|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

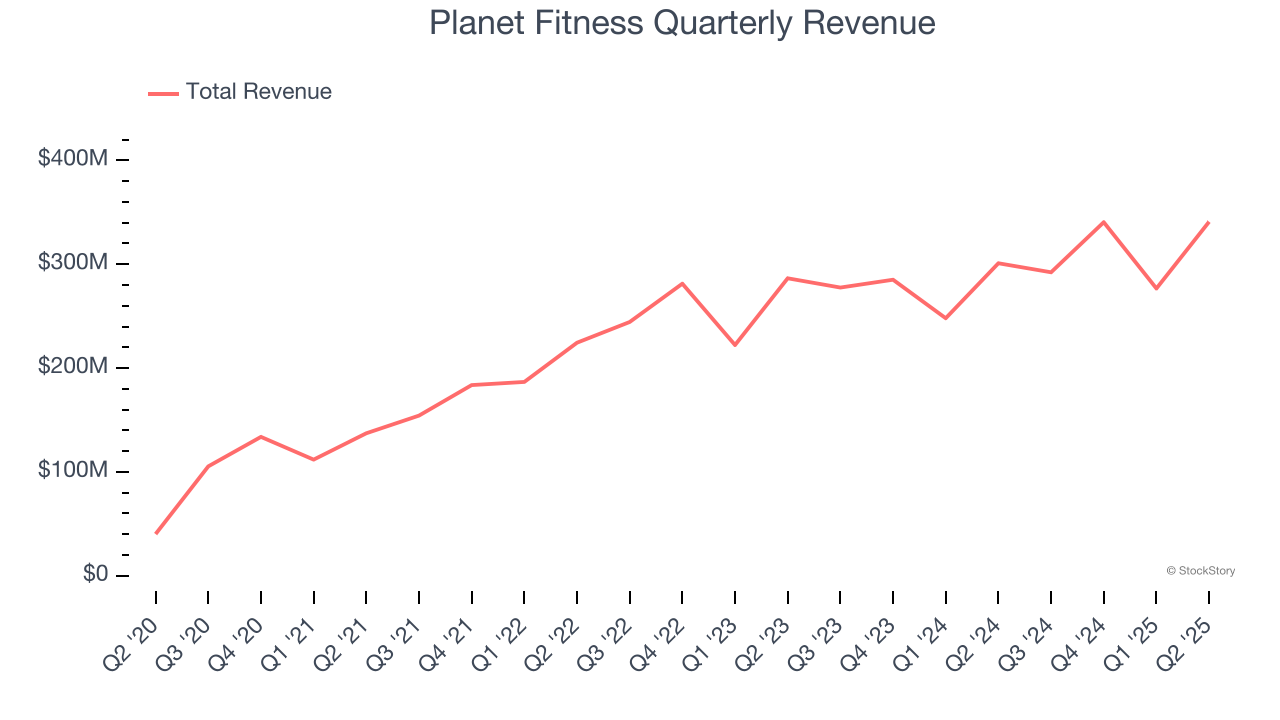

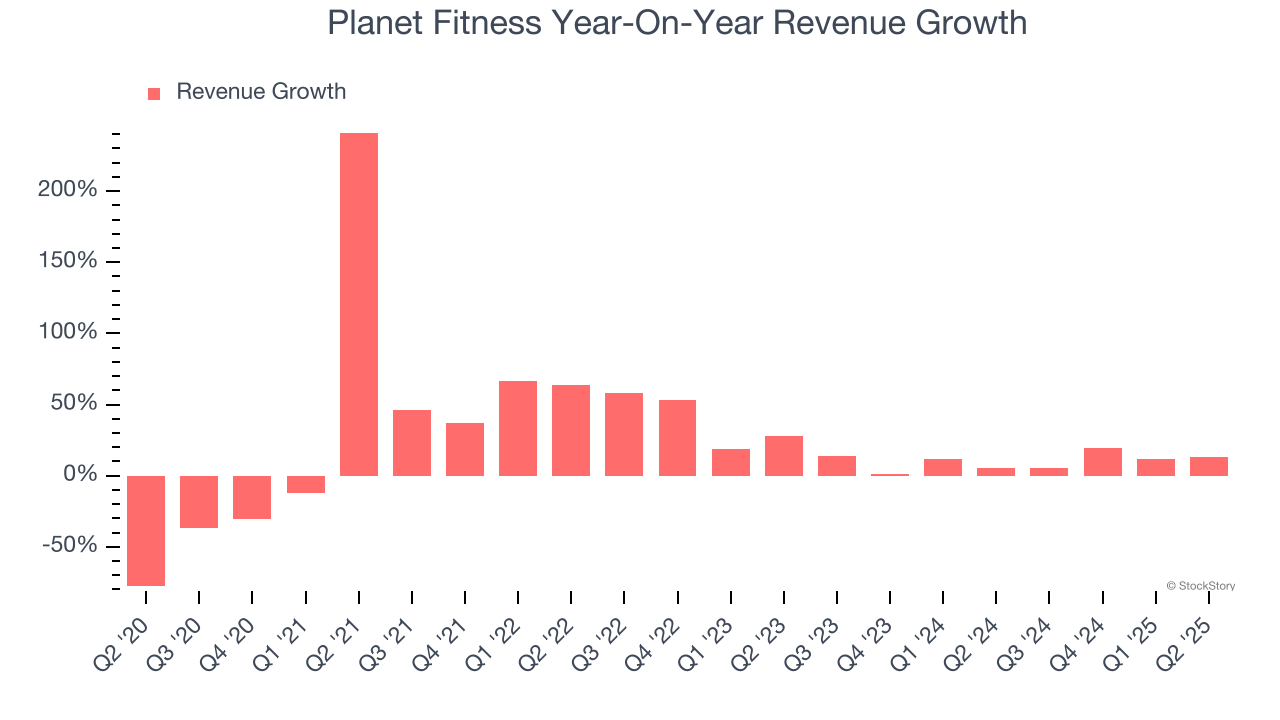

Inclusive gym franchise company (NYSE:PLNT) reported Q2 CY2025 results topping the market’s revenue expectations, with sales up 13.3% year on year to $340.9 million. Its non-GAAP profit of $0.86 per share was 8.7% above analysts’ consensus estimates.

Is now the time to buy Planet Fitness? Find out by accessing our full research report, it’s free.

"Today marks the 10-year anniversary for Planet Fitness as a public company. Over the past decade, through a steadfast commitment to our mission and strategy, we've added nearly 14 million members, expanded our global footprint by more than 1,700 clubs, and established a presence in all 50 states and four additional countries. While we are proud of our accomplishments, we believe there is even greater opportunity ahead. As consumers increasingly prioritize health and well-being, Planet Fitness is well-positioned to meet this demand with our judgement-free, high-quality, and affordable fitness experience. Early momentum in programs like our High School Summer Pass – which is now in its fifth year and outpacing prior-year sign-ups and workouts – underscores our potential," said Colleen Keating, Chief Executive Officer.

Founded by two brothers who purchased a struggling gym, Planet Fitness (NYSE:PLNT) is a gym franchise that caters to casual fitness users by providing a friendly and inclusive atmosphere.

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Planet Fitness’s sales grew at a solid 18.9% compounded annual growth rate over the last five years. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Planet Fitness’s recent performance shows its demand has slowed as its annualized revenue growth of 9.9% over the last two years was below its five-year trend. Note that COVID hurt Planet Fitness’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

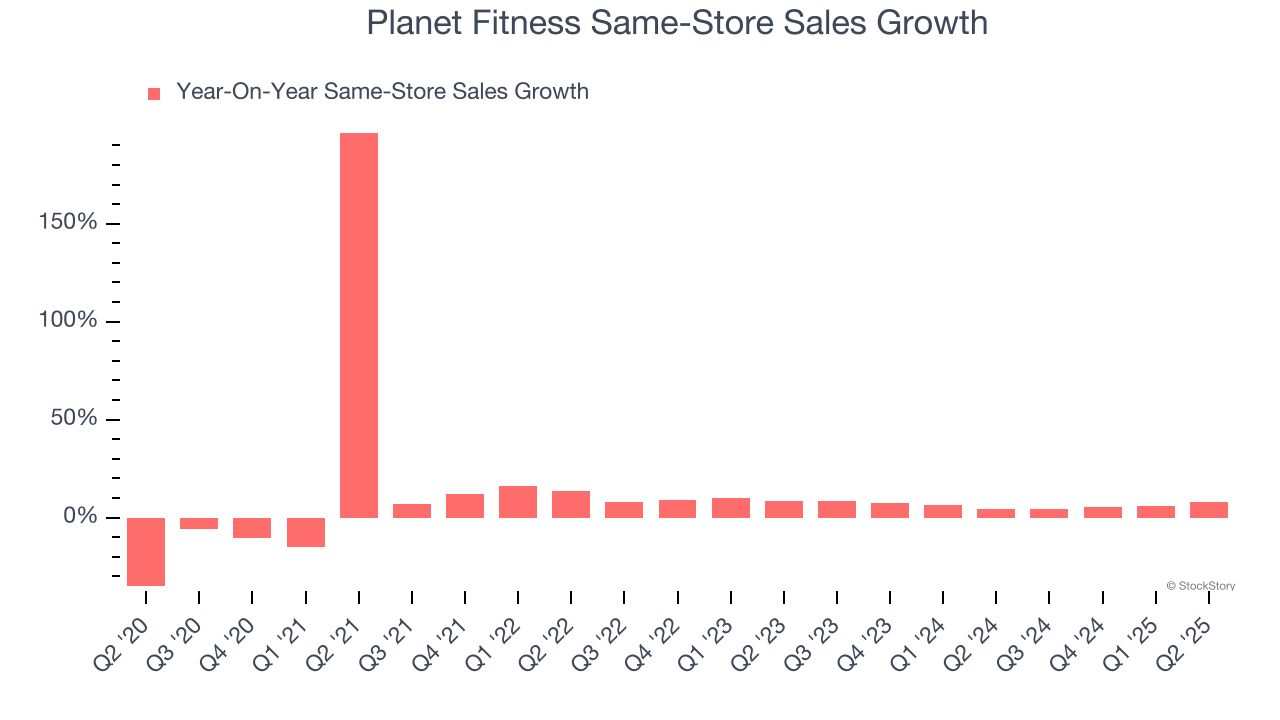

Planet Fitness also reports same-store sales, which show how much revenue its established locations generate. Over the last two years, Planet Fitness’s same-store sales averaged 6.3% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Planet Fitness reported year-on-year revenue growth of 13.3%, and its $340.9 million of revenue exceeded Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 10% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not catalyze better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

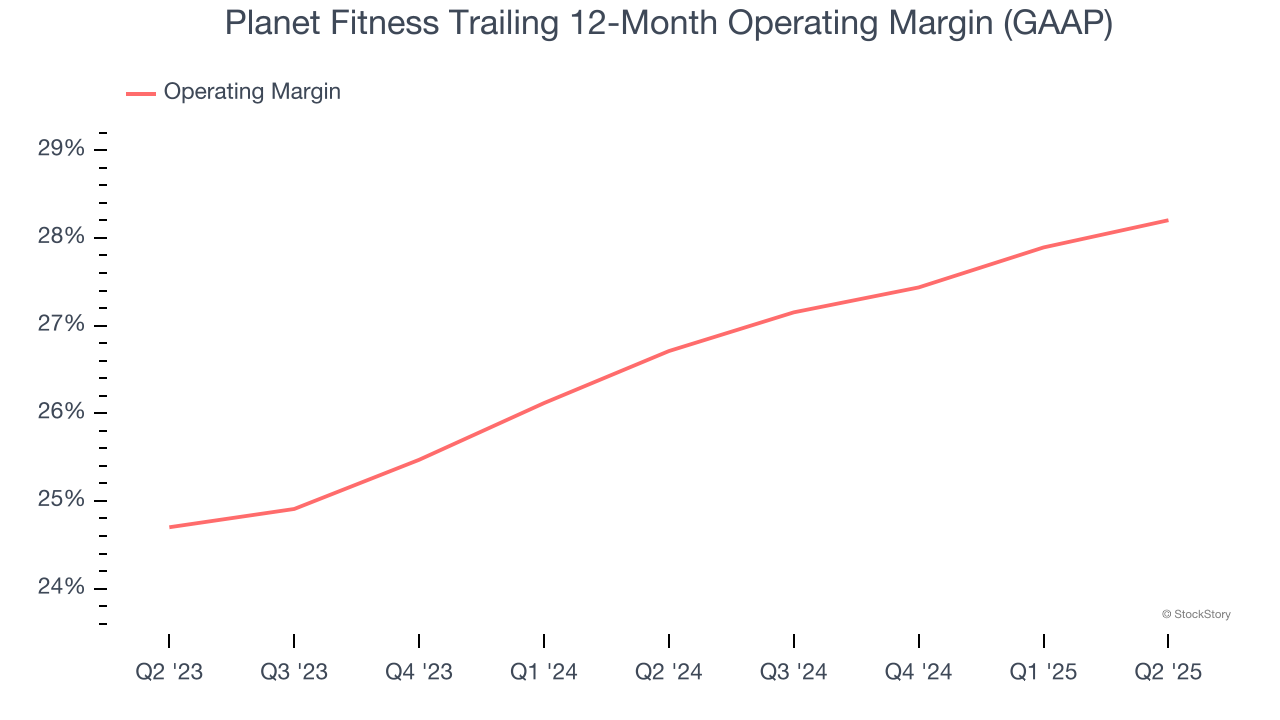

Planet Fitness’s operating margin has risen over the last 12 months and averaged 27.5% over the last two years. On top of that, its profitability was elite for a consumer discretionary business thanks to its efficient cost structure and economies of scale.

This quarter, Planet Fitness generated an operating margin profit margin of 30%, up 1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

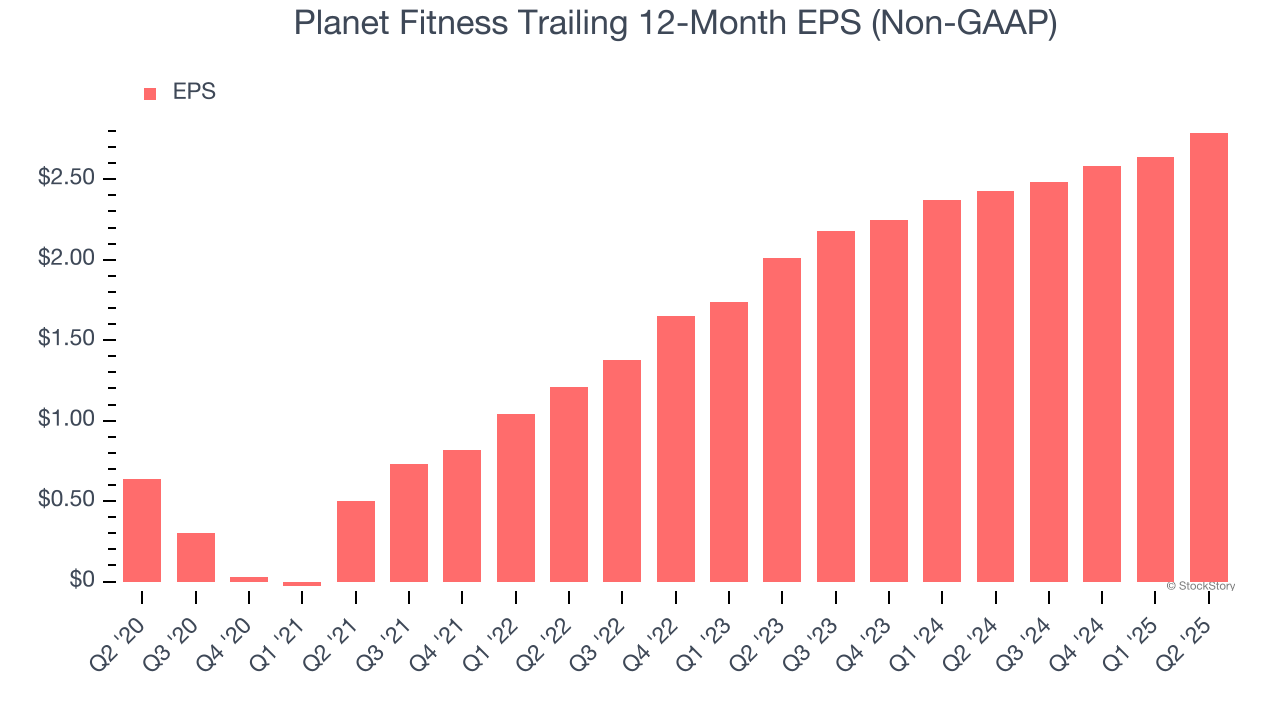

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Planet Fitness’s EPS grew at an astounding 34.2% compounded annual growth rate over the last five years, higher than its 18.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q2, Planet Fitness reported adjusted EPS at $0.86, up from $0.71 in the same quarter last year. This print beat analysts’ estimates by 8.7%. Over the next 12 months, Wall Street expects Planet Fitness’s full-year EPS of $2.79 to grow 13.6%.

We enjoyed seeing Planet Fitness beat analysts’ same-store sales expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 2.2% to $111.82 immediately after reporting.

Indeed, Planet Fitness had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-19 | |

| Feb-19 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-13 | |

| Feb-10 | |

| Feb-09 | |

| Jan-28 | |

| Jan-23 | |

| Jan-20 | |

| Jan-16 | |

| Jan-16 | |

| Jan-15 | |

| Jan-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite