|

|

|

|

|||||

|

|

|

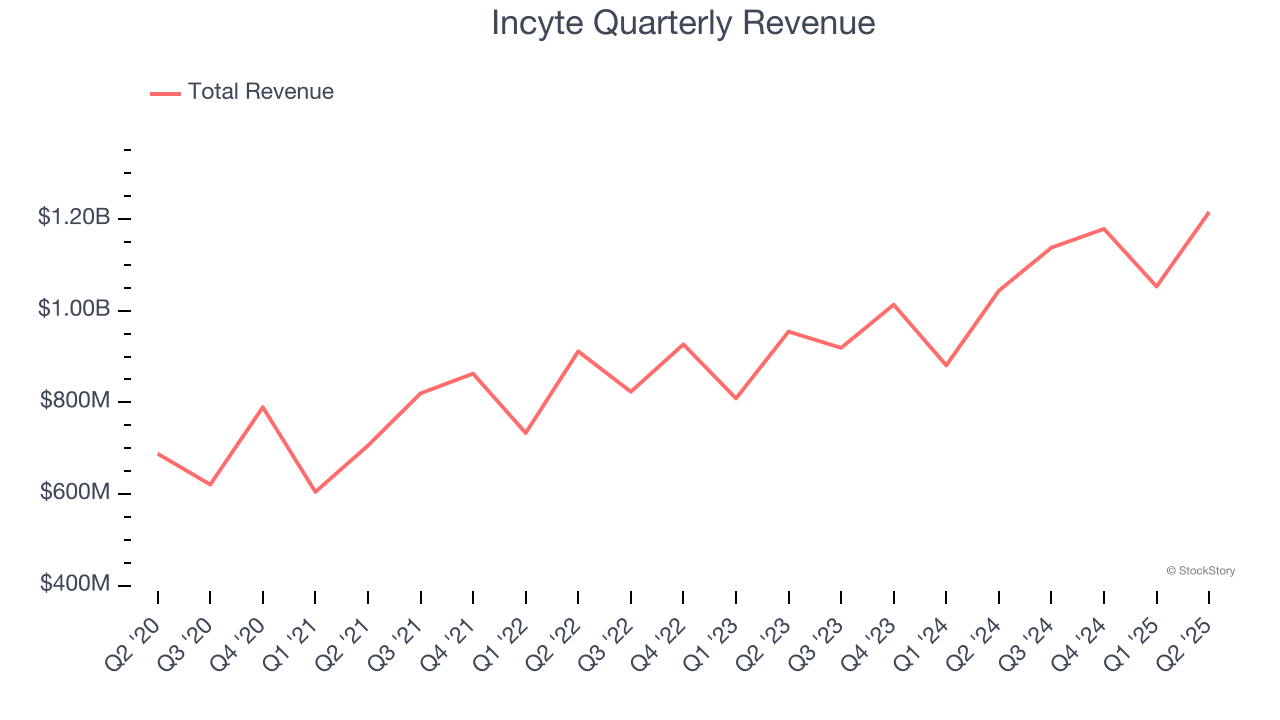

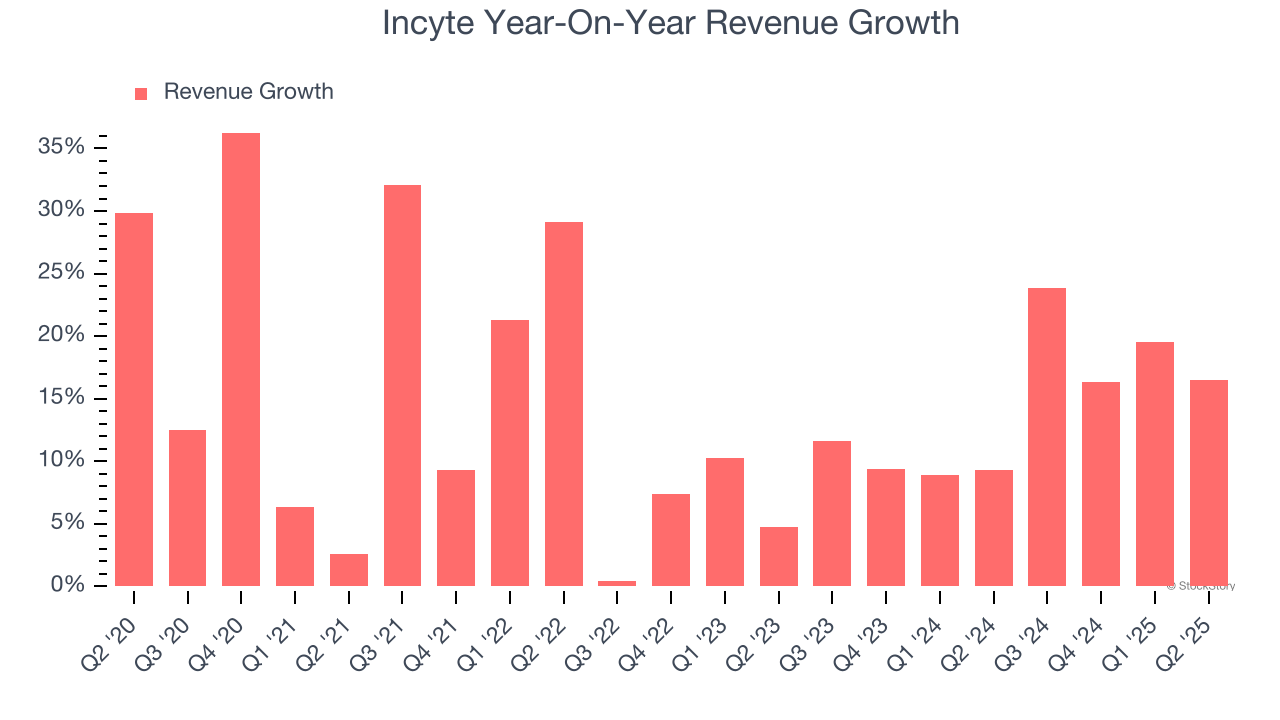

Biopharmaceutical company Incyte Corporation (NASDAQ:INCY) announced better-than-expected revenue in Q2 CY2025, with sales up 16.5% year on year to $1.22 billion. Its non-GAAP profit of $1.57 per share was 6.5% above analysts’ consensus estimates.

Is now the time to buy Incyte? Find out by accessing our full research report, it’s free.

"...Our second quarter results reflect strong growth for Jakafi® (ruxolitinib), Opzelura® (ruxolitinib) cream and Niktimvo™ (axatilimab), positioning us well to deliver on our 2025 objectives," said Bill Meury, Chief Executive Officer, Incyte.

Founded in 1991 and evolving from a genomics research firm to a commercial-stage drug developer, Incyte (NASDAQ:INCY) is a biopharmaceutical company that discovers, develops, and commercializes proprietary therapeutics for cancer and inflammatory diseases.

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Incyte’s 13.9% annualized revenue growth over the last five years was solid. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Incyte’s annualized revenue growth of 14.2% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Incyte reported year-on-year revenue growth of 16.5%, and its $1.22 billion of revenue exceeded Wall Street’s estimates by 5.5%.

Looking ahead, sell-side analysts expect revenue to grow 7.5% over the next 12 months, a deceleration versus the last two years. Still, this projection is above average for the sector and suggests the market sees some success for its newer products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

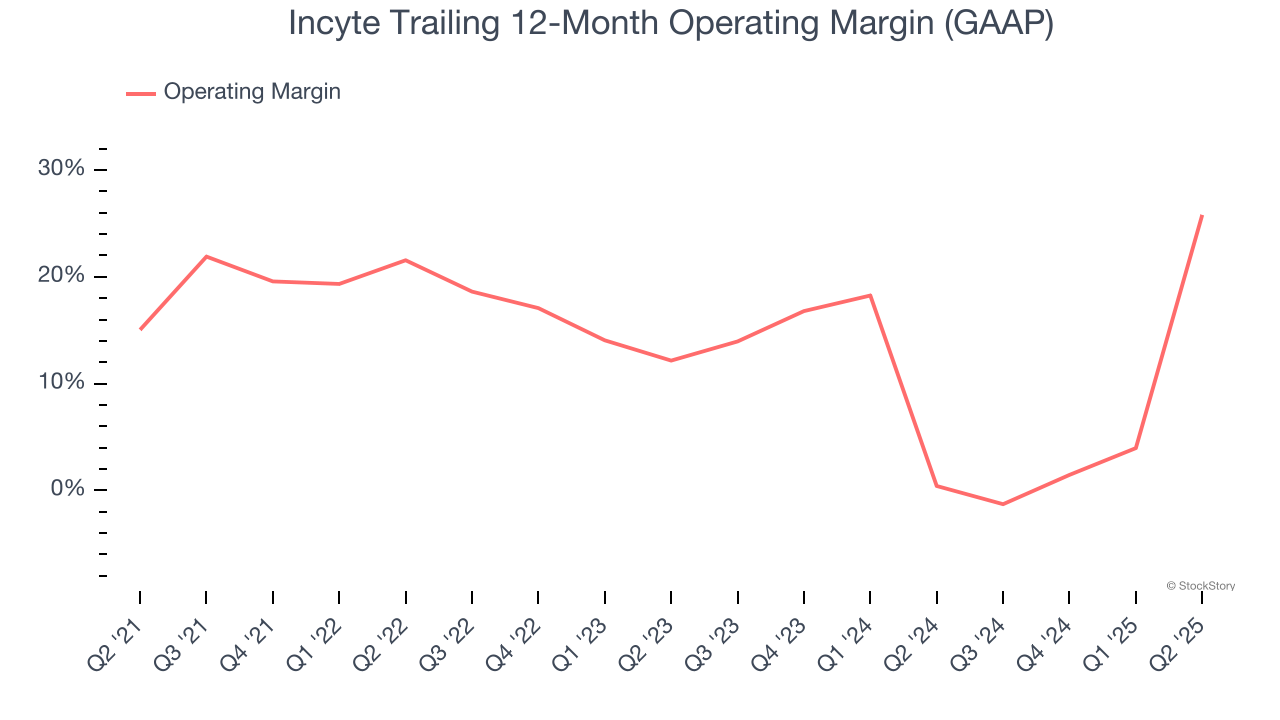

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Incyte has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 15.3%.

Looking at the trend in its profitability, Incyte’s operating margin rose by 10.8 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 13.6 percentage points on a two-year basis. These data points are very encouraging and shows momentum is on its side.

In Q2, Incyte generated an operating margin profit margin of 43.6%, up 89.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

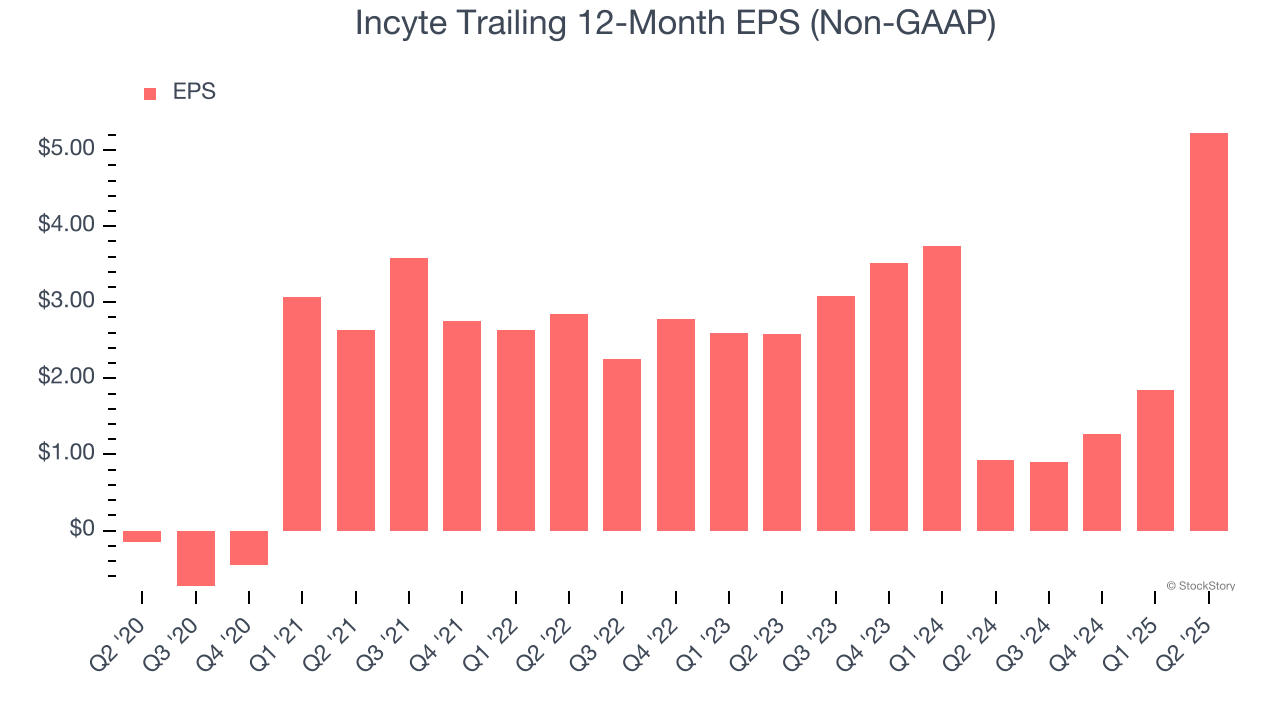

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Incyte’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

In Q2, Incyte reported EPS at $1.57, up from negative $1.82 in the same quarter last year. This print beat analysts’ estimates by 6.5%. Over the next 12 months, Wall Street expects Incyte’s full-year EPS of $5.23 to grow 16.9%.

We were impressed by how significantly Incyte blew past analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 4% to $73 immediately after reporting.

Incyte had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Incyte Crumbles As Light Opzelura Guide Undoes Quarterly Sales Beat

INCY -8.24%

Investor's Business Daily

|

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite