|

|

|

|

|||||

|

|

|

CSX Corporation (CSX) is scheduled to report second-quarter 2025 results on July 23, after market close.

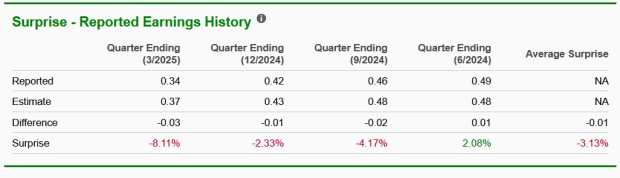

CSX has a disappointing earnings surprise history, having lagged the Zacks Consensus Estimate in three of the preceding four quarters and outpaced the mark in the remaining quarter, the average miss being 3.13%. (See the Zacks Earnings Calendar to stay ahead of market-making news)

Let’s see how things have shaped up for CSX this earnings season.

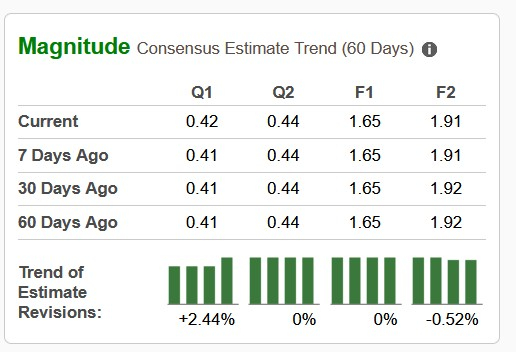

The Zacks Consensus Estimate for CSX’s second-quarter 2025 earnings has been revised upward by 2.44% in the past 60 days to 42 cents per share. However, the consensus mark implies a 14.29% downside from the year-ago actual.

Rail network issues due to headwinds like locomotive or crew/labor shortages and other service disruptions, represent a major challenge for CSX. Network issues or supply chain constraints are likely to have adversely impacted service levels, in turn hurting operating efficiency and the volume of shipments. CSX’s high capital expenditures may further impede its bottom line.

Coal market weakness continues to be a major headwind for CSX. The weak coal market has resulted in below-par coal revenues. Coal revenues fell 10% year over year in 2024, followed by a 27% year-over-year decline in first-quarter 2025. Coal volumes decreased 3% in 2024, followed by a 9% decline in first-quarter 2025. As a result of this continuous decrease, the second quarter of 2025 is likely to have witnessed a similar downtrend in the coal segment.

The Zacks Consensus Estimate for CSX’s second-quarter 2025 revenues is pegged at $3.59 billion, indicating a 3.08% decline year over year. The top line is likely to have been weighed down by a decline in coal revenues, fuel surcharges, and merchandise volume.

The Zacks Consensus Estimate for second-quarter Merchandise revenues is pegged at $2.26 billion, indicating a 1.4% downfall from the year-ago reported figure, as well as below our estimate of $2.29 billion. The Zacks Consensus Estimate for second-quarter Intermodal revenues is pegged at $504 million, indicating a 0.2% decline from the year-ago reported figure, as well as below our estimate of $528.2 million.

The Zacks Consensus Estimate for second-quarter Coal revenues is pegged at $474 million, indicating a 15.8% decline from the year-ago reported figure but above our estimate of $444.3 million. The Zacks Consensus Estimate for second-quarter Trucking revenues is pegged at $216 million, indicating a 2.2% decline from the year-ago reported figure. The consensus mark lies below our estimate of $225.7 million.

Our proven model does not conclusively predict an earnings beat for CSX this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

CSX has an Earnings ESP of -0.21% and a Zacks Rank #3.

CSX Corporation price-eps-surprise | CSX Corporation Quote

CSX reported disappointing first-quarter 2025 results, wherein both earnings and revenues lagged the Zacks Consensus Estimate. Quarterly earnings per share of 34 cents missed the Zacks Consensus Estimate of 37 cents and decreased 26% on a year-over-year basis on the back of lower revenues. Total revenues of $3.42 million missed the Zacks Consensus Estimate of $3.47 million and declined 7% year over year.

Here are a few stocks from the broader Zacks Transportation sector that investors may consider, as our model shows that these have the right combination of elements to beat on earnings this reporting cycle.

SkyWest, Inc.SKYW has an Earnings ESP of +3.06% and a Zacks Rank #2 at present. SKYW is scheduled to report second-quarter 2025 earnings on July 24. You can seethe complete list of today’s Zacks #1 Rank stocks here.

SkyWest, founded in 1972, is based in St. George and operates regional jets for major U.S. airlines. SKYW is the holding company for SkyWest Airlines, SkyWest Charter and SkyWest Leasing, an aircraft leasing company.

SKYW has an impressive earnings surprise track record, having surpassed the Zacks Consensus Estimate in each of the last four quarters, the average beat being 17.1%. The Zacks Consensus Estimate for SKYW’s second-quarter 2025 earnings has been revised 1.30% upward in the past 60 days. SKYW’s second-quarter 2025 earnings are expected to grow 28.5% year over year.

Knight-Swift Transportation Holdings Inc. (KNX) has an Earnings ESP of +3.22% and a Zacks Rank #3 at present. KNX is scheduled to report second-quarter 2025 earnings on July 23.

KNX’s second-quarter 2025 earnings are expected to grow 41.67% year over year. The Zacks Consensus Estimate for KNX’s second-quarter 2025 earnings has been revised downward by 2.86% in the past 60 days. KNX’s earnings beat the Zacks Consensus Estimate in three of the preceding four quarters (missed the mark in the remaining quarter), the average beat being 3.25%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 8 hours | |

| 9 hours | |

| 9 hours | |

| Mar-13 | |

| Mar-13 | |

| Mar-12 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite