|

|

|

|

|||||

|

|

|

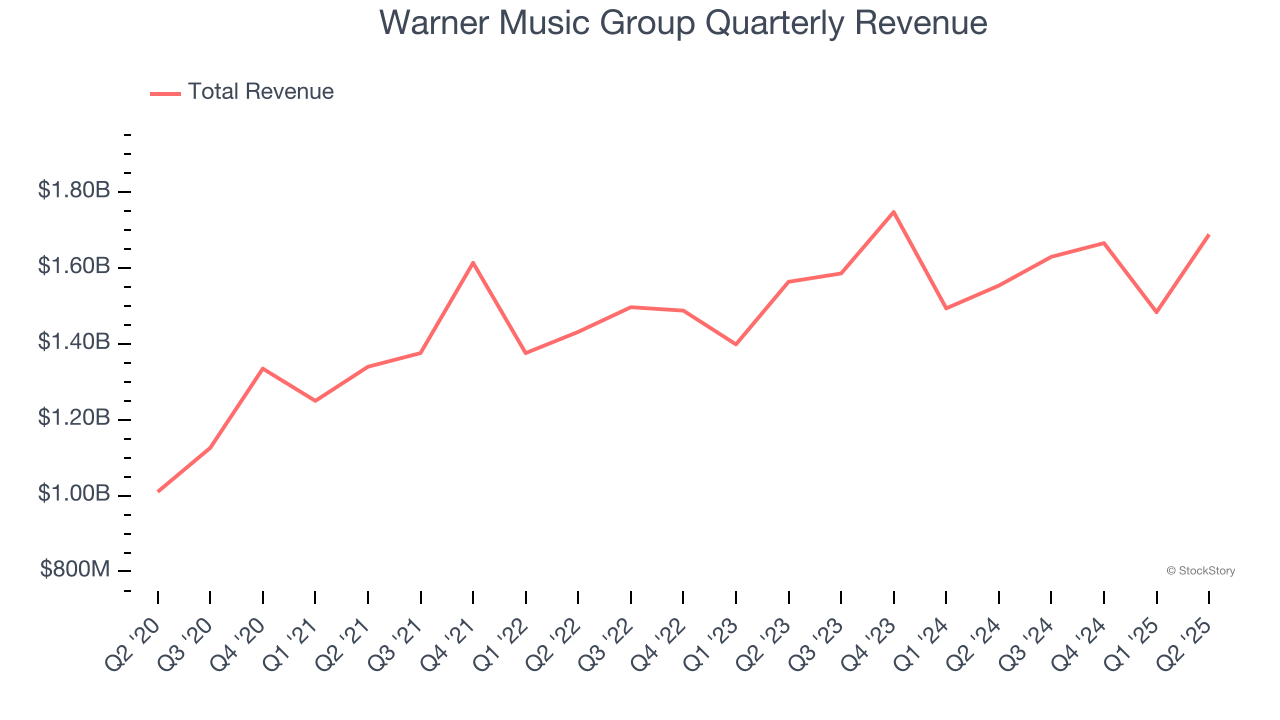

Global music entertainment company Warner Music Group (NASDAQ:WMG) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 8.7% year on year to $1.69 billion. Its GAAP loss of $0.03 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Warner Music Group? Find out by accessing our full research report, it’s free.

“This quarter we delivered massive chart hits, breakthrough stars, strong revenue growth, and market share gains…all of which show our strategy is working,” said Robert Kyncl, CEO, Warner Music Group.

Launching the careers of legendary artists like Frank Sinatra, Warner Music Group (NASDAQ:WMG) is a music company managing a diverse portfolio of artists, recordings, and music publishing services worldwide.

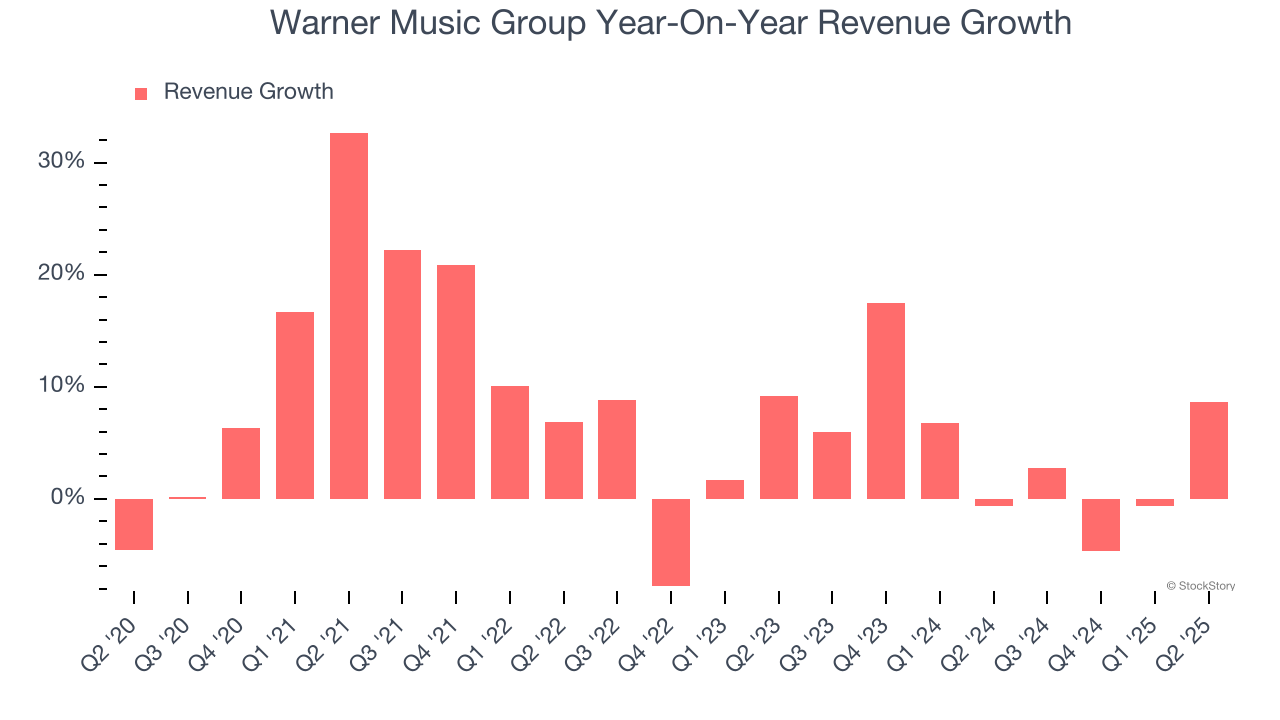

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Warner Music Group grew its sales at a sluggish 7.7% compounded annual growth rate. This was below our standard for the consumer discretionary sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Warner Music Group’s recent performance shows its demand has slowed as its annualized revenue growth of 4.3% over the last two years was below its five-year trend.

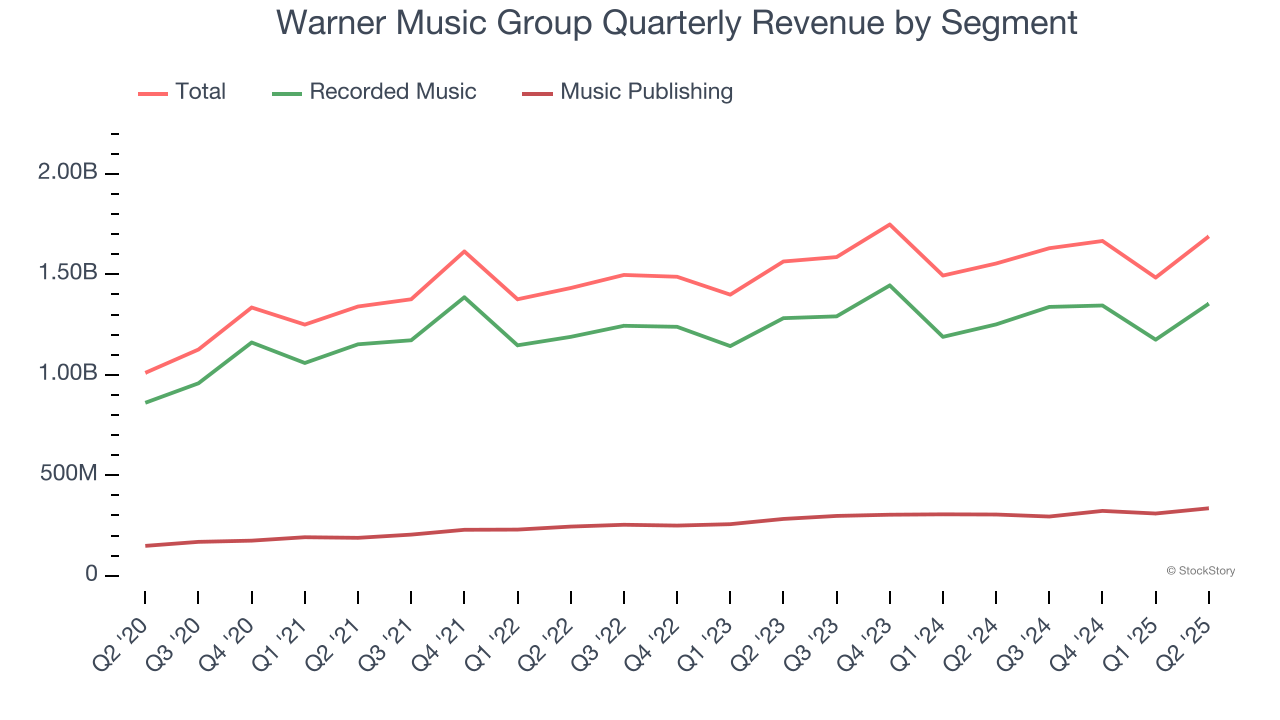

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Recorded Music and Music Publishing, which are 80.2% and 19.9% of revenue. Over the last two years, Warner Music Group’s Recorded Music revenue (new music production) averaged 3.2% year-on-year growth while its Music Publishing revenue (royalties from catalog music) averaged 10.3% growth.

This quarter, Warner Music Group reported year-on-year revenue growth of 8.7%, and its $1.69 billion of revenue exceeded Wall Street’s estimates by 6.2%.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

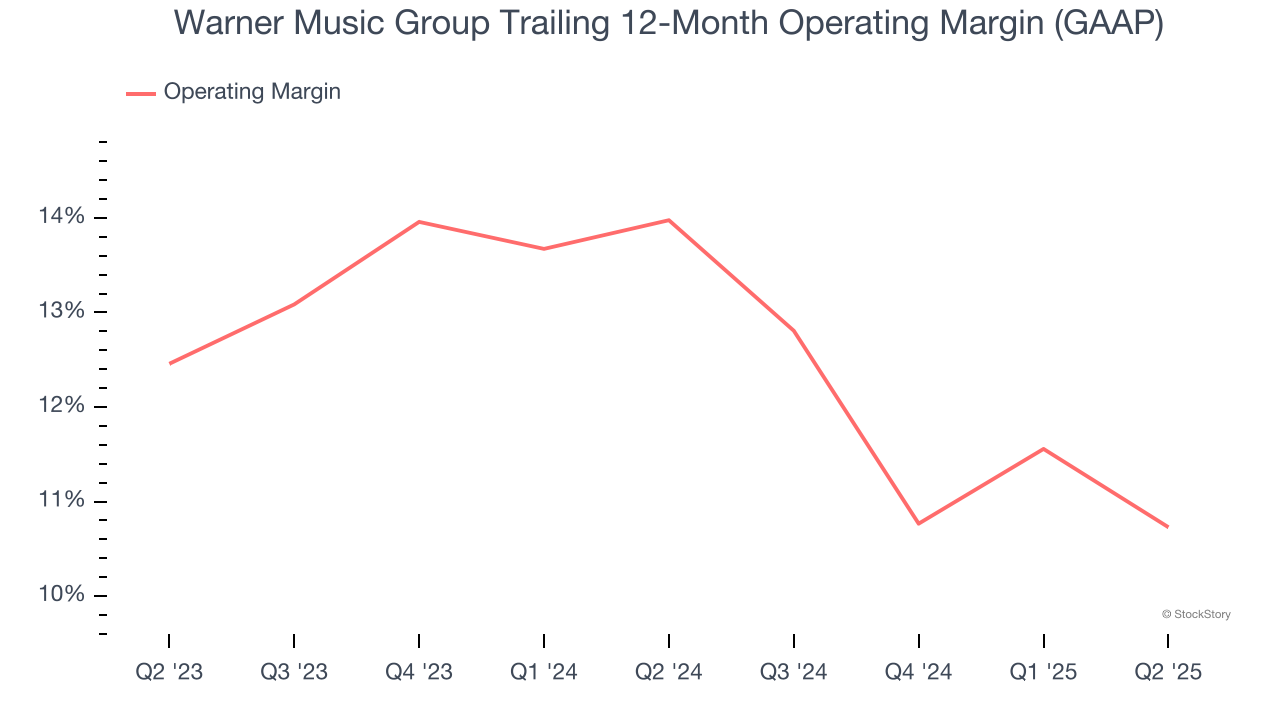

Warner Music Group’s operating margin has been trending down over the last 12 months, but it still averaged 12.3% over the last two years, decent for a consumer discretionary business. This shows it generally does a decent job managing its expenses.

This quarter, Warner Music Group generated an operating margin profit margin of 10%, down 3.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

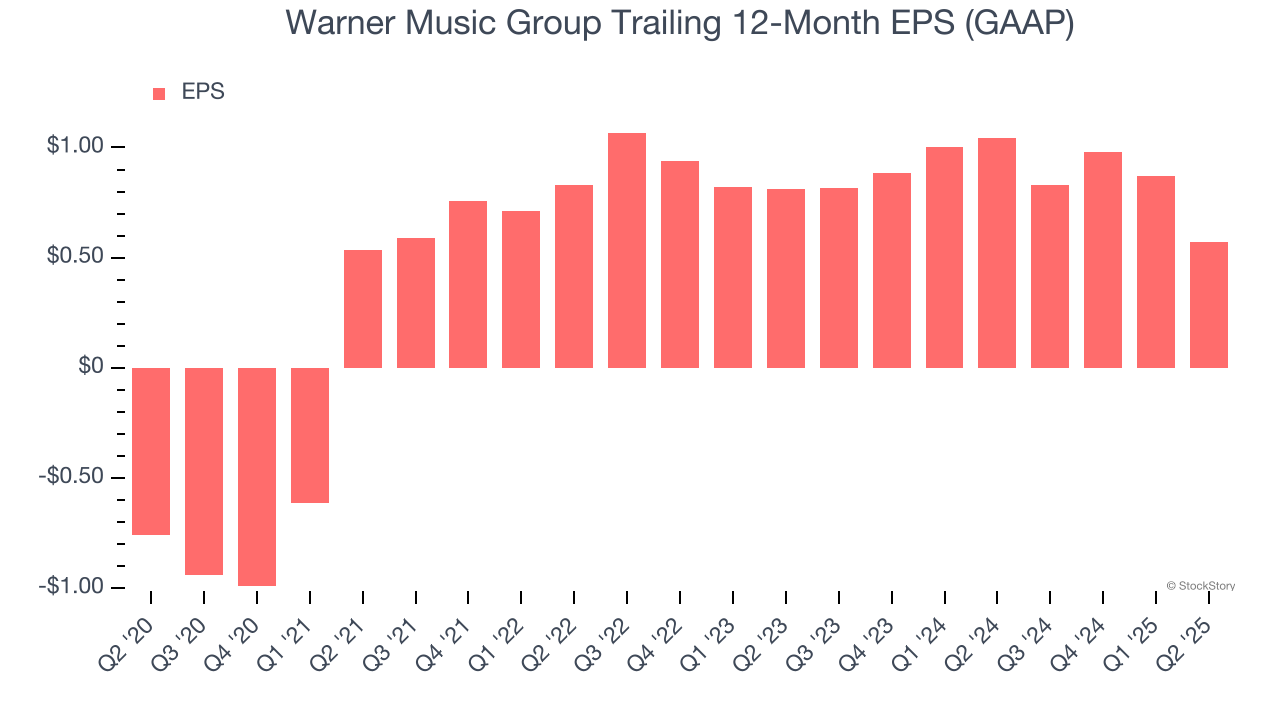

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Warner Music Group’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q2, Warner Music Group reported EPS at negative $0.03, down from $0.27 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Warner Music Group’s full-year EPS of $0.57 to grow 116%.

We enjoyed seeing Warner Music Group beat analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this was a mixed quarter. The stock traded up 3.6% to $31.11 immediately after reporting.

So do we think Warner Music Group is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| Jul-08 | |

| Jul-07 | |

| Jun-10 | |

| May-12 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-07 | |

| Apr-30 | |

| Apr-16 | |

| Apr-14 | |

| Apr-13 | |

| Apr-09 | |

| Apr-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite