|

|

|

|

|||||

|

|

|

New Elite Feature: Compare relative returns, fundamentals, and sector rankings head-to-head.

ASML Holding ASML and Applied Materials AMAT are two of the biggest names in the semiconductor equipment industry, playing critical roles in the chipmaking process. ASML is the global leader in lithography systems, especially in the high-end extreme ultraviolet (EUV) technology, while AMAT holds a dominant position in deposition, etching and process control.

As the semiconductor industry continues to grow on the back of artificial intelligence (AI), automotive and cloud computing trends, investors might be thinking: Which of these two industry giants looks like the better buy right now?

ASML Holding is widely regarded as the most important company in the global semiconductor value chain due to its monopoly in EUV lithography. This cutting-edge technology is essential for manufacturing the smallest and most advanced chips used in AI accelerators, high-performance computing and smartphones. Demand for EUV systems remains robust, with top customers like Taiwan Semiconductor Manufacturing, Samsung and Intel investing heavily in advanced node development.

Financially, ASML Holding is performing well. In the second quarter of 2025, it reported revenue growth of 23% and a 47% jump in earnings per share. Despite strong quarterly results, management’s commentary about next year’s forecasts raises concerns about its growth prospects.

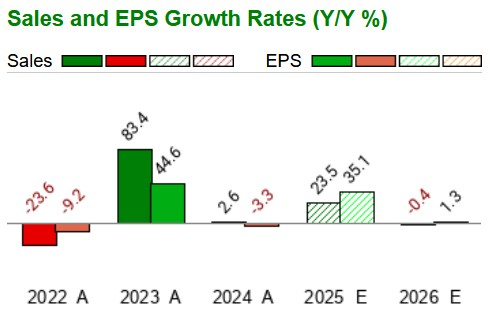

On the second-quarter earnings call, management backed away from earlier confidence about growth in 2026. Previously, ASML Holding had expected demand to keep rising, especially with AI fueling more chip production. However, on the second-quarter call, the company said that it “cannot confirm growth in 2026,” pointing to customer hesitation and ongoing market uncertainty.

During the call, ASML Holding acknowledged that ongoing U.S.-China tariff discussions, including the Section 232 tariff review, are negatively impacting customer capital spending timelines. This hesitation may delay orders and revenue recognition in late 2025 and into 2026, casting doubt on near-term growth continuity. Analysts are also pessimistic about the company’s prospects in 2026, as reflected by the Zacks Consensus Estimate.

Additionally, ASML Holding issued disappointing guidance for the third quarter. The company expects third-quarter revenues between €7.4 billion and €7.9 billion, indicating year-over-year growth of 14.6% at the midpoint. This forecasted growth rate is significantly lower than the 46% increase registered in the first quarter and 23.2% in the second quarter.

ASML Holding expects the third-quarter gross margin in the 50-52% range, depicting a significant decline from 53.7% in the second quarter. This sequential decrease is expected mainly due to margin-dilutive High NA system revenues and fewer upgrade orders.

Applied Materials benefits from a more diversified portfolio within semiconductor manufacturing equipment. Unlike ASML, which is centered around lithography, Applied’s tools are used across deposition, etch and metrology processes, giving it broader exposure to different parts of the chip production chain. This diversity enables the company to better handle industry fluctuations and win share across logic, memory and packaging markets.

Applied Materials’ long-term growth prospects remain highly compelling, thanks to its leadership in AI-driven semiconductor technology. AI chip demand is fueling a new wave of semiconductor investments, and Applied Materials is positioned at the forefront of this trend. The company’s expertise in gate-all-around (GAA) transistors, high-bandwidth memory (HBM) and advanced packaging makes it a critical supplier for AI chipmakers.

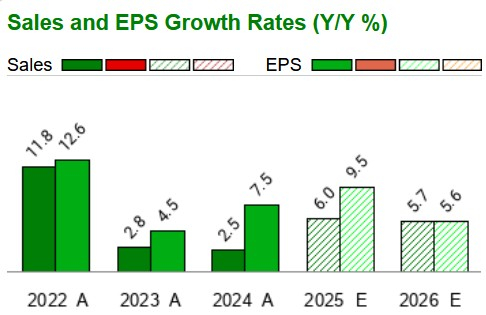

In fiscal 2024, Applied Materials’ revenues from advanced semiconductor nodes surpassed $2.5 billion. Management expects this figure to double in fiscal 2025, fueled by increasing customer adoption of GAA and backside power delivery solutions.

These factors are strongly driving Applied Materials’ top and bottom-line growth. In the last reported results for the second quarter of fiscal 2025, its non-GAAP EPS surged 14.4% on 6.8% higher revenues. The company’s guidance for the third quarter indicates year-over-year growth of 6.2% in revenues and a 10.8% increase in non-GAAP EPS.

Analysts also seem to be optimistic about the company’s prospects in the near term. The Zacks Consensus Estimate for fiscal 2025 and 2026 indicates steady growth momentum.

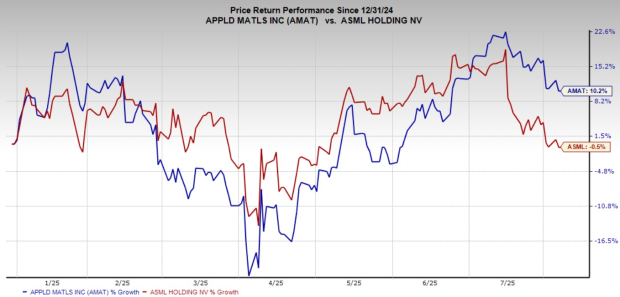

Year to date, shares of ASML Holding have fallen 0.5%, while Applied Materials has risen 10.2%.

On the valuation front, ASML is trading at a forward earnings multiple of 24.33, higher than AMAT’s 18.14X. While both companies are of high quality, Applied Materials looks more reasonably priced, especially considering its stronger near-term momentum.

While both companies are essential to the future of semiconductor manufacturing, Applied Materials stands out as the better investment option at this time. It offers stronger near-term earnings stability, broader product exposure and more attractive valuation. ASML remains a long-term winner, thanks to its unmatched lithography technology, but its rich valuation and short-term headwinds make it less appealing than AMAT.

Additionally, AMAT carries a Zacks Rank #2 (Buy), making it a clear winner over ASML, which has a Zacks Rank #4 (Sell) at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| 14 hours | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-02 | |

| Jun-02 | |

| Jun-01 | |

| May-28 | |

| May-28 | |

| May-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite