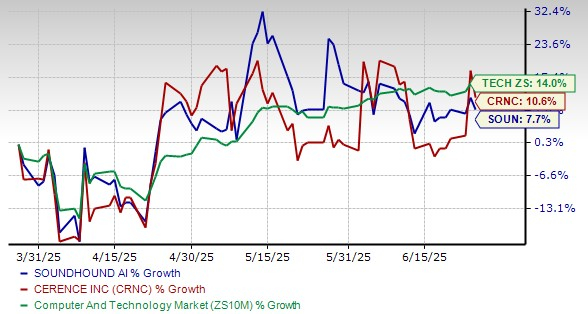

SoundHound stock has risen 7.7% over the past three months. Meanwhile, Cerence shares have rallied 10.6% over the same period. Both SOUN and CRNC stocks have underperformed the Zacks Computer and Technology sector during the period.

Share Price Performance

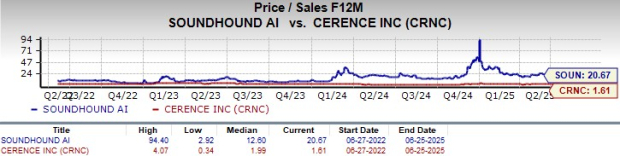

Having a market capitalization of around $3.85 billion, SoundHound’s stock has been volatile, reflecting the high expectations built into its valuation. After a huge AI-fueled rally in 2023, the stock pulled back in 2025. Even if revenues double as expected, the forward price-to-sales would be roughly 20X, still lofty relative to most software peers.

With a market capitalization of around $407.5 million, Cerence trades at roughly 1.61X trailing 12-month sales. SOUN trades at about 20.67X forward 12-month trailing sales, much higher than CRNC’s.

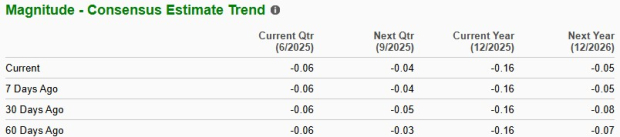

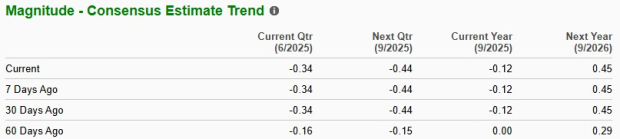

The loss estimate trend for SOUN has remained unchanged over the past 60 days, whereas the market remains skeptical about CRNC’s ability to sustain profitability. Over the same period, the estimate has changed to a loss from break-even earnings for CRNC stock for the current year.

The estimated figure for SOUN’s 2025 bottom line reflects an improvement from a year-ago reported loss of $1.04 per share, unlike CRNC. Cerence management has cited sluggish EV sales and softness in China as headwinds in the current year.

For SOUN

For CRNC

Both SoundHound AI and Cerence are prominent players in voice AI, yet they present starkly different investment profiles. SoundHound is a high-growth upstart, doubling its revenues and expanding aggressively across industries with cutting-edge voice AI solutions.

While both SoundHound and Cerence — each carrying a Zacks Rank #3 (Hold) — are credible players in voice AI, SoundHound’s diversified industry exposure, strong revenue growth and ambitious roadmap position it for broader upside as voice interfaces gain mainstream adoption. Cerence, though more deeply entrenched in the auto market, faces growth constraints and contract headwinds. Given SoundHound’s expanding customer base, product versatility and potential to scale across sectors beyond autos, it appears better positioned for long-term growth despite its premium valuation. Cerence’s stock arguably has a more limited immediate upside, with its growth currently constrained by industry softness. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 42 min | |

| 43 min | |

| 50 min | |

| 53 min | |

| 54 min | |

| 55 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite