|

|

|

|

|||||

|

|

|

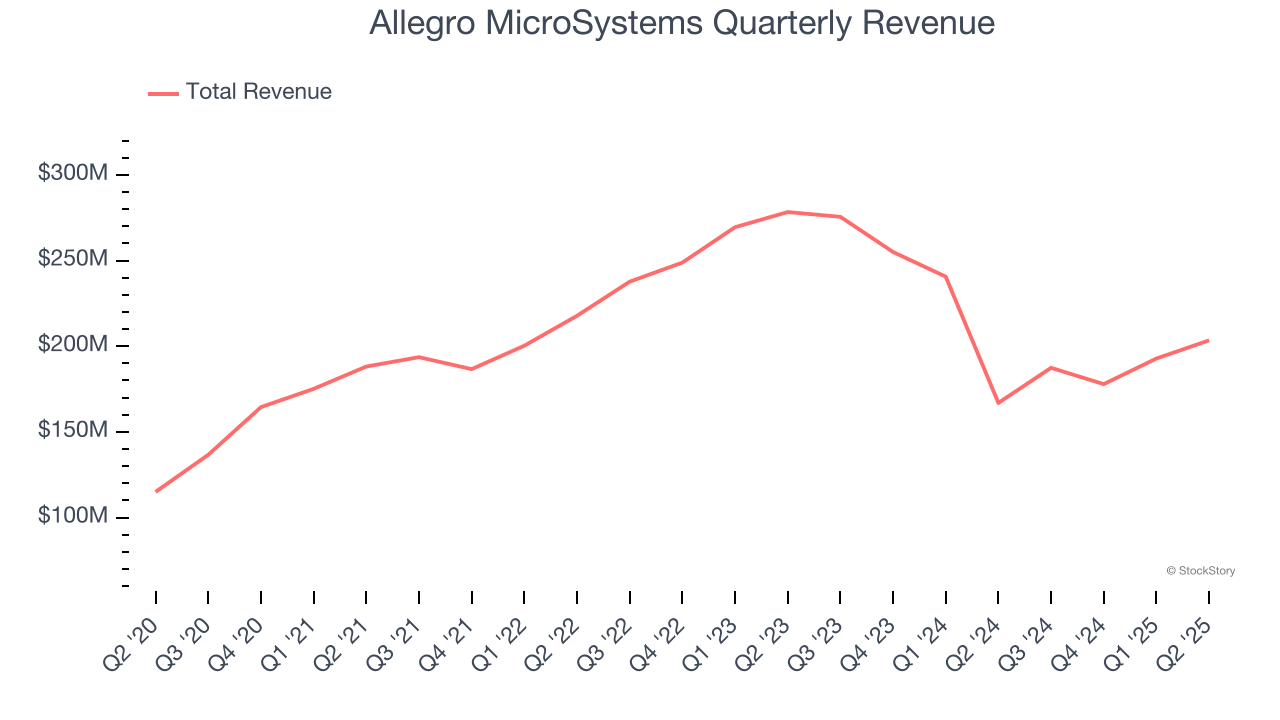

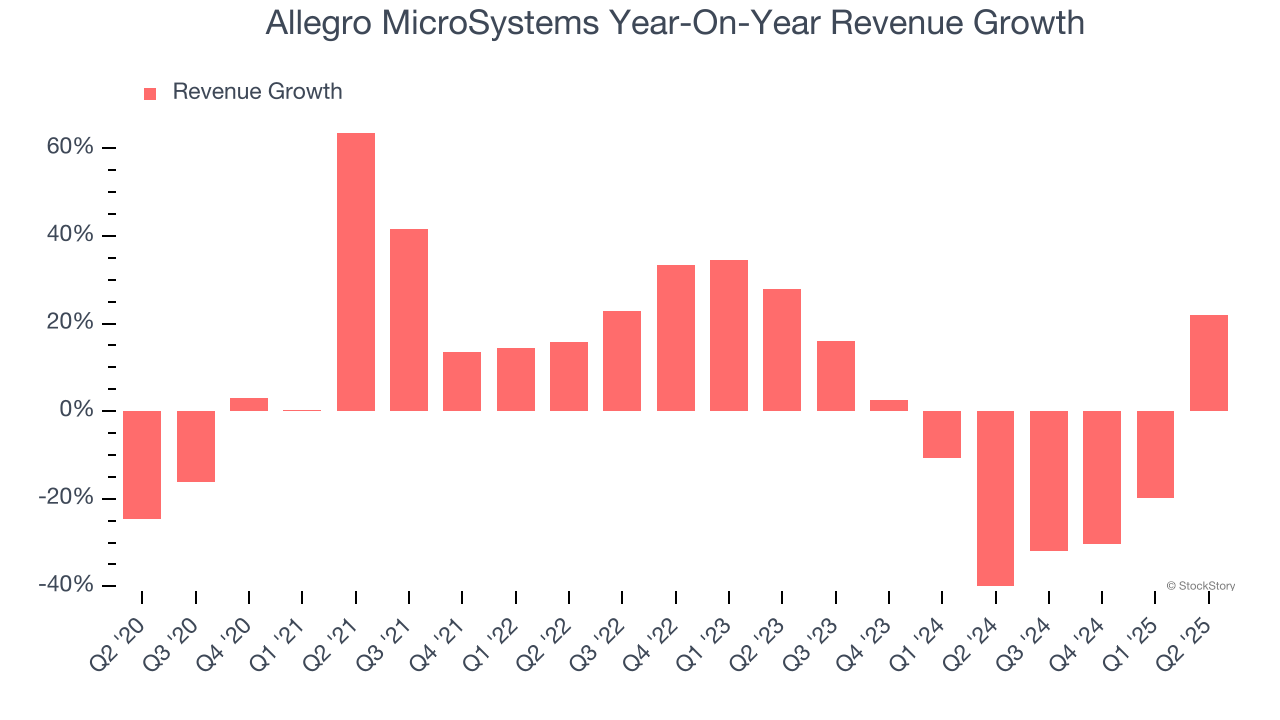

Chip designer Allegro MicroSystems (NASDAQ:ALGM) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 21.9% year on year to $203.4 million. Guidance for next quarter’s revenue was better than expected at $210 million at the midpoint, 1.4% above analysts’ estimates. Its GAAP loss of $0.07 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Allegro MicroSystems? Find out by accessing our full research report, it’s free.

“We delivered strong first quarter results, with sales of over $203 million, up 22% year-over-year, and led by growth in both e-Mobility and Industrial and Other, increasing 31% and 50% year-over-year, respectively. Non-GAAP EPS was $0.09, increasing nearly 3x year-over-year, demonstrating the significant operating leverage in our business model,” said Mike Doogue, President and CEO of Allegro.

The result of a spinoff from Sanken in Japan, Allegro MicroSystems (NASDAQ:ALGM) is a designer of power management chips and distance sensors used in electric vehicles and data centers.

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Allegro MicroSystems grew its sales at a sluggish 4.4% compounded annual growth rate. This was below our standard for the semiconductor sector and is a tough starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Allegro MicroSystems’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 14.2% annually.

This quarter, Allegro MicroSystems reported robust year-on-year revenue growth of 21.9%, and its $203.4 million of revenue topped Wall Street estimates by 2.8%. Adding to the positive news, Allegro MicroSystems’s growth inflected positively this quarter, indicating that the recent cyclical downturn is likely in the rearview mirror. Company management is currently guiding for a 12.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 15.3% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and suggests its newer products and services will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

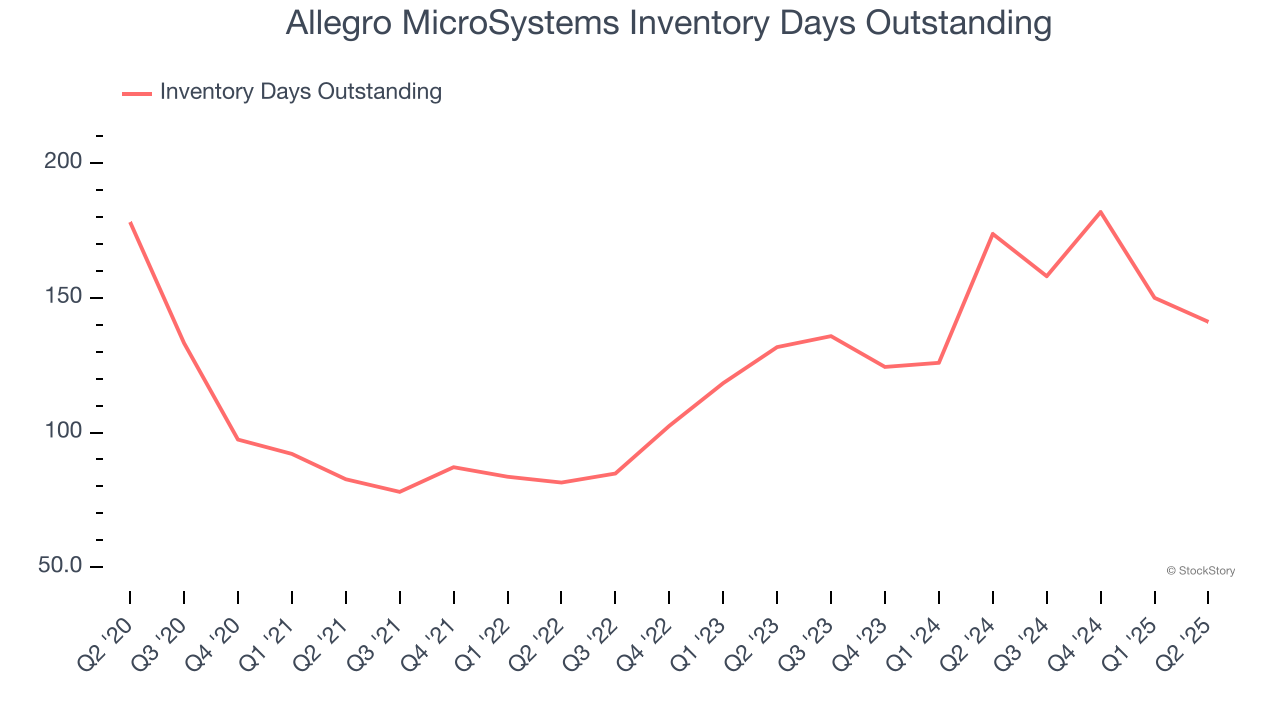

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Allegro MicroSystems’s DIO came in at 141, which is 23 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

We were impressed by how Allegro MicroSystems beat analyst' guidance expectations this quarter. We were also glad its inventory levels shrunk. On the other hand, its EPS missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 2% to $33.19 immediately following the results.

So do we think Allegro MicroSystems is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| Jul-30 | |

| Jul-30 | |

| Jul-20 | |

| Jul-16 | |

| Jul-13 | |

| Jul-09 | |

| Jul-02 | |

| Jul-02 | |

| Jul-01 | |

| Jun-29 |

Allegro MicroSystems Spikes To All-Time High On 'Best Idea' Rating

ALGM +14.65%

Investor's Business Daily

|

| Jun-18 | |

| May-13 | |

| May-13 | |

| May-07 | |

| May-07 |

Allegro MicroSystems Stock Dips Despite Beat-And-Raise Earnings Report

ALGM -6.70%

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite