|

|

|

|

|||||

|

|

|

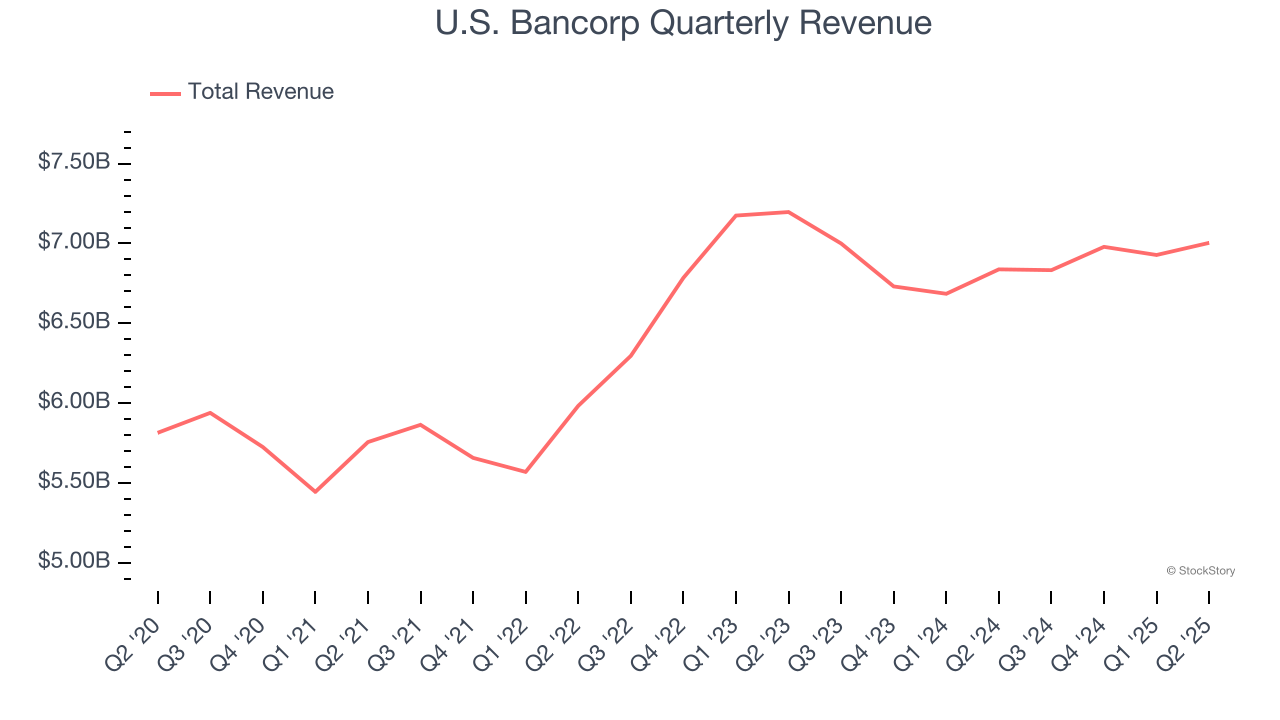

Financial services giant U.S. Bancorp (NYSE:USB) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 2.4% year on year to $7.00 billion. Its GAAP profit of $1.11 per share was 3.9% above analysts’ consensus estimates.

Is now the time to buy U.S. Bancorp? Find out by accessing our full research report, it’s free.

With roots dating back to 1863 and a presence across 26 states primarily in the Midwest and West, U.S. Bancorp (NYSE:USB) is one of America's largest banks providing lending, deposit services, wealth management, payment processing, and merchant services to individuals and businesses.

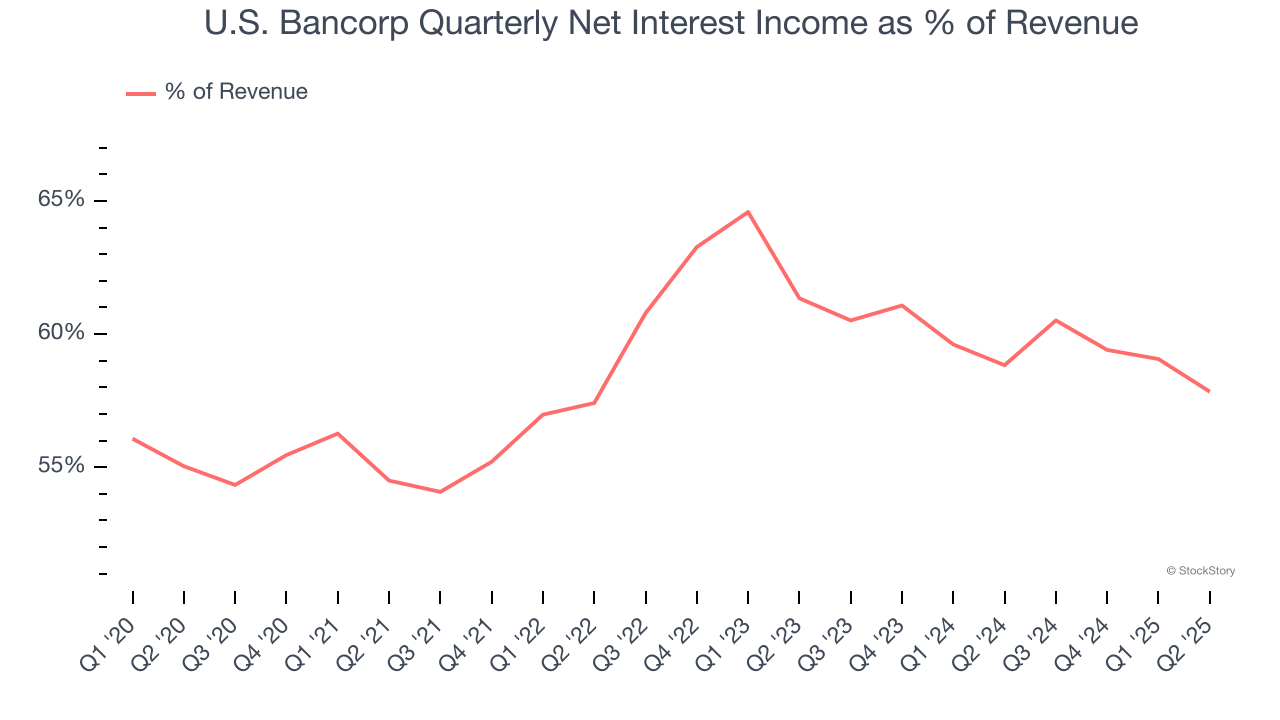

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

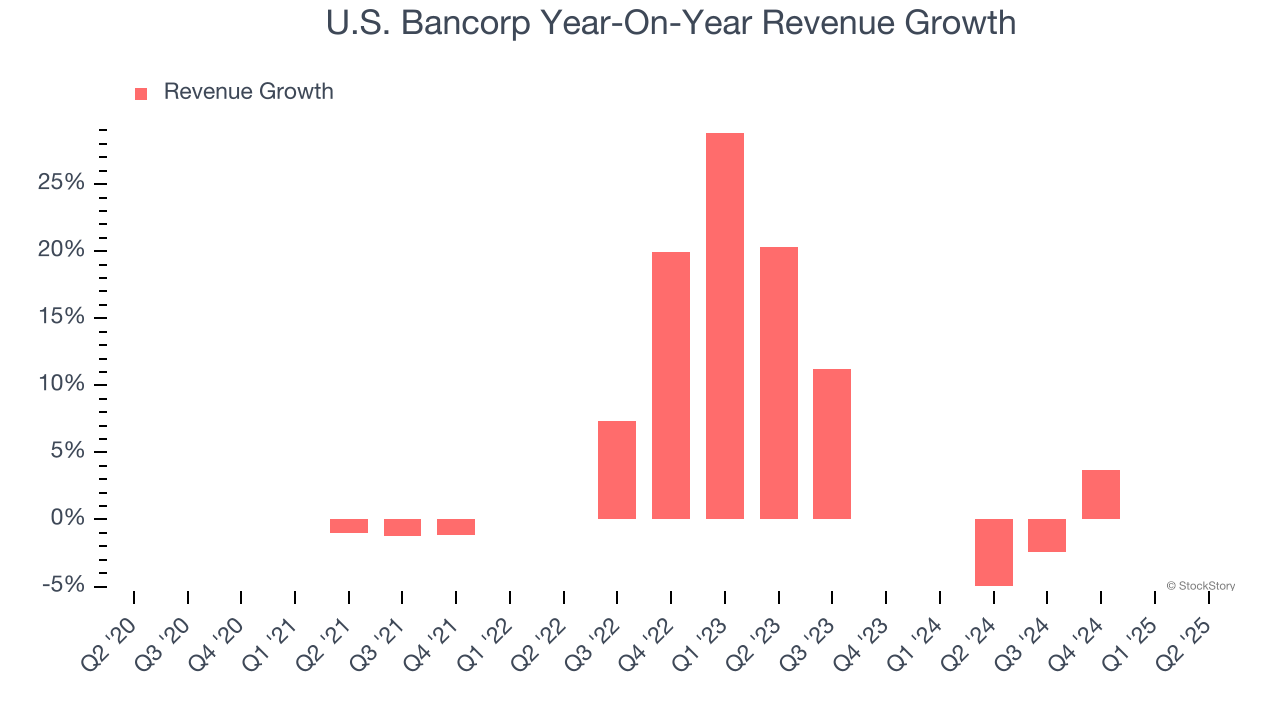

Over the last five years, U.S. Bancorp grew its revenue at a mediocre 3.7% compounded annual growth rate. This was below our standard for the bank sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. U.S. Bancorp’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, U.S. Bancorp grew its revenue by 2.4% year on year, and its $7.00 billion of revenue was in line with Wall Street’s estimates.

Net interest income made up 58.6% of the company’s total revenue during the last five years, meaning U.S. Bancorp’s growth drivers strike a balance between lending and non-lending activities.

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

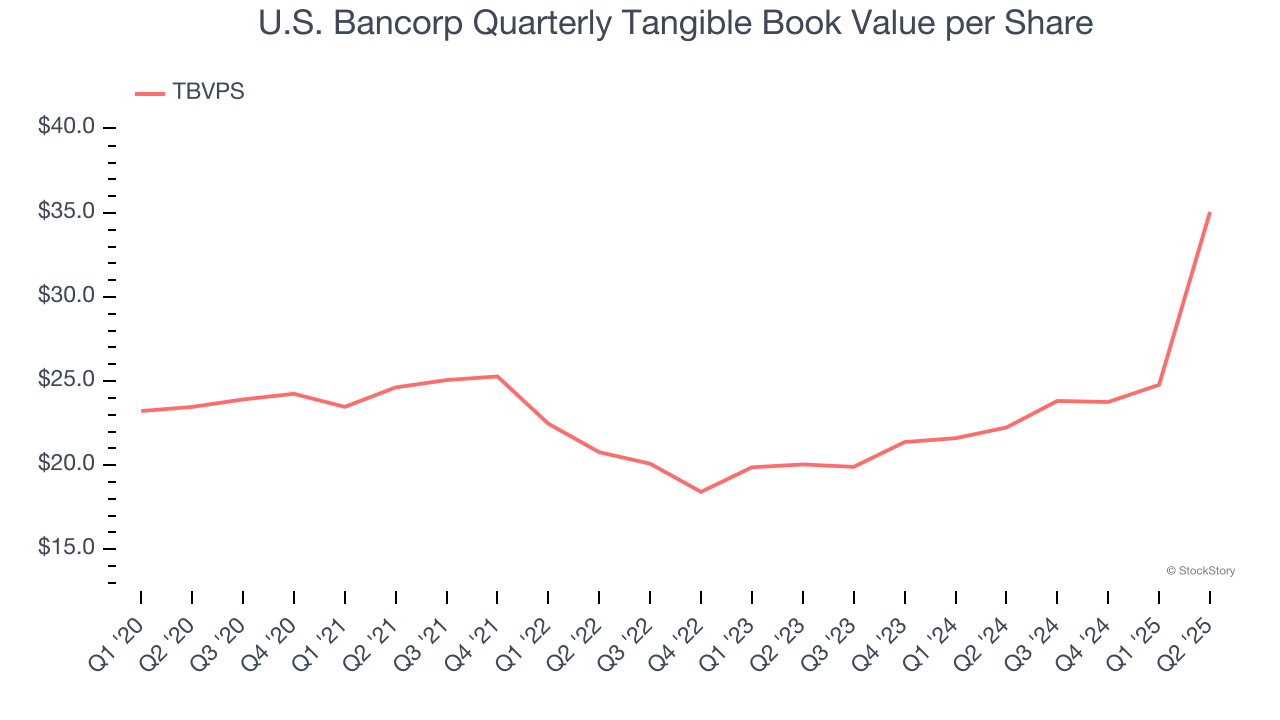

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

U.S. Bancorp’s TBVPS grew at an excellent 8.4% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 32.3% annually over the last two years from $20.04 to $35.06 per share.

Over the next 12 months, Consensus estimates call for U.S. Bancorp’s TBVPS to shrink by 16.1% to $29.41, a sour projection.

We were impressed by how significantly U.S. Bancorp blew past analysts’ tangible book value per share expectations this quarter. On the other hand, its net interest income missed and its revenue was in line with Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.8% to $43.95 immediately after reporting.

Is U.S. Bancorp an attractive investment opportunity at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-13 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-06 | |

| Feb-05 | |

| Feb-04 | |

| Feb-03 | |

| Feb-02 | |

| Feb-02 | |

| Feb-01 |

Business People: U.S. Bancorp President & CEO Gunjan Kedia to add chair to her titles

USB

Pioneer Press, St. Paul, Minn.

|

| Jan-29 | |

| Jan-29 | |

| Jan-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite