|

|

|

|

|||||

|

|

|

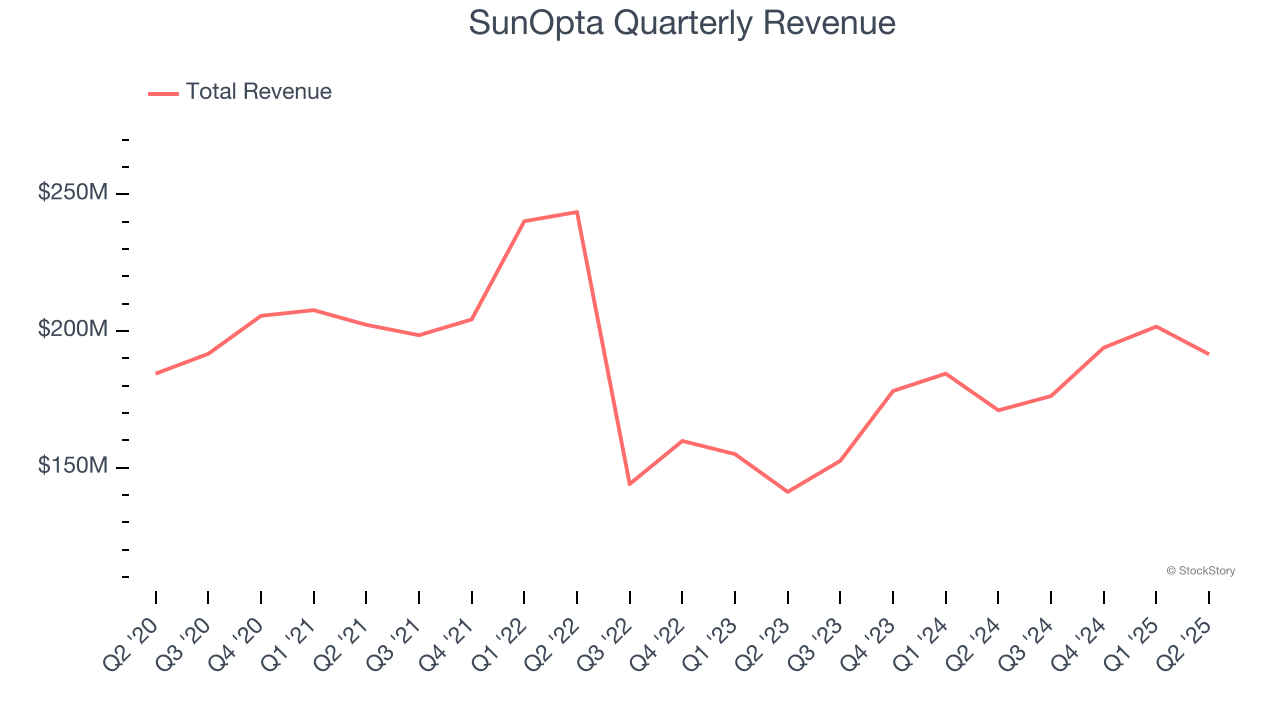

Plant-based food and beverage company SunOpta (NASDAQ:STKL) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 12% year on year to $191.5 million. The company’s full-year revenue guidance of $810 million at the midpoint came in 1.5% above analysts’ estimates. Its non-GAAP profit of $0.04 per share was $0.02 above analysts’ consensus estimates.

Is now the time to buy SunOpta? Find out by accessing our full research report, it’s free.

Committed to clean-label foods, SunOpta (NASDAQ:STKL) is a sustainability-focused food and beverage company specializing in the sourcing, processing, and packaging of organic products.

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $763.2 million in revenue over the past 12 months, SunOpta is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, SunOpta’s demand was weak over the last three years. Its sales fell by 4.9% annually despite consumers buying more of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, SunOpta reported year-on-year revenue growth of 12%, and its $191.5 million of revenue exceeded Wall Street’s estimates by 3.1%.

Looking ahead, sell-side analysts expect revenue to grow 8.7% over the next 12 months, an acceleration versus the last three years. This projection is commendable and implies its newer products will spur better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

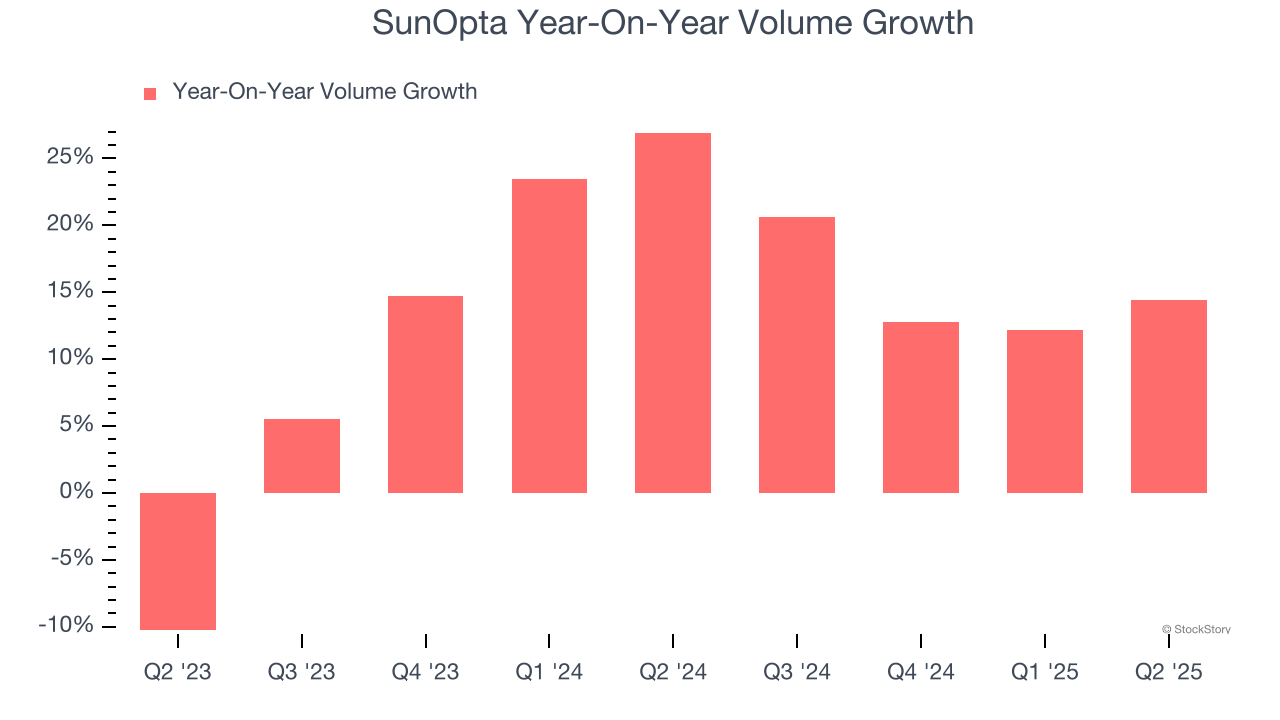

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

SunOpta’s average quarterly volume growth of 16.3% over the last two years has beaten the competition by a long shot. This is great because companies with significant volume growth are needles in a haystack in the stable consumer staples sector.

In SunOpta’s Q2 2025, sales volumes jumped 14.4% year on year. This result shows the business is staying on track, but the deceleration suggests growth is getting harder to come by.

We were impressed by how significantly SunOpta blew past analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its gross margin missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 7.1% to $5.55 immediately after reporting.

Sure, SunOpta had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| May-01 | |

| Apr-30 | |

| Apr-22 | |

| Apr-17 | |

| Apr-10 | |

| Apr-01 | |

| Mar-24 | |

| Mar-19 | |

| Mar-18 | |

| Mar-10 | |

| Mar-03 | |

| Mar-02 | |

| Feb-16 | |

| Feb-09 | |

| Feb-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite