|

|

|

|

|||||

|

|

|

Philip Morris International Inc. PM continues to demonstrate that pricing power is a central engine behind its robust profitability. In the first quarter of 2025, the company reported organic net revenue growth of 10.2% and organic operating income growth of 16%, with gross margin expansion of 340 basis points (bps) on an organic basis. Notably, pricing contributed 6 points to net revenue growth, driven by an 8% increase in combustible pricing and around 3% in smoke-free products excluding devices.

Strong pricing helped offset the unfavorable impact of combustible geographic mix and currency headwinds. Importantly, Philip Morris’ smoke-free segment, which includes IQOS, ZYN and VEEV, saw 670 bps of organic gross margin expansion, surpassing 70% in the first quarter. That is more than 5 percentage points above combustibles, reflecting a favorable product mix and premium positioning. ZYN, in particular, continues to deliver best-in-class gross margins and performs robustly at retail, maintaining a strong value share despite heavy competitor discounting.

Philip Morris’ consistent ability to implement effective pricing strategies across both combustible and smoke-free categories highlights the strength of its brand equity and consumer loyalty. As higher-margin smoke-free products continue to gain share, the company’s pricing power remains a key lever for expanding profitability. This disciplined approach positions Philip Morris to sustain margin growth while navigating macro pressures and maintaining leadership in the evolving nicotine landscape.

Altria Group, Inc. MO continues to exercise pricing power, particularly in the smokeable segment, where it achieved a 10.8% net price realization in the first quarter of 2025. Despite double-digit volume declines, Altria maintained a 64.4% adjusted OCI margin, underscoring its ability to pass on costs and sustain profitability. However, Altria faces growing price sensitivity among lower-income consumers, with an uptick in discount segment share.

Turning Point Brands, Inc. TPB emphasizes brand strength and market positioning over aggressive pricing. Stoker’s portfolio of Turning Point Brands showed volume resilience due to consumer trade-down trends, while its modern oral business relies more on strategic brand building than aggressive pricing. Turning Point Brands continues to invest heavily in distribution and marketing, with margin performance influenced by mix shifts and input cost pressures, including tariffs.

Shares of Philip Morris have gained 18.4% in the past three months compared with the industry’s growth of 18.2%.

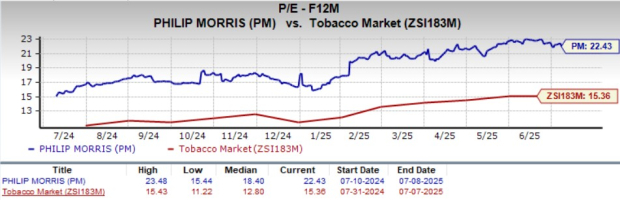

From a valuation standpoint, PM trades at a forward price-to-earnings ratio of 22.43X, up from the industry’s average of 15.36X.

The Zacks Consensus Estimate for PM’s 2025 and 2026 earnings implies year-over-year growth of 13.7% and 11.7%, respectively.

Philip Morris currently holds a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite