|

|

|

|

|||||

|

|

|

Clover Health Investments CLOV is slated to release second-quarter 2025 results on Aug. 5, after market close. The Zacks Consensus Estimate for earnings and revenues is pegged at 3 cents per share and $482.5 million, respectively.

The earnings estimate, which has remained stable over the past 30 days, indicates a whopping 200% growth year over year. The Zacks Consensus Estimate for quarterly revenues suggests a year-over-year increase of 35.4%.

The consensus mark for 2025 revenues is pegged at $1.89 billion, implying a rise of 37.7% year over year, and the same for EPS is pinned at 11 cents, suggesting a year-over-year decline of 21.4%. This Medicare Advantage insurer’s earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, delivering an average surprise of 114.58%.

Per our proven model, a stock with a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold), along with a positive Earnings ESP, has higher chances of beating estimates. This is not the case here, as you can see below.

Earnings ESP: CLOV has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Clover Health heads into its second-quarter earnings release next week riding on its stellar first-quarter results with 30% Medicare Advantage (MA) membership growth and a 279% year-over-year surge in adjusted EBITDA. The upcoming results are expected to reflect continued benefits from its tech-enabled care delivery model and strategic member onboarding efforts.

A key tailwind that is likely to have sustained performance is the expansion and deeper integration of Clover Assistant (CA), its AI-powered clinical decision support tool. CA’s role in early disease detection and chronic care management has already shown quantifiable outcomes.

A May whitepaper from its subsidiary, Counterpart Health, highlighted an 18% reduction in hospitalizations and 25% lower 30-day readmissions in congestive heart failure (CHF) patients managed by CA-equipped PCPs. These results are not only clinically meaningful but may also translate into cost efficiencies — potentially easing pressure on the company’s Insurance Benefit Expense Ratio (“BER”), which was 86.1% in the first quarter.

Member growth, particularly in core markets like New Jersey, remains robust on the back of strong plan retention and disciplined benefit design. New members onboarded during the AEP and OEP seasons were reportedly utilizing care at expected levels, reinforcing the strength of cohort management strategies. This is likely to have resulted in increased sales during the soon-to-be-reported quarter.

On the technology commercialization front, CLOV’s Counterpart Health continues to scale, bringing the Assistant’s capabilities to non-Clover plans via SaaS-style arrangements. Management remains optimistic about its long-term potential. However, this is unlikely to have had a material impact in the second quarter.

Investors are likely to ask questions on updates about utilization trends, HCC risk adjustment transitions and the sustainability of SG&A leverage during the second-quarter earnings call.

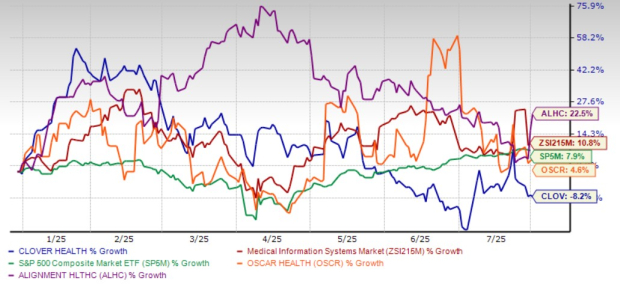

On a year-to-date basis, shares of CLOV have declined 8.2%, underperforming its close peers, Alignment Healthcare ALHC and Oscar Health OSCR and the Medical Info Systems sector.

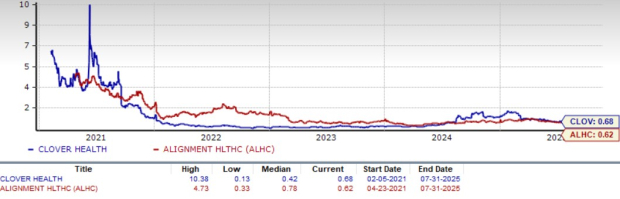

In terms of valuation, Clover Health trades at a forward 12-month P/S of 0.65 — above Alignment Healthcare (0.62) and Oscar Health (0.31). Despite Alignment Healthcare and Oscar Health offering lower multiples, CLOV’s premium reflects stronger growth expectations.

CLOV vs ALHC

CLOV vs OSCR

Clover Health continues to demonstrate solid execution with strong MA membership growth, improved clinical outcomes via Clover Assistant and expanding Counterpart Health traction. Its near-term upside appears fairly priced in. The company’s profitability remains modest, with Insurance BER still elevated and full-year gains partly dependent on favorable seasonality and continued cost control.

Additionally, while Counterpart holds promise, material revenue contribution is still evolving. Given these factors and pending confirmation of sustainable margin improvement in the second half of 2025, investors should continue to hold the stock. However, new investors may await clearer visibility into operating leverage and execution on non-insurance revenues before adding the stock to their portfolio.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-17 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-08 | |

| Jul-07 | |

| Jul-02 | |

| Jul-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite