|

|

|

|

|||||

|

|

|

Pentair plc PNR posted adjusted earnings per share (EPS) of $1.39 for the second quarter of 2025, which beat the Zacks Consensus Estimate of $1.33 by a margin of 4.5%. The bottom line also topped its guidance of $1.31-$1.35 and marked a 14% improvement from the prior-year quarter.

Including one-time items, EPS was 90 cents compared with the prior-year quarter’s $1.11.

Pentair plc price-consensus-eps-surprise-chart | Pentair plc Quote

Net sales rose 2% year over year to $1.123 billion. The top line surpassed the Zacks Consensus Estimate of $1.115 billion. Excluding the impacts of acquisitions, divestitures and currency translation, core sales were up 1%.

The cost of sales inched up 0.8% year over year to $667 million. The gross profit was $457 million, up 4.3% from the prior-year quarter. The gross margin was 40.7% compared with the year-ago quarter’s 39.8%.

SG&A expenses totaled $214 million, up 29.5% from the prior-year quarter’s $165 million. Research and development expenses were up 1% year over year to $25 million.

The operating income, including one-time items, was $217.7 million, down 12% from the year-ago quarter. Operating margin was 19.4% compared with 22.6% in the year-ago quarter.

The adjusted segment operating income increased 9% year over year to $296.7 million. The adjusted segment operating margin was 26.4%, a 170-basis point expansion from the year-ago quarter.

Net sales in the Flow segment totaled $397 million, flat compared with the prior-year quarter. Our estimate for the segment’s net sales was $407 million. Operating earnings for the segment rose 10% year over year to $93 million. Our estimate for the segment’s operating profit was $89 million.

Net sales in the Water Solutions segment were down 4% year over year to $298 million. The figure came in short of our estimate of $306.4 million. The segment’s earnings declined 3% to $70 million and missed our projection of $73 million.

Net sales in the Pool segment totaled $427 million, up 9% year over year. Our estimate for the segment’s net sales was $399.6 million. Operating earnings for the segment grew 14.3% year over year to $152.7 million. Our estimate for the segment’s operating income was $146.7 million.

Pentair had cash and cash equivalents of around $143 million at the end of the second quarter of 2025 compared with $119 million at 2024-end. Net cash generated from operating activities was $568 million in the first half of 2025 compared with $432 million in the prior-year comparable period.

The company had a long-term debt of $1.39 billion as of June 30, 2025, down from $1.64 billion as of Dec. 31, 2024.

Pentair had hiked its dividend by 9% to 25 cents per share earlier this year. This marked the 49th consecutive year that the company has increased its dividend.

Pentair has repurchased 1.3 million of its shares for $125 million so far in 2025. As of June 30, 2025, the company had $325 million available under its share repurchase authorization.

Backed by the upbeat performance so far this year, Pentair expects adjusted EPS to be in the range of $4.75- $4.85 for 2025, higher than its previous guidance of $4.65-$4.80. The mid-point of the range indicates year-over-year growth of 9.1%.

The company has also raised its year-over-year reported sales growth guidance to 1-2% for 2025. Earlier, sales were expected to be flat or increase 2% on a reported basis from the 2024 level.

For the third quarter, the company expects an adjusted EPS between $1.16 and $1.20, implying an 8% rise at the midpoint. Pentair anticipates the quarter’s sales to be flat to up 1% from the year-ago quarter’s figure.

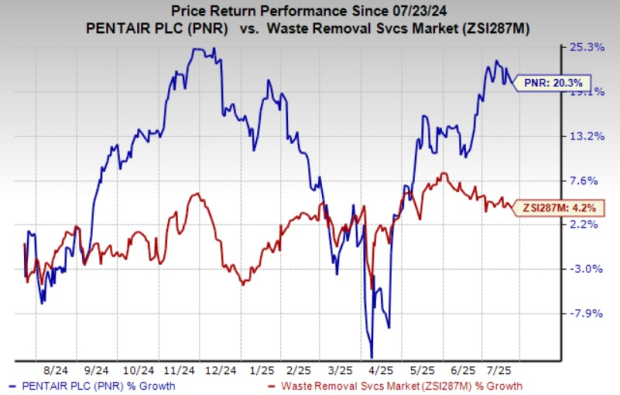

Pentair stock has gained 20.3% over the past year compared with the industry’s 4.2% growth.

Pentair currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Pool Corp. POOL is expected to release second-quarter 2025 results on July 24, 2025. The Zacks Consensus Estimate for POOL’s earnings is pegged at $5.13 per share, indicating year-over-year growth of 3%.

The estimate for Pool Corp.’s top line is pegged at $1.79 billion, implying an increase of 1.2% from the prior year’s figure. POOL has a trailing four-quarter average earnings surprise of 1.17%.

Xylem XYL, scheduled to release second-quarter 2024 results on July 31, has a trailing four-quarter average earnings surprise of 4.15%. The Zacks Consensus Estimate for Xylem’s earnings for the quarter is pegged at $1.14 per share, implying year-over-year growth of 4.6%.

The consensus estimate for Xylem’s top line is pegged at $2.21 billion, indicating a rise of 2% from the prior-year figure.

Ecolab ECL is scheduled to report second-quarter 2025 results on July 29. The Zacks Consensus Estimate for earnings is pegged at $1.90 per share, implying a 13% increase from the prior-year figure.

The estimate for Ecolab’s revenues for the quarter is $4.01 billion, indicating a 0.6% increase from the year-ago quarter. The company has an average earnings surprise of 0.7% in the past four quarters.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-31 | |

| Mar-31 | |

| Mar-29 | |

| Mar-24 | |

| Mar-24 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 | |

| Mar-19 | |

| Mar-19 | |

| Mar-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite