|

|

|

|

|||||

|

|

|

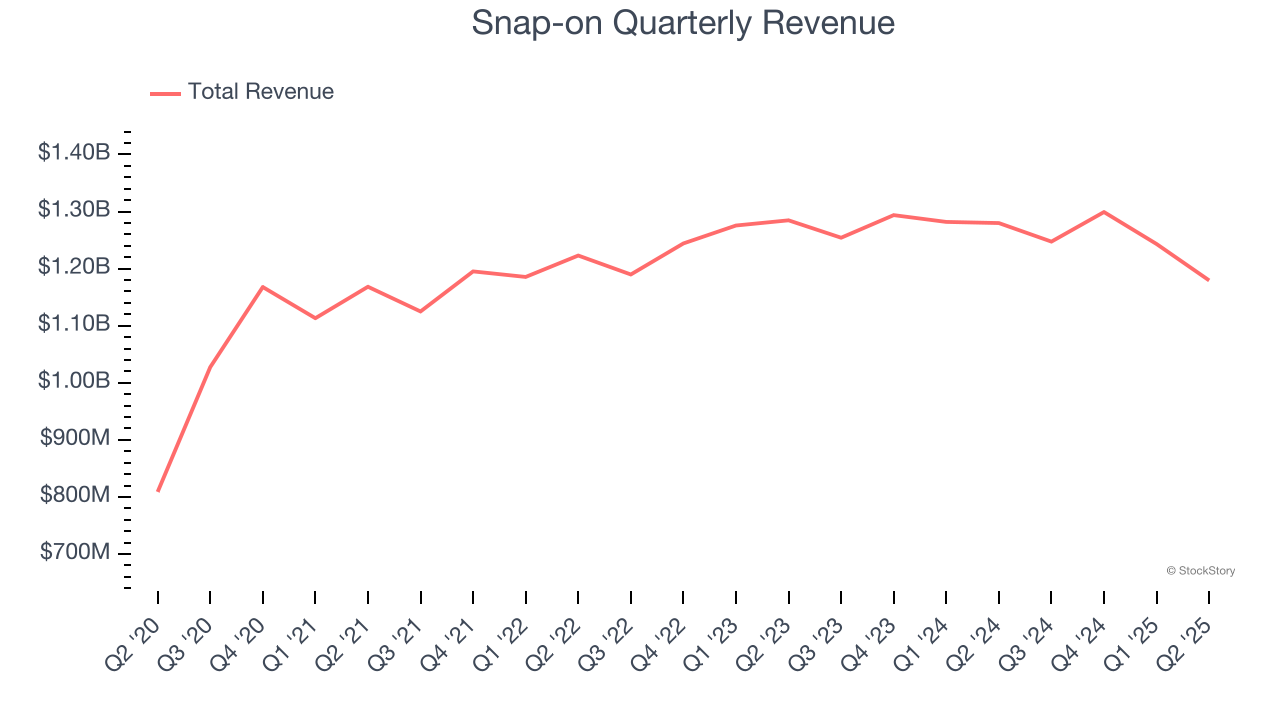

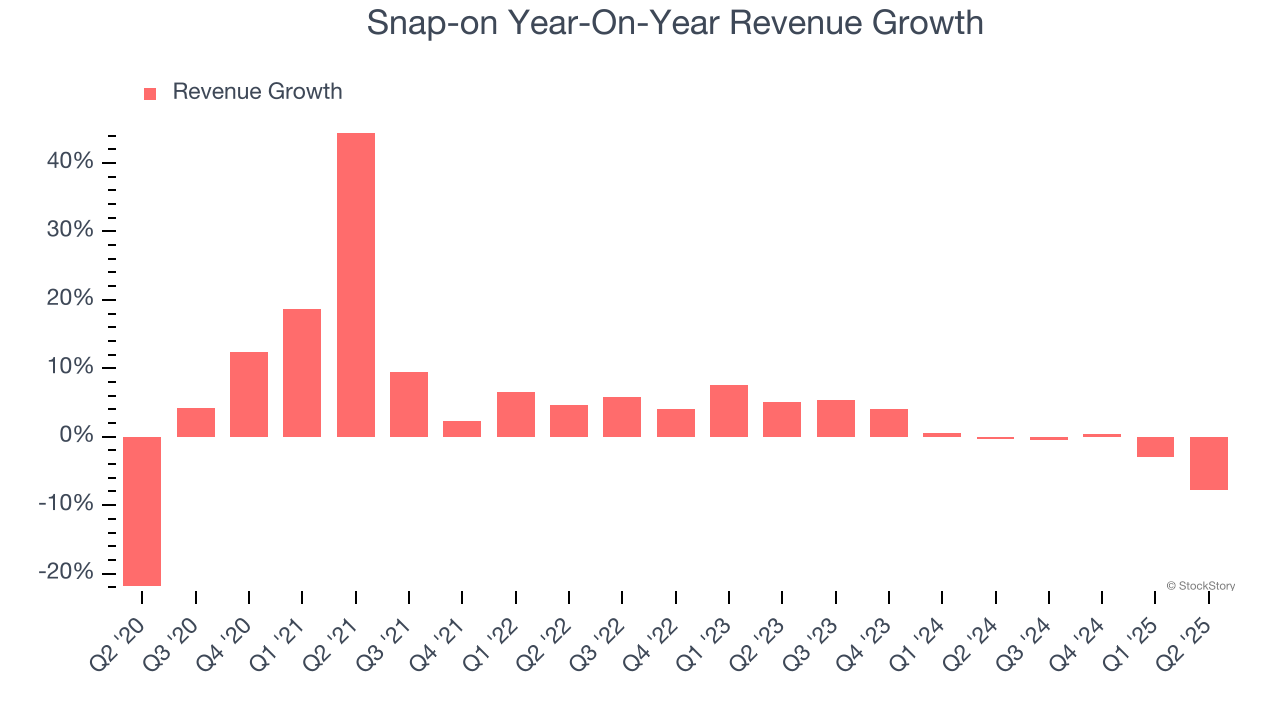

Professional tools and equipment manufacturer Snap-on (NYSE:SNA) fell short of the market’s revenue expectations in Q2 CY2025, with sales falling 7.9% year on year to $1.18 billion. Its GAAP profit of $4.72 per share was 2% above analysts’ consensus estimates.

Is now the time to buy Snap-on? Find out by accessing our full research report, it’s free.

Founded in 1920, Snap-on (NYSE:SNA) is a global provider of tools, equipment, and diagnostics for various industries such as vehicle repair, aerospace, and the military.

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Snap-on’s sales grew at a tepid 5.7% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Snap-on’s recent performance shows its demand has slowed as its revenue was flat over the last two years. We also note many other Professional Tools and Equipment businesses have faced declining sales because of cyclical headwinds. While Snap-on’s growth wasn’t the best, it did do better than its peers.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Snap-on’s organic revenue averaged 3.6% year-on-year declines. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Snap-on missed Wall Street’s estimates and reported a rather uninspiring 7.9% year-on-year revenue decline, generating $1.18 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months. While this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

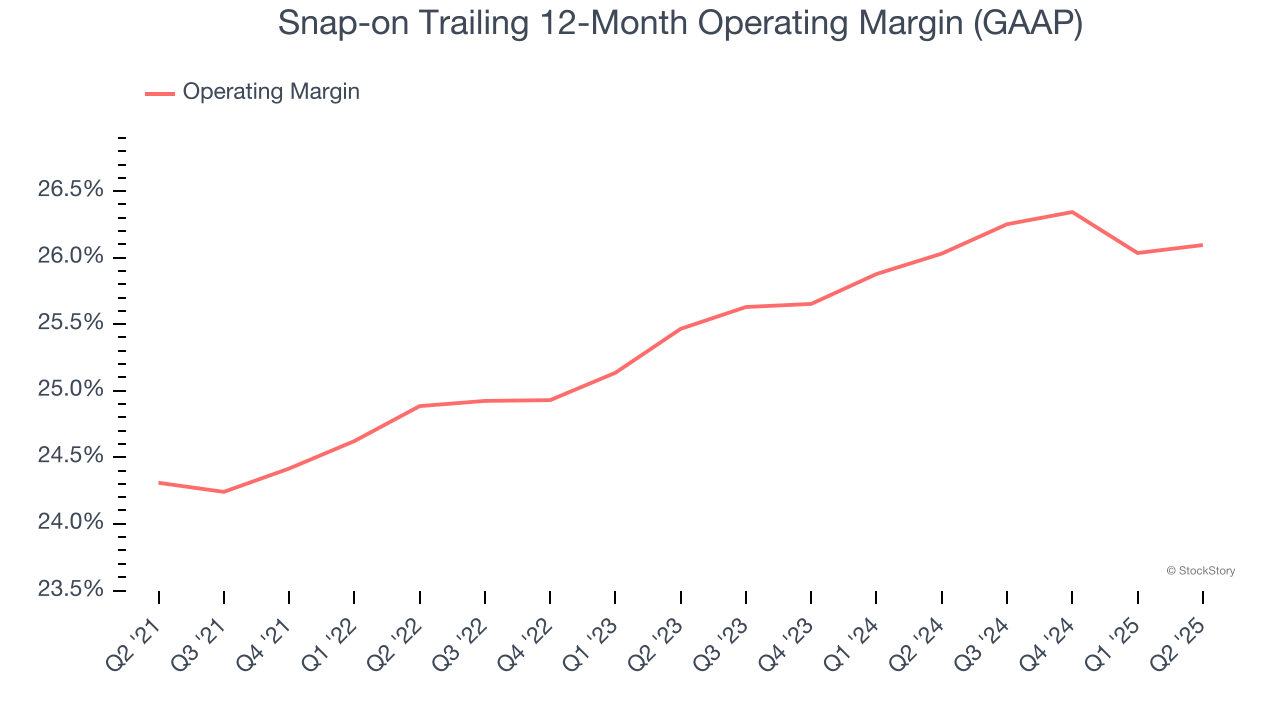

Snap-on has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 25.4%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Snap-on’s operating margin rose by 1.8 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q2, Snap-on generated an operating margin profit margin of 27.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

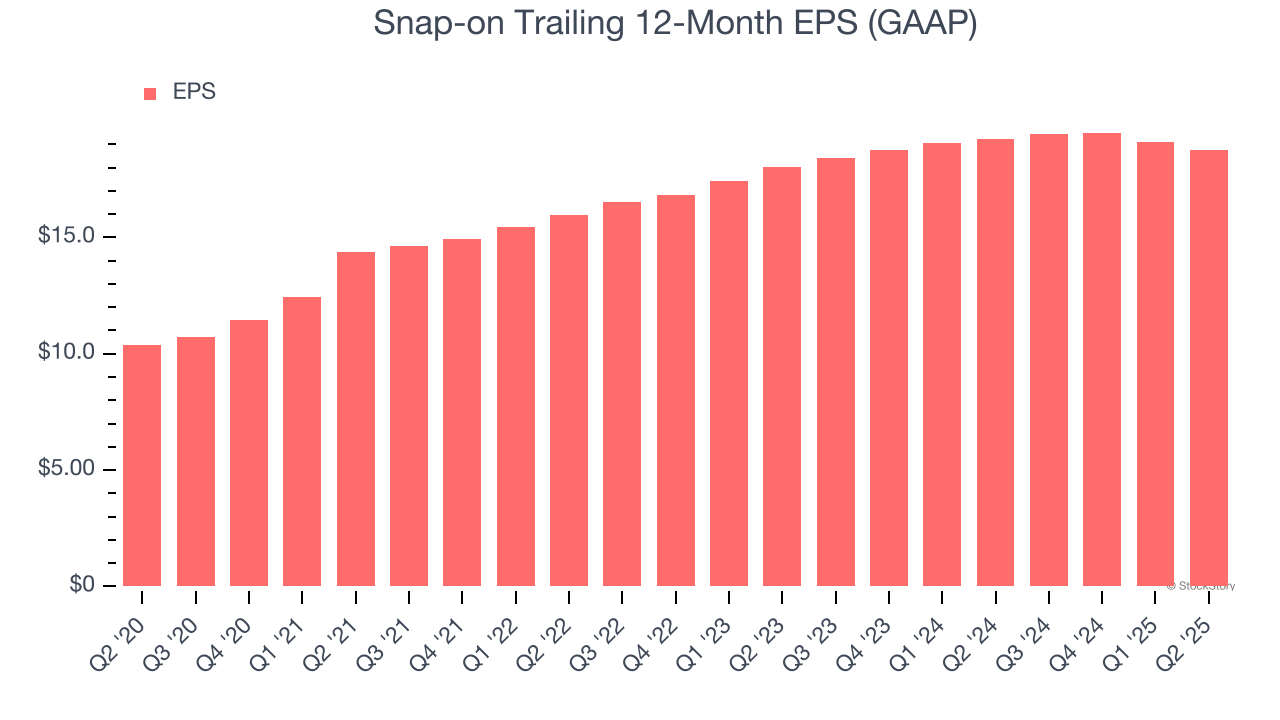

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Snap-on’s EPS grew at a remarkable 12.6% compounded annual growth rate over the last five years, higher than its 5.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

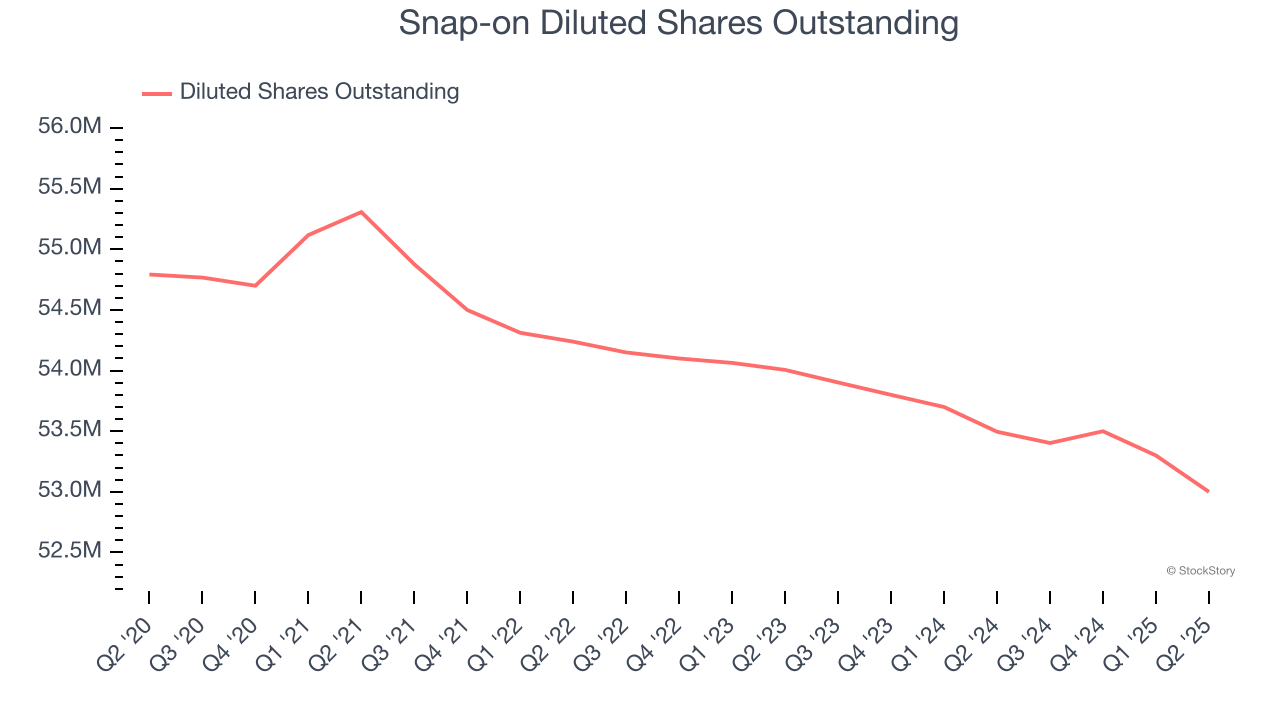

Diving into the nuances of Snap-on’s earnings can give us a better understanding of its performance. As we mentioned earlier, Snap-on’s operating margin was flat this quarter but expanded by 1.8 percentage points over the last five years. On top of that, its share count shrank by 3.3%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Snap-on, its two-year annual EPS growth of 2% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q2, Snap-on reported EPS at $4.72, down from $5.07 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2%. Over the next 12 months, Wall Street expects Snap-on’s full-year EPS of $18.76 to grow 3.2%.

It was good to see Snap-on narrowly top analysts’ organic revenue expectations this quarter. On the other hand, its revenue missed. Overall, this was a softer quarter. The stock remained flat at $311 immediately following the results.

Big picture, is Snap-on a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-09 | |

| Jun-25 | |

| Jun-09 | |

| May-28 | |

| May-05 | |

| Apr-30 | |

| Apr-29 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite