|

|

|

|

|||||

|

|

|

Earnings season continues to roll along, with results so far being positive. Like recent periods, the big banks helped kick off the period on a strong enough note, with many other companies following suit over the past week.

And concerning next week’s docket, a few big-time financial players – Visa V and PayPal PYPL – are on the schedule.

Let’s take a closer look at expectations.

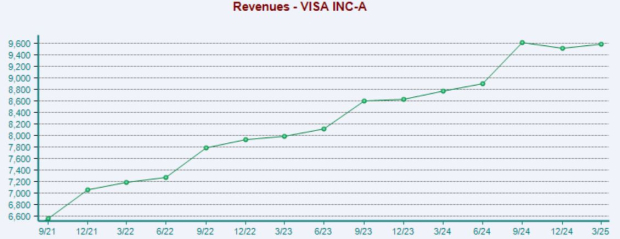

EPS and revenue expectations for Visa have been taken marginally higher over recent months, with the financial titan expected to see a nice 18% move higher in earnings alongside an 11% sales increase.

The company’s consistent top-line growth has positioned it nicely in the minds of investors over its long history, reflecting a ‘dependable’ stock overall. Below is a chart illustrating the company’s sales on a quarterly basis.

Visa’s total payments volume (TPV) is a key metric that investors closely monitor. However, the metric isn’t just watched in relation to Visa’s specific results, as it also reflects the state of the broader consumer base overall.

TPV grew 8% year-over-year throughout its latest period, undoubtedly a healthy growth rate. It’s reasonable to expect another healthy print concerning TPV, especially following the CEO’s statement following its latest release –

‘Visa’s strong 9% fiscal second quarter net revenue growth was driven by healthy trends in payments volume, cross-border volume and processed transactions. Consumer spending remained resilient, even with macroeconomic uncertainty.

He continued –

Our strategy across consumer payments, commercial and money movement solutions and value-added services, our diversified business model, and our focus on innovation position us well for the rest of the fiscal year and beyond."

Shares are heading into the release a bit expensive, with the current 28.2X forward 12-month earnings multiple above the 26.9X five-year median and reflecting a 23% premium relative to the S&P 500.

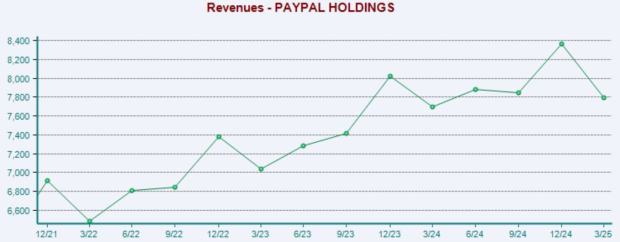

While expectations for PayPal haven’t budged much over recent months, the development still reflects a nice level of stability, certainly not raising any red flags. The payments titan is expected to see 9% EPS growth on 2.7% higher sales, with the sales growth rate accelerating nicely relative to the subsequent period. Below is a chart illustrating the company’s sales on a quarterly basis.

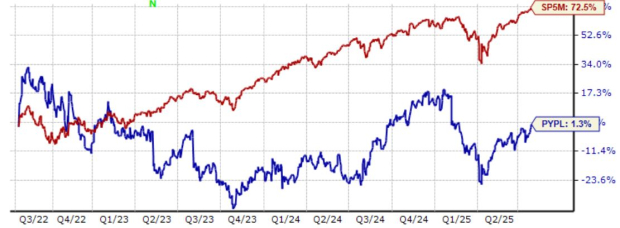

While we can see that top line growth has remained consistent, share performance hasn’t reflected the favorable development over the broader three-year period. The stock has overall been trading back-and-forth in a somewhat tight range over the past three years, nearly flat compared to a 72% gain from the S&P 500.

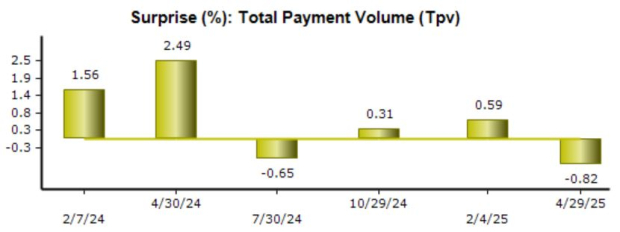

Like V, total payment volume (TPV) will be a key item to watch in the release. PayPal’s TPV totaled a sizable $417 billion throughout its latest period, up 3% from the same period last year. The Zacks Consensus estimate for TPV stands at $434.4 billion, implying a 4% year-over-year climb.

As shown below, the company has had mixed performance concerning beating our consensus TPV estimates, with two misses and two beats coming over the last four quarters.

Shares head into the print at historically low valuation levels, with the current 14.3X forward 12-month earnings multiple comparing to a 19.5X five-year median and reflecting a 37% discount relative to the S&P 500.

Bottom Line

Several notable financial titans – PayPal PYPL and Visa V – headline the reporting docket for the finance sector next week, with many other notable companies also on the list.

The outlook for Visa heading into the release seems relatively ‘calm’, with expectations trending marginally higher over recent months. While shares do trade at a steep premium, Visa’s consistent and predictable growth both help ease the valuation concern.

The setup for PayPal appears similarly calm given its historically low valuation multiples and decent growth in TPV also forecasted. As shown above, the stock hasn’t done much of anything over the past three years, with a positive set of results and decent commentary surrounding guidance potentially finally getting the stock out of its lull.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours |

What the $38 billion Visa, Mastercard swipe fee settlement means for credit card users

V

Yahoo Personal Finance

|

| 14 hours | |

| 15 hours | |

| 19 hours | |

| Jun-09 |

Judge Gives Preliminary Approval to Visa-Mastercard Settlement With Merchants

V

The Wall Street Journal

|

| Jun-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite