|

|

|

|

|||||

|

|

|

We get into the heart of the Q2 earnings season this week, with more than 400 companies on deck to report results, including 109 S&P 500 members. The reporting docket expands beyond the Finance core, which has dominated the results thus far, with a representative cross-section of all sectors reporting results this week, including Tesla TSLA and Alphabet GOOGL in the Mag 7 group.

We are off to a very good start in the Q2 earnings season. It isn’t simply companies beating estimates that were too low to begin with, a reflection of analysts sharply cutting estimates in the wake of the ‘Liberation Day’ tariff announcement.

There is also favorable management commentary about current business trends that should help firm up earnings expectations for Q3 and beyond.

It is admittedly early in the reporting cycle, with Q2 results from only about 12% of S&P 500 members out, and the sample of results is over-indexed to the Finance sector. But we remain confident that the trends established at this early stage will be validated by the one-fifth of S&P 500 members reporting results this week and through the remainder of the Q2 reporting cycle.

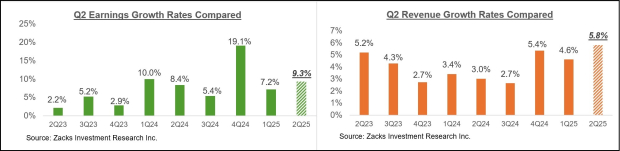

Through Monday morning (July 21st), we have seen Q2 results from 62 S&P 500 members, or 12.4% of the index’s total membership. Total earnings for these companies are up +9.3% from the same period last year on +5.8% higher revenues, with 82.3% beating EPS estimates and an equal proportion beating revenue estimates.

The EPS and revenue beats percentages are tracking notably above the historical averages for this group of 62 index members, as the comparison charts below show.

The comparison charts below show the Q2 earnings and revenue growth rates for these 62 index members relative to what we had seen from the group in other recent periods.

By the end of this week, we will have seen Q2 results from more than a third of the index’s total membership.

Alphabet will report June-quarter results after the market’s close on Wednesday (July 23rd), with the company expected to report $2.14 per share in earnings on $79.3 billion in revenues, representing year-over-year changes of +13.2% and +11.1%, respectively.

Alphabet shares have struggled this year, with the stock down -2% this year vs. a +7.3% gain for the S&P 500 index and a +9.9% gain for the Zacks Tech sector. Alphabet’s search dominance has been a perennial antitrust target, so those worries aren’t necessarily new. However, the concern among market participants is the company’s ability to secure its lucrative search franchise in the coming AI-dominated world.

Search is undoubtedly a significant contributor to earnings, but we suspect that investors' concerns about the search business may be causing them to overlook gems like YouTube and Waymo, which are integral to the Alphabet story. Then there is cloud, where Alphabet remains a leader along with Amazon and Microsoft.

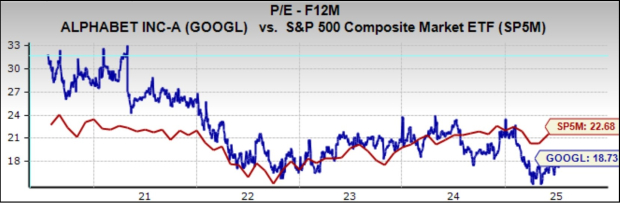

This note focuses on the evolving aggregate earnings trends, but we can’t help but flag Alphabet’s discounted valuation, as the chart below illustrates.

Tesla is also reporting the same day as Alphabet (July 23rd), with the company expected to come out with $0.40 per share in earnings on $22.5 billion in revenues, representing year-over-year changes of -23.1% and -11.9%, respectively. Tesla shares are down -18.4% this year, lagging the broader market’s +7.3% gain. In addition to operational challenges in the EV market that have been weighing on Tesla’s margins and deliveries lately, Tesla shares are also influenced by the market’s collective view of Elon Musk.

Looking at Q2 as a whole, combining the actual results that have come out with estimates for the still-to-come companies, total S&P 500 earnings are expected to be up +6% on +4.3% higher revenues.

The chart below shows current Q2 earnings and revenue growth expectations in the context of the preceding 4 quarters and the coming four quarters.

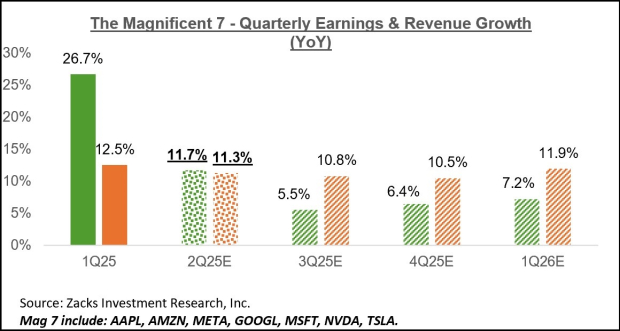

For the Mag 7, whose members start reporting results this week, total Q2 earnings are expected to be up +11.7% on +11.3% higher revenues, as the chart below shows.

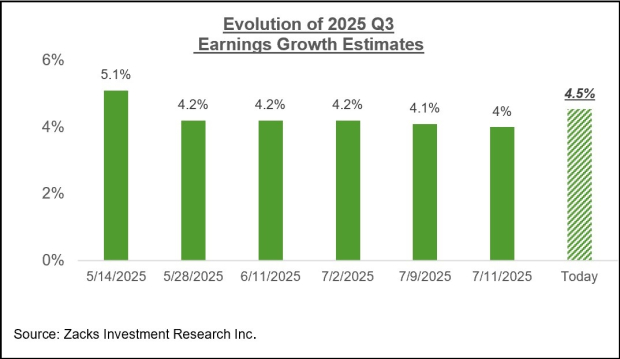

As you can see above, 2025 Q3 earnings for the S&P 500 index are currently expected to be up +4.5% from the same period last year on +4.5% higher revenues. Unlike what we had witnessed for Q2 during the first three weeks of the quarter, we are starting to see estimates modestly go up, as the chart below shows.

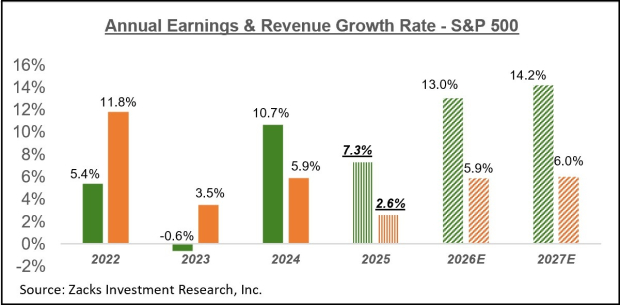

The chart below shows the overall earnings picture on a calendar-year basis.

In terms of S&P 500 index ‘EPS’, these growth rates approximate to $254.42 for 2025 and $287.60 for 2026.

The chart below shows how these calendar year 2025 earnings growth expectations have evolved since the start of Q2. As you can see below, estimates fell sharply at the start of the quarter, which coincided with the tariff announcements, but have notably stabilized over the last four to six weeks.

For a detailed view of the evolving earnings picture, please check out our weekly Earnings Trends report here >>>> Q2 Earnings Season Kicks Off Positively: A Closer Look

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 55 min | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| Jul-30 | |

| Jul-30 |

Elon Musk Mulls Selling Tesla's China Unit To Smooth SpaceX Merger: WSJ

TSLA

Investor's Business Daily

|

| Jul-30 | |

| Jul-30 |

Tesla Weighs Sale of China Business to Pave Way for Potential SpaceX Merger

TSLA

The Wall Street Journal

|

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite