|

|

|

|

|||||

|

|

|

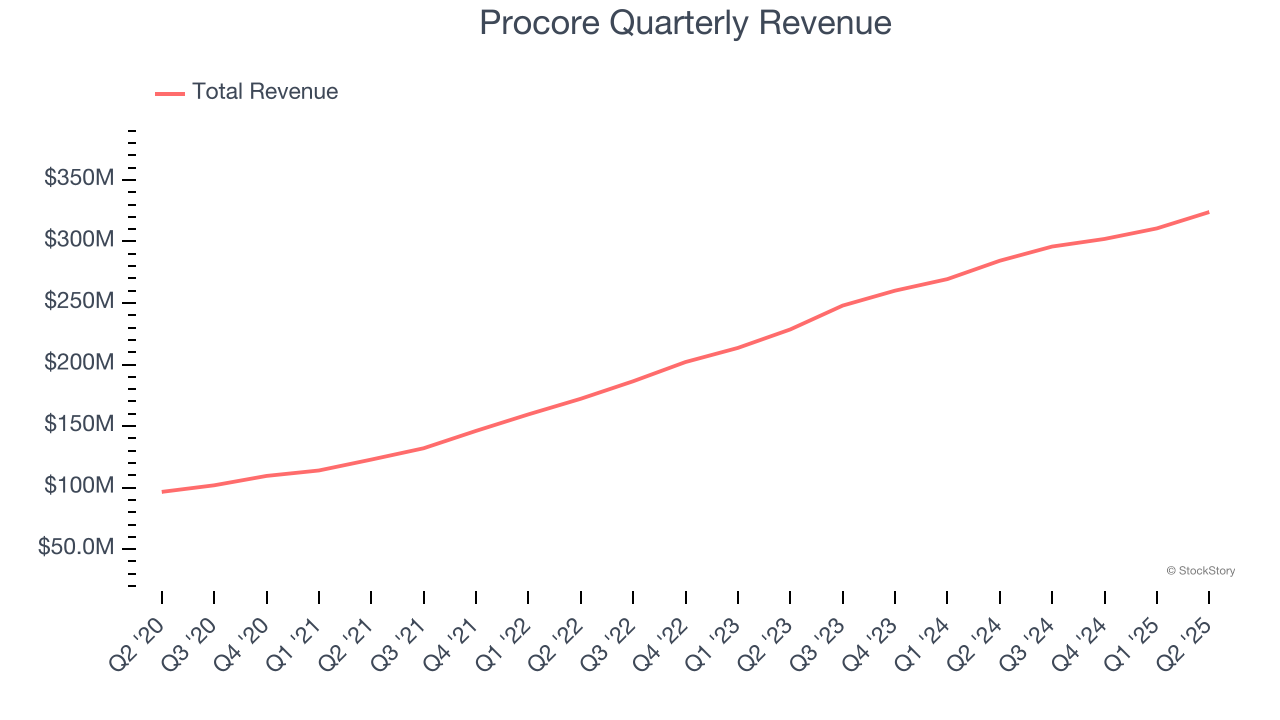

Construction management software maker Procore (NYSE:PCOR) announced better-than-expected revenue in Q2 CY2025, with sales up 13.9% year on year to $323.9 million. The company expects next quarter’s revenue to be around $327 million, close to analysts’ estimates. Its non-GAAP profit of $0.35 per share was 33.4% above analysts’ consensus estimates.

Is now the time to buy Procore? Find out by accessing our full research report, it’s free.

Used to manage the multi-year expansion of the Panama Canal that began in 2007, Procore (NYSE:PCOR) offers a software-as-service project, finance, and quality management platform for the construction industry.

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Procore’s sales grew at a solid 26.4% compounded annual growth rate over the last three years. Its growth beat the average software company and shows its offerings resonate with customers.

This quarter, Procore reported year-on-year revenue growth of 13.9%, and its $323.9 million of revenue exceeded Wall Street’s estimates by 3.9%. Company management is currently guiding for a 10.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.9% over the next 12 months, a deceleration versus the last three years. Still, this projection is above average for the sector and implies the market sees some success for its newer products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

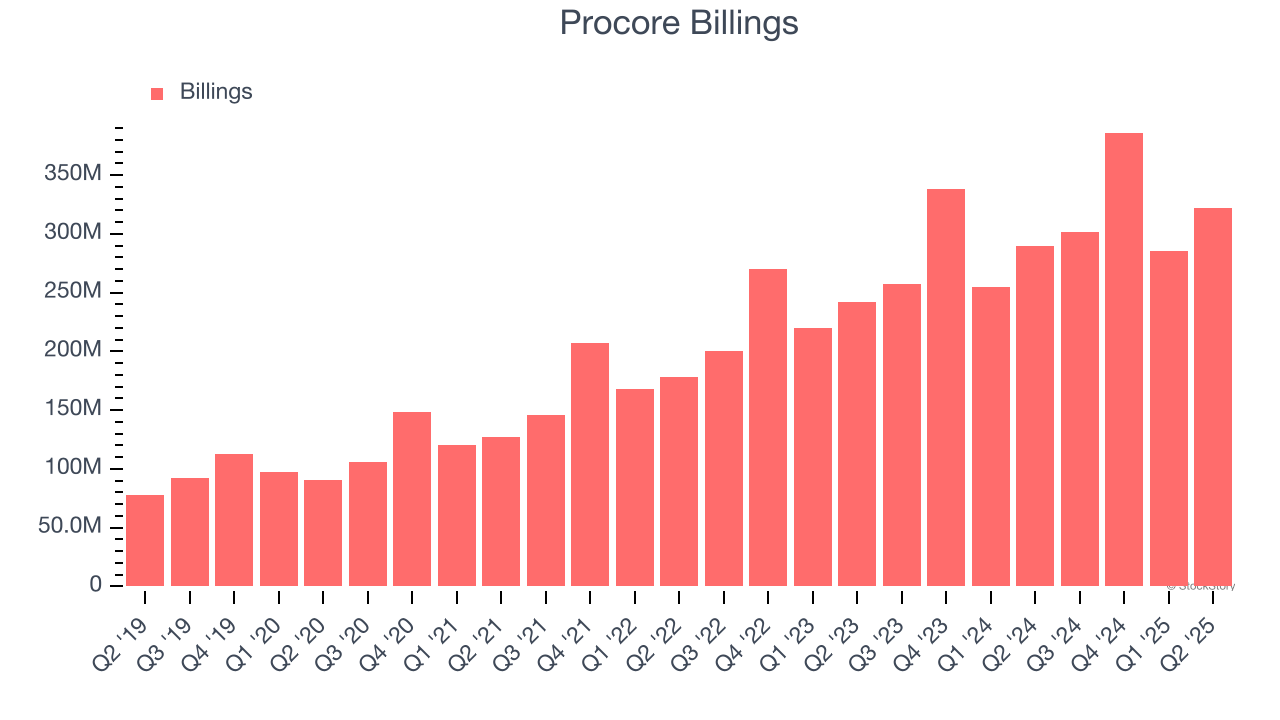

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Procore’s billings punched in at $322.2 million in Q2, and over the last four quarters, its growth slightly outpaced the sector as it averaged 13.6% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

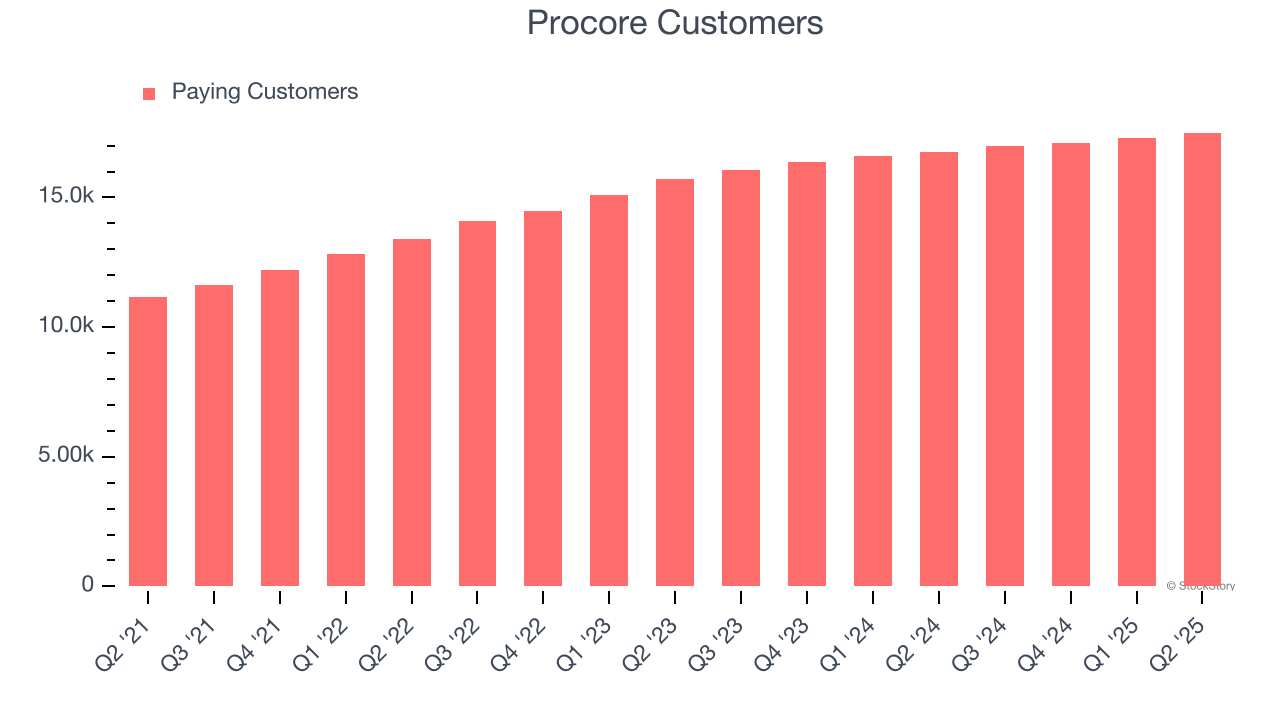

Procore reported 17,501 customers at the end of the quarter, a sequential increase of 195. That’s a little worse than last quarter but in line with what we’ve observed in past quarters, suggesting the company still has decent sales momentum despite the weaker quarter.

It was encouraging to see Procore beat analysts’ revenue expectations this quarter. We were also happy its billings outperformed Wall Street’s estimates. On the other hand, its customer growth stalled. Overall, this print had some key positives. The stock remained flat at $72 immediately after reporting.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| Jul-09 | |

| Jun-17 | |

| Jun-01 | |

| May-21 | |

| May-05 | |

| May-05 | |

| May-05 | |

| Apr-22 | |

| Apr-14 | |

| Mar-16 | |

| Mar-10 | |

| Mar-09 | |

| Feb-28 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite