|

|

|

|

|||||

|

|

|

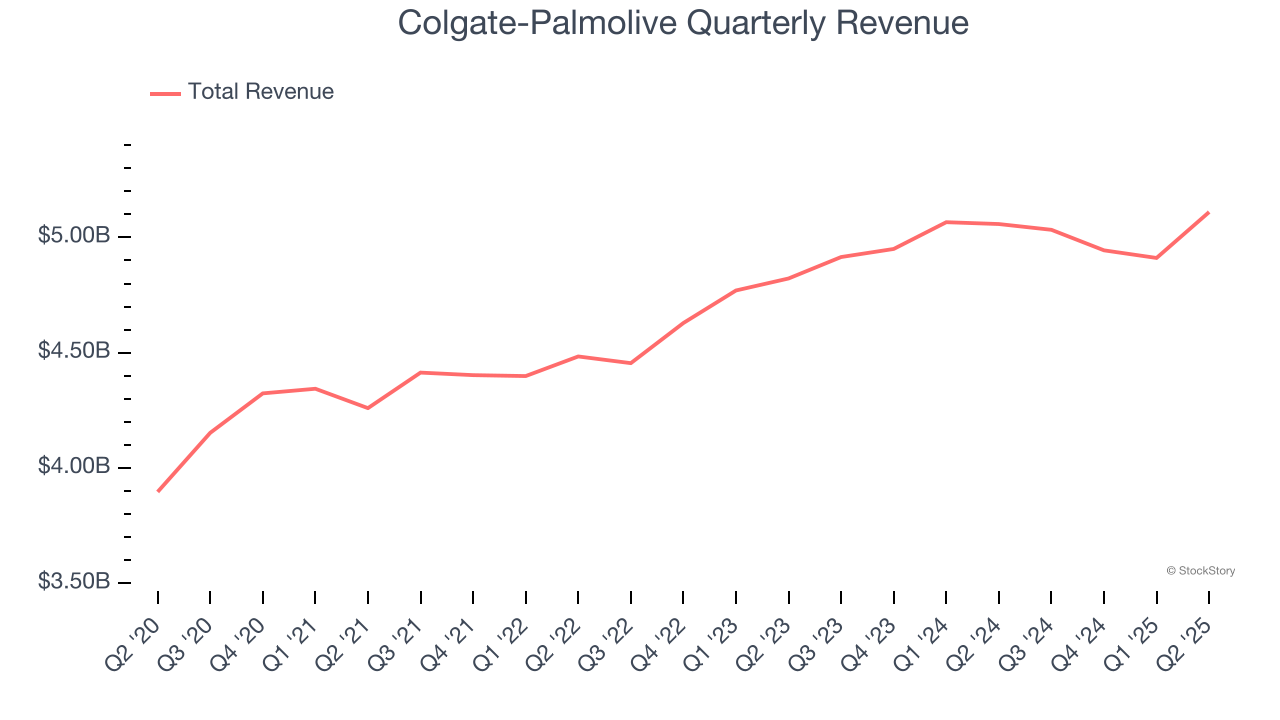

Consumer products company Colgate-Palmolive (NYSE:CL) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 1% year on year to $5.11 billion. Its non-GAAP profit of $0.92 per share was 2.8% above analysts’ consensus estimates.

Is now the time to buy Colgate-Palmolive? Find out by accessing our full research report, it’s free.

Colgate-Palmolive Company (NYSE:CL) today reported results for second quarter 2025. Noel Wallace, Chairman, President and Chief Executive Officer, commented on the Base Business second quarter results, “I am pleased that Colgate-Palmolive people achieved another quarter of net sales, organic sales and earnings per share growth in the face of continued difficult market conditions worldwide, with organic sales growth improving sequentially versus the first quarter despite an even greater negative impact from lower private label pet sales.

Formed after the 1928 combination between toothpaste maker Colgate and soap maker Palmolive-Peet, Colgate-Palmolive (NYSE:CL) is a consumer products company that focuses on personal, household, and pet products.

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $20 billion in revenue over the past 12 months, Colgate-Palmolive is larger than most consumer staples companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. Its size also gives it negotiating leverage with distributors, allowing its products to reach more shelves. However, its scale is a double-edged sword because there are only so many big store chains to sell into, making it harder to find incremental growth. To accelerate sales, Colgate-Palmolive likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Colgate-Palmolive’s 4.2% annualized revenue growth over the last three years was sluggish, but to its credit, consumers bought more of its products.

This quarter, Colgate-Palmolive reported modest year-on-year revenue growth of 1% but beat Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months, similar to its three-year rate. This projection is underwhelming and suggests its newer products will not accelerate its top-line performance yet. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

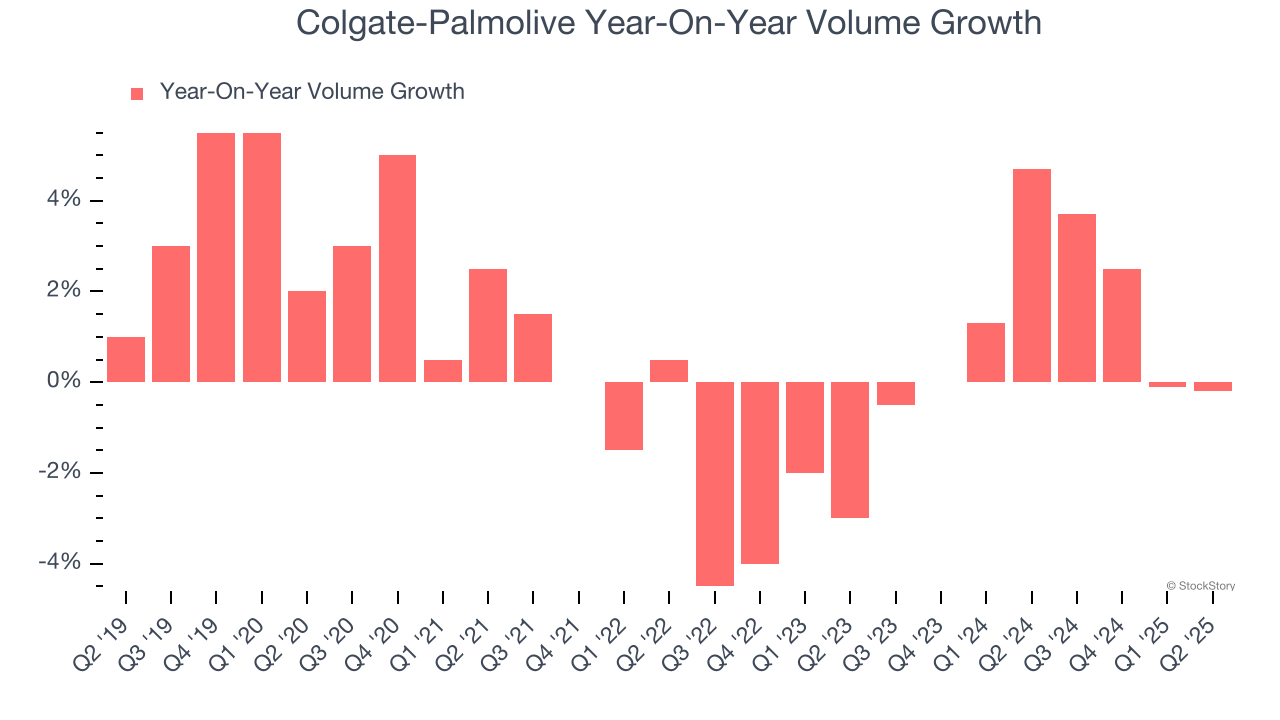

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Colgate-Palmolive generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Colgate-Palmolive’s average quarterly volume growth was a healthy 1.4%. Even with this good performance, we can see that most of the company’s gains have come from price increases by looking at its 6.1% average organic revenue growth. The ability to sell more products while raising prices indicates that Colgate-Palmolive enjoys some degree of inelastic demand.

In Colgate-Palmolive’s Q2 2025, year on year sales volumes were flat. This result was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Colgate-Palmolive can reaccelerate demand for its products.

It was encouraging to see Colgate-Palmolive beat analysts’ revenue expectations this quarter. On the other hand, its EBITDA slightly missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $84.57 immediately following the results.

Is Colgate-Palmolive an attractive investment opportunity at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Apr-04 | |

| Apr-04 | |

| Apr-04 | |

| Apr-04 | |

| Apr-04 | |

| Apr-04 | |

| Apr-04 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite