|

|

|

|

|||||

|

|

|

Philip Morris International Inc. PM reported second-quarter 2025 results, with both the top and bottom lines increasing year over year. Net sales missed the Zacks Consensus Estimate, while earnings beat the same.

Results were fueled by robust momentum across regions and product categories, including continued momentum in IQOS and ZYN, along with a stable combustibles performance. Reflecting this strong performance, management has raised its full-year guidance.

Second-quarter adjusted earnings were $1.91 per share, which increased 20.1% year over year. Excluding currency effects, the adjusted EPS jumped 18.9%. The bottom line beat the Zacks Consensus Estimate of $1.85.

Net revenues of $10,140 million increased 7.1% on a reported basis and 6.8% on an organic basis. Revenues missed the Zacks Consensus Estimate of $10,255 million. The increase in organic revenues was backed by positive pricing variance (mainly driven by elevated combustible tobacco pricing) and favorable volume/mix (attributable to increased smoke-free product volumes), partially offset by lower cigarette volumes and an unfavorable cigarette mix.

Philip Morris International Inc. price-consensus-eps-surprise-chart | Philip Morris International Inc. Quote

During the second quarter, Philip Morris’ net revenues from combustible products grew 2.1% year over year and increased 2% organically, despite a return to expected volume declines. Growth was driven by continued strong pricing, partially offset by unfavorable mix dynamics.

Revenues from the smoke-free business increased 15.2% (up 14.5% on an organic basis) and formed 41% of the company’s total revenues. Within the smoke-free business, inhalable smoke-free products (SFP) were driven by strength in IQOS, while oral SFP was fueled by increased shipment volumes of ZYN.

Total shipment volumes (including heated tobacco units, oral SFP and cigarettes) increased 1.2% to 200.1 billion units in the second quarter.

The adjusted operating income ascended 16.1% (up 14.9% on an organic basis) to $4,246 million, driven by improved pricing variance and a positive volume/mix, somewhat negated by increased marketing, administration and research costs.

Following the sale of Vectura Group Ltd. on Dec. 31, 2024, the company revised its segment reporting to integrate ongoing Wellness and Healthcare results into the Europe segment. Its second-quarter 2025 financial results reflect this updated segment structure.

Net revenues in the European region grew 8.7% (up 7.3%) on an organic basis to $4,234 million. This was a result of positive pricing variance and favorable volume/mix. Total HTU and cigarette shipment volumes in the region decreased 2.4% to 55.1 billion units.

In the SSEA, CIS & MEA regions, net revenues increased 5.6% (up 4.9% organically) to $2,926 million on improved pricing variance and favorable volume. Total cigarette and HTU shipment volume in the region rose 1.1% to 95.3 billion units.

In the EA, AU & PMI GTR regions, net revenues grew 2.1% (up 1.6% organically) to $1,708 million on favorable volume/mix. Total cigarette and HTU shipment volume in the region rose 3.6% to 28.3 billion units.

Revenues in the Americas rose 12.7% (up 17% on an organic basis) to $1,272 million. This was a result of the positive volume/mix and predominantly driven by nicotine pouches in the United States. Total cigarette and HTU shipment volumes in the Americas increased 1.6% to 15.3 billion units.

The company ended the quarter with cash and cash equivalents of $4,138 million, long-term debt of $42,431million and a total shareholder deficit of $10,012 million.

Philip Morris announced its quarterly dividend of $1.35 per share ($5.40 on an annualized basis). However, the company stated that it would not make share repurchases in 2025.

Adjusted EPS for 2025 is now envisioned in the $7.43-$7.56 range, indicating 13-15% growth. Earlier, the metric was expected in the $7.36-$7.49 per share range, implying 12-14% growth. Adjusted EPS, excluding currency, is likely to be in the $7.33-$7.46 band, indicating a year-over-year increase of 11.5-13.5%. For full-year 2025, PM expects reported EPS in the band of $7.24-$7.37 compared with $4.52 in 2024.

The total international industry volume for cigarettes and HTUs (excluding China and the United States) is likely to decline nearly 1% in 2025. The total cigarette and smoke-free product shipment volume for Philip Morris is expected around 1%, driven by a smoke-free product volume increase of 12-14%, partly offset by cigarette volume declines, which are now forecasted to be around 2%.

Nicotine pouch shipment volumes in the United States are expected to be between 800 million and 840 million cans for 2025.

For 2025, PM expects net revenues to increase 6-8% on an organic basis. The operating income on an organic basis is likely to rise 11-12.5%.

Management expects an operating cash flow of more than $11.5 billion in 2025. Capital expenditures are likely to be nearly $1.6 billion, primarily implying investments to support the smoke-free business.

For the third quarter of 2025, Philip Morris envisions adjusted EPS in the range of $2.08-$2.13, including a projected favorable currency impact of five cents.

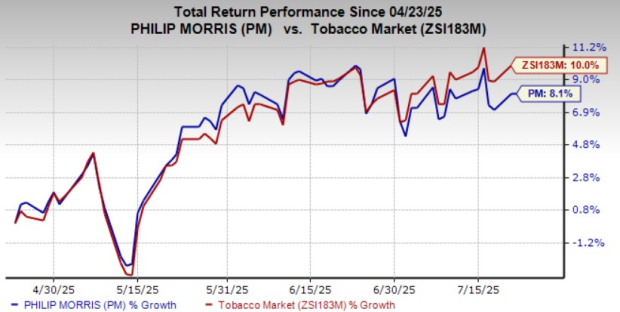

Shares of this Zacks Rank #2 (Buy) company have gained 8.1% in the past three months compared with the industry’s growth of 10%.

TreeHouse Foods, Inc. THS manufactures and distributes private-brands snacks and beverages in the United States and internationally. It presently flaunts a Zacks Rank #1(Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for TreeHouse Foods’ current financial-year sales indicates growth of 0.4% from the year-ago number. THS delivered a trailing four-quarter earnings surprise of 58.8%, on average.

Post Holdings, Inc. POST operates as a consumer-packaged goods holding company in the United States and internationally. It currently carries a Zacks Rank of 2. POST delivered a trailing four-quarter earnings surprise of 22.9%, on average.

The consensus estimate for Post Holdings’ current fiscal-year sales and earnings indicates growth of 2.6% and 5.3%, respectively, from the prior-year levels.

The Chefs' Warehouse, Inc. CHEF distributes specialty food and center-of-the-plate products in the United States, the Middle East and Canada. It currently carries a Zacks Rank of 2. CHEF delivered a trailing four-quarter earnings surprise of 10.2%, on average.

The Zacks Consensus Estimate for The Chefs' Warehouse’s current fiscal-year sales and earnings indicates growth of 6% and 12.2%, respectively, from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-08 | |

| Mar-08 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 | |

| Mar-02 | |

| Mar-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite