|

|

|

|

|||||

|

|

|

GE Aerospace GE is scheduled to release second-quarter 2025 results on July 17, before market open. The Zacks Consensus Estimate for earnings is currently pegged at $1.43 per share on revenues of $9.7 billion. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

GE’s second-quarter earnings estimates have increased a penny over the past seven days. The bottom-line projection indicates an increase of 19.2% from the year-ago number. The Zacks Consensus Estimate for quarterly revenues indicates year-over-year growth of 17.9%.

GE Aerospace has an impressive earnings surprise history. The company’s earnings outpaced the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 18%. In the last reported quarter, it delivered an earnings surprise of 18.3%.

Our proven model predicts an earnings beat for GE this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

GE has an Earnings ESP of +4.94% and sports a Zacks Rank of 1 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

GE Aerospace price-eps-surprise | GE Aerospace Quote

The growing installed base and the higher utilization of engine platforms across commercial and defense end markets are expected to have benefited GE Aerospace in the second quarter. Solid demand for LEAP, GEnx & GE9X engines and related services, supported by growth in air traffic, fleet renewal and expansion activities, is likely to have benefited the Commercial Engines & Services business. The consensus estimate for the segment’s second-quarter revenues is pinned at $7.43 billion, indicating 6.5% growth on a sequential basis.

The Defense & Propulsion Technologies business is anticipated to have performed well, backed by the growing popularity of the company’s propulsion & additive technologies, critical aircraft systems and aftermarket services in the defense sector. Rising U.S. & international defense budgets, positive airline & airframer dynamics and robust demand for commercial air travel are anticipated to have boosted the segment’s performance in the second quarter. The consensus mark for the segment’s revenues is pegged at $2.57 billion, indicating a 10.5% increase sequentially.

GE has been making investments to expand and upgrade manufacturing facilities in the United States and overseas. These investments are likely to have enabled the company to boost its operational capacities and cater to the increased demand from its commercial and defense customers. This, along with its focus on operational execution, robust backlog level and aim to generate healthy free cash flow, is likely to have bolstered its second-quarter performance.

The company’s portfolio reshaping actions include disposing non-profitable businesses to unlock value for its shareholders. In April 2024, GE completed the spin-off of its Vernova business, which marked the completion of its multi-year portfolio restructuring actions. The transaction allowed GE to achieve better operational focus on its core aerospace business and financial flexibility. This is expected to have driven its margins and profitability in the to-be-reported quarter.

However, high costs and operating expenses owing to certain projects and restructuring activities are likely to have weighed on the company’s performance. Also, supply-chain challenges, such as the availability of raw materials and labor shortages, especially in the aerospace and defense markets, are likely to have been a spoilsport.

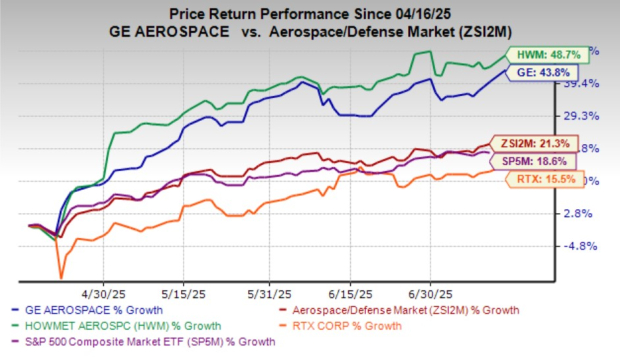

GE Aerospace’s shares have surged 43.8% in the past three months compared with the Zacks Aerospace - Defense industry’s 21.3% growth. The company’s shares have also fared comparatively better than the S&P 500’s increase of 18.6%. Its peers, RTX Corporation RTX and Howmet Aerospace Inc. HWM, have gained 15.5% and 48.7%, respectively, over the same period.

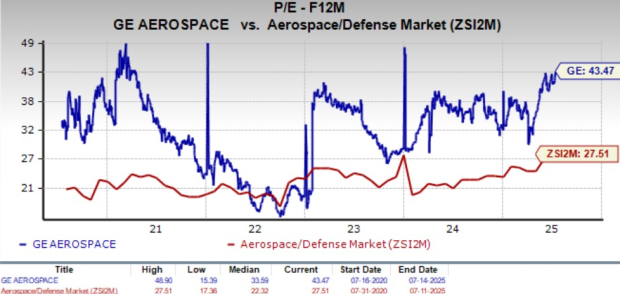

GE is trading at a forward 12-month price-to-earnings (P/E) ratio of 43.47X, higher than the industry average of 27.51X. This elevated valuation could make the stock vulnerable to further pullbacks if market sentiment sours. In comparison with GE’s valuation, RTX Corp. is trading cheaper, while Howmet Aerospace has a lofty valuation. Notably, RTX Corp. and Howmet Aerospace are currently trading at 23.55X and 48.11X, respectively.

GE Aerospace's robust and diversified portfolio, encompassing commercial engines, propulsion and additive technologies, along with the strength in the aerospace and defense markets, is likely to drive its performance. For 2025, GE expects organic revenues to grow in the low-double-digit range from the year-ago level.

We are also optimistic about its portfolio-reshaping actions, which are expected to reduce its operational costs and improve margins and cash flow in the long term. To add to its strengths, GE continues to reward shareholders with substantial dividends and share repurchases, supported by a strong cash flow and operational excellence.

GE Aerospace's solid foothold and persistent strength in the aerospace and defense markets, driven by solid build rates, wide-body aircraft recovery and robust defense budget, bode well for growth. Given the strength in most of its served markets, the company has built a sound liquidity position that supports its shareholder-friendly policies.

Despite its expensive valuation, given the positive analyst sentiment and its growth prospects, the time appears right for potential investors to bet on this company.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 11 hours | |

| 11 hours | |

| 11 hours | |

| 13 hours | |

| 15 hours | |

| 19 hours | |

| Jul-19 | |

| Jul-17 | |

| Jul-17 |

Stock Market Losses Led By Nasdaq, AI Stocks; Goldman, GE, Taiwan Semi, IBM In Focus: Weekly Review

GE

Investor's Business Daily

|

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite