|

|

|

|

|||||

|

|

|

Ralph Lauren Corporation RL is set to report first-quarter fiscal 2026 results on Aug. 7, before market open. The Zacks Consensus Estimate for revenues is pegged at $1.65 billion, which indicates growth of 8.8% from the year-ago quarter’s reported figure.

The consensus estimate for earnings is pegged at $3.45 per share, which suggests growth of 27.8% from the year-earlier actual. The consensus mark for earnings has increased 0.6% in the past seven days.

In the last reported quarter, the company’s bottom line surpassed the Zacks Consensus Estimate by 13.5%. Ralph Lauren has a trailing four-quarter earnings surprise of 9%, on average.

Ralph Lauren’s quarterly performance is likely to have benefited from a strong brand presence, a diverse product portfolio and expanding e-commerce capabilities, which have been strengthening its market position. The company's growing store footprint, coupled with its focus on innovation and integration of AI technology, reflects its commitment to staying ahead in the evolving fashion industry and achieving sustained growth.

RL has been experiencing growth in its digital and omnichannel business through investments in mobile, omnichannel and fulfillment. The company has been adding consumers to its direct-to-consumer business, highlighting the effectiveness of its strategies and the strong appeal of its products, which is expected to have aided the fiscal first-quarter performance. Such positives are expected to be reflected in its top and bottom-line results.

On the last reported quarter’s earnings call, management was optimistic about business momentum and executing the long-term game plan, continuing to elevate the brand and strengthen its positioning in the marketplace. The company expects revenues in the first half of fiscal 2026 to increase in the mid-single digits, driven by growth in its Asia and Europe businesses.

For the fiscal first quarter, management anticipates revenues to grow year over year in the high-single digits on a constant-currency basis. The operating margin is likely to expand 150-200 bps in constant currency, driven by a gross margin expansion and slight operating expense leverage. Foreign currency is expected to have a minimal impact on the gross and operating margins.

Ralph Lauren Corporation price-eps-surprise | Ralph Lauren Corporation Quote

However, Ralph Lauren has been facing challenges stemming from its extensive international exposure, particularly due to fluctuating foreign exchange rates. The company's global footprint makes it vulnerable to currency volatility and the strengthening U.S. dollar has emerged as a notable financial headwind. This currency shift has adversely impacted its revenues and earnings.

RL has been witnessing a tough operating landscape, including the ongoing macroeconomic and geopolitical uncertainties, inflationary pressures, consumer-spending-related headwinds, supply-chain disruptions, tariff-related pressures, and foreign currency volatility. On the last reported quarter’s earnings call, the company noted no change in its underlying business trends from fourth-quarter fiscal 2025 into early first-quarter fiscal 2026.

Ralph Lauren has been struggling with macro challenges and inflationary headwinds, apart from higher operating costs, for a while now. The macro indicators, including the tariff impacts, weakening consumer confidence, a higher risk of a broader consumer pullback, and a highly uncertain global operating landscape, suggest caution for the upcoming quarters.

Our proven model conclusively predicts an earnings beat for Ralph Lauren this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is exactly the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Ralph Lauren currently has an Earnings ESP of +0.75% and a Zacks Rank of 2.

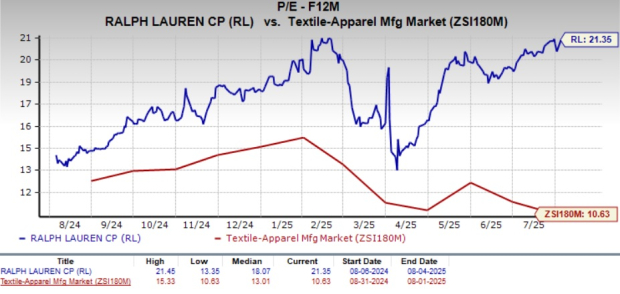

Ralph Lauren's stock is trading at a premium valuation relative to the industry. Going by the price-to-earnings ratio, the stock is currently trading at 21.35X on a forward 12-month basis, higher than its median of 18.07X and the Textile - Apparel industry’s 10.63X.

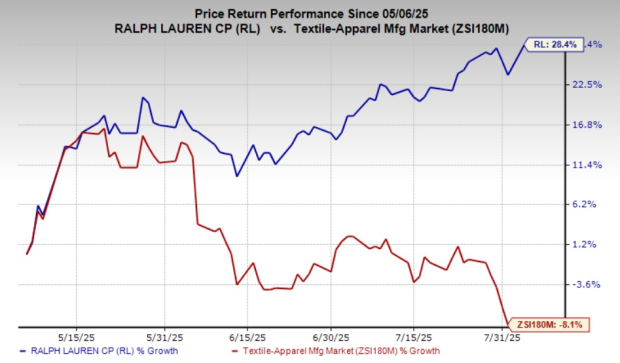

The recent market movements show that RL shares have risen 28.4% in the past three months against the industry's 8.1% decline.

Here are some companies that, according to our model, have the right combination of elements to beat on earnings this reporting cycle.

Central Garden & Pet CENT has an Earnings ESP of +6.98% and currently flaunts a Zacks Rank of 1. CENT is likely to register a bottom-line increase when it reports third-quarter fiscal 2025 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $987.1 million, indicating a 0.9% decline from the figure reported in the prior-year quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Central Garden’s earnings is pegged at $1.34 per share, implying a 1.5% increase from the year-ago quarter’s actual. The consensus mark for earnings has increased 14.5% in the past 30 days. CENT delivered an earnings surprise of 206.6% in the last quarter.

Wolverine World Wide WWW has an Earnings ESP of +5.75% and a Zacks Rank of 2 at present. WWW is likely to register top and bottom-line growth when it releases second-quarter 2025 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $446.5 million, which implies growth of 5% from the figure reported in the year-ago quarter.

The consensus estimate for WWW’s quarterly earnings has been unchanged in the past 30 days at 22 cents per share, implying growth of 46.7% from the year-ago quarter’s reported number. Wolverine delivered an earnings surprise of 38.6%, on average, in the trailing four quarters.

Planet Fitness PLNT has an Earnings ESP of +0.81% and a Zacks Rank of 2 at present. PLNT is likely to register top and bottom-line growth when it releases second-quarter 2025 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $334.3 million, which implies a rise of 11.1% from the figure reported in the year-ago quarter.

The consensus estimate for Planet Fitness’ quarterly earnings has moved up by a penny in the past 30 days to 79 cents per share, implying growth of 11.3% from the year-ago quarter’s reported number. PLNT delivered an earnings surprise of 6.9%, on average, in the trailing four quarters.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 | |

| Mar-03 | |

| Mar-03 | |

| Mar-03 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite