|

|

|

|

|||||

|

|

|

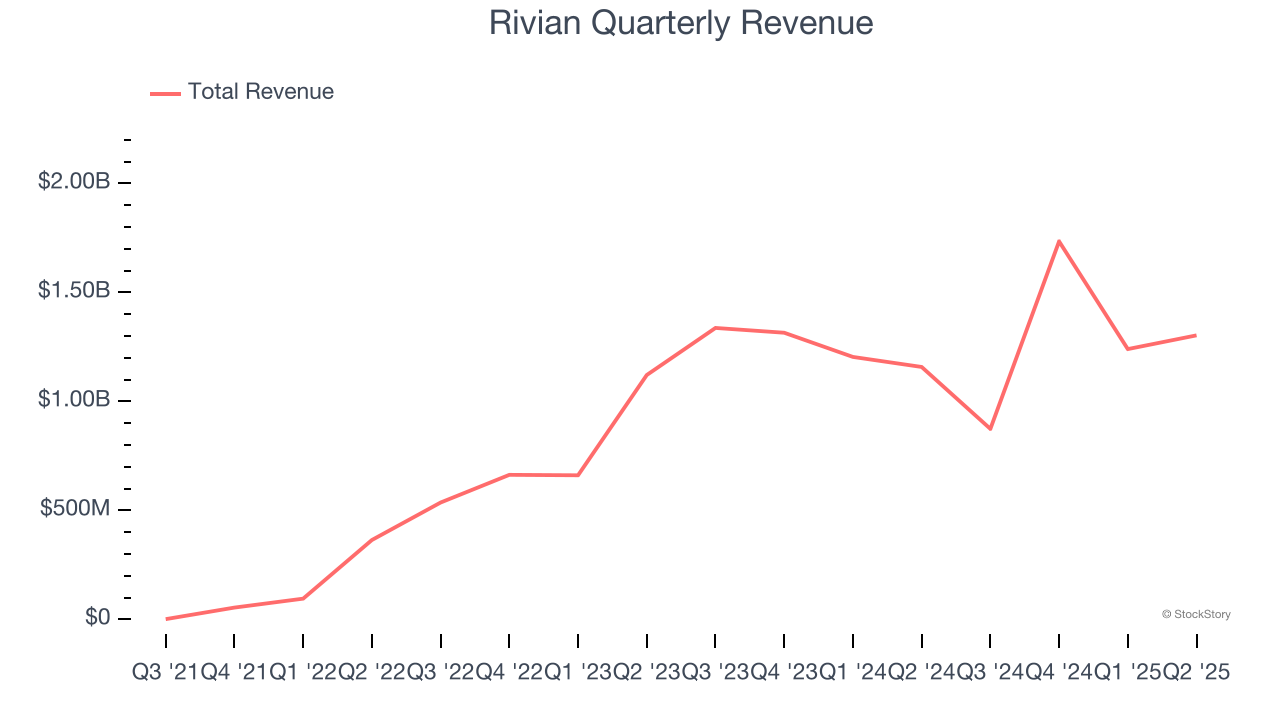

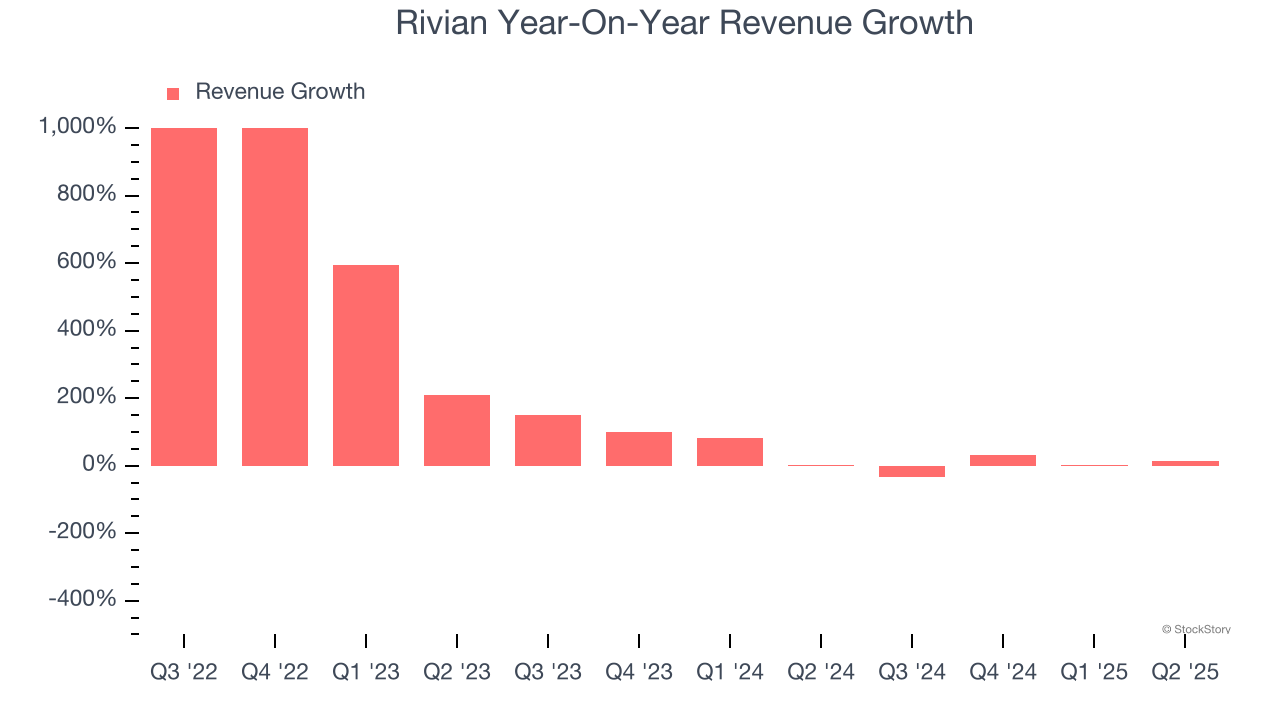

Electric vehicle manufacturer Rivian (NASDAQ:RIVN) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 12.5% year on year to $1.30 billion. Its non-GAAP loss of $0.80 per share was 26% below analysts’ consensus estimates.

Is now the time to buy Rivian? Find out by accessing our full research report, it’s free.

The manufacturer of Amazon’s delivery trucks, Rivian (NASDAQ:RIVN) designs, manufactures, and sells electric vehicles and commercial delivery vans.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Rivian’s sales grew at an incredible 262% compounded annual growth rate over the last three years. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Rivian’s annualized revenue growth of 31.5% over the last two years is below its three-year trend, but we still think the results suggest healthy demand.

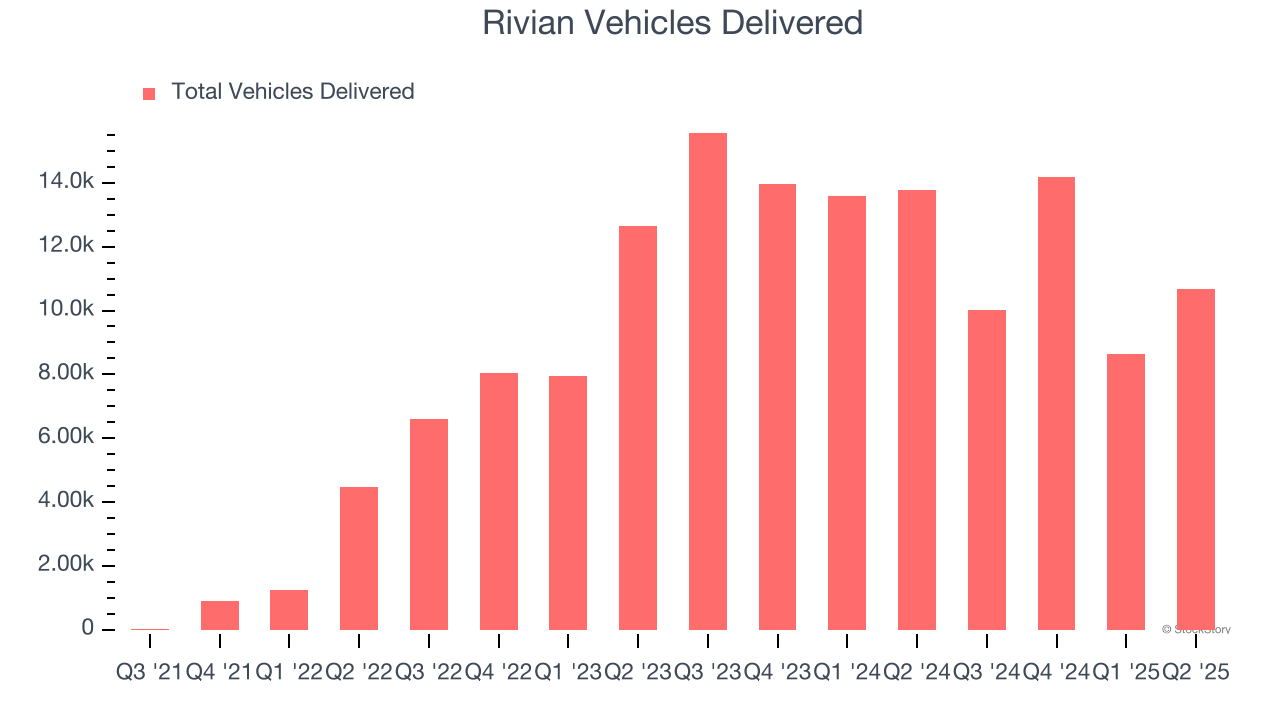

We can better understand the company’s revenue dynamics by analyzing its number of vehicles delivered, which reached 10,661 in the latest quarter. Over the last two years, Rivian’s vehicles delivered grew by 11.1% annually. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Rivian reported year-on-year revenue growth of 12.5%, and its $1.30 billion of revenue exceeded Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to grow 12.5% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and implies the market sees success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

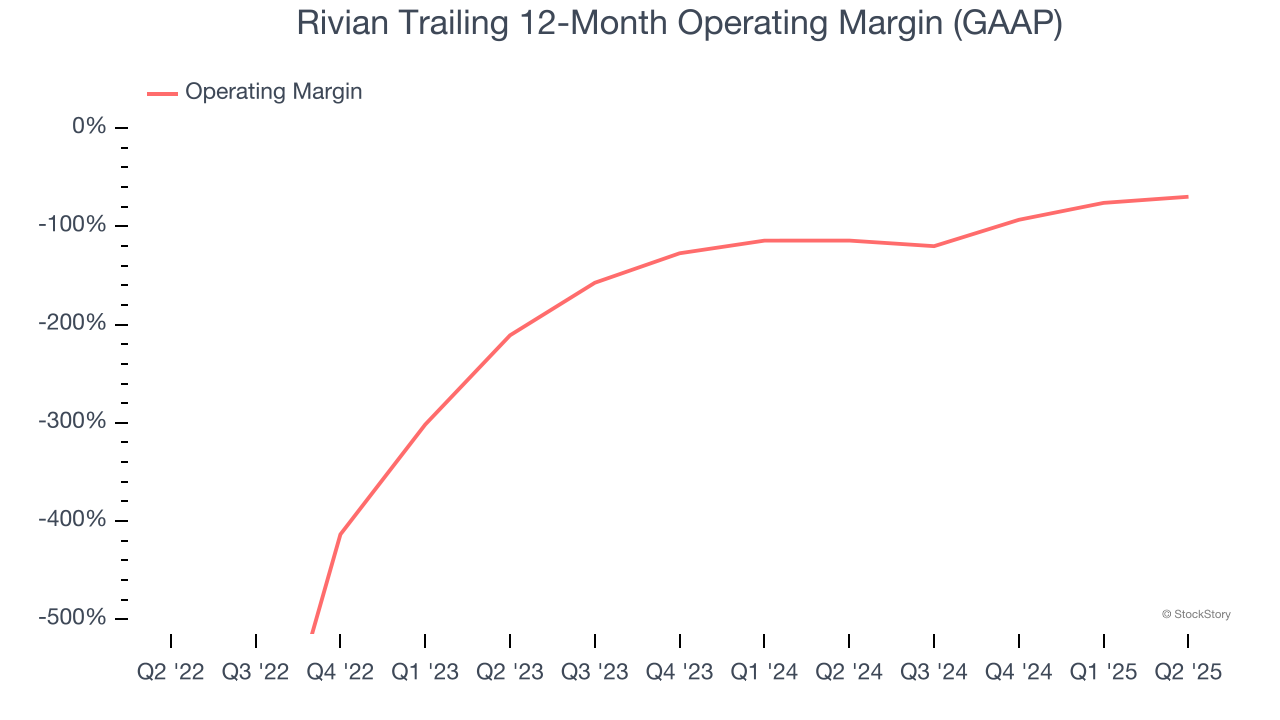

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Rivian’s high expenses have contributed to an average operating margin of negative 162% over the last four years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Rivian’s operating margin rose over the last four years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q2, Rivian generated a negative 85.5% operating margin.

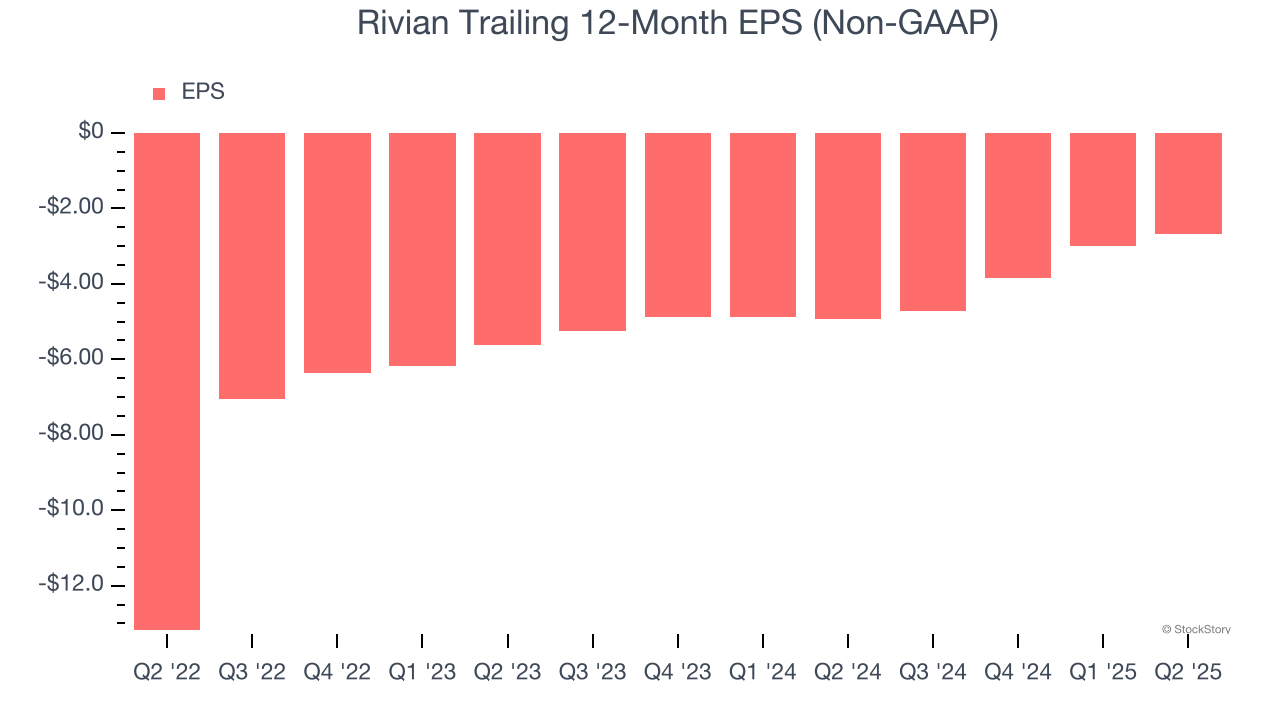

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Rivian’s full-year earnings are still negative, it reduced its losses and improved its EPS by 31.1% annually over the last two years.

In Q2, Rivian reported adjusted EPS at negative $0.80, up from negative $1.13 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Rivian to improve its earnings losses. Analysts forecast its full-year EPS of negative $2.68 will advance to negative $2.43.

We enjoyed seeing Rivian beat analysts’ revenue expectations this quarter. On the other hand, its full-year EBITDA guidance missed and its EBITDA fell short of Wall Street’s estimates, showing that while there is topline strength, the growth is not as profitable as expected. Overall, this was a weaker quarter. The stock traded down 3.8% to $11.72 immediately after reporting.

The latest quarter from Rivian’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| 3 hours | |

| 4 hours | |

| 9 hours | |

| 15 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite