|

|

|

|

|||||

|

|

|

Under Armour, Inc. UAA reported first-quarter fiscal 2026 results, wherein the top line exceeded the Zacks Consensus Estimate and the bottom line missed the same. Revenues decreased and earnings increased year over year. Also, e-commerce revenues fell year over year.

However, the company highlighted continued brand momentum despite a challenging environment and reaffirmed its focus on executing the strategic plan with clarity and discipline. Key priorities moving forward include strengthening brand positioning through premium products, increasing average selling prices via innovation, optimizing top-volume programs and delivering a stronger price-to-value proposition to build a more resilient Under Armour.

Under Armour, Inc. price-consensus-eps-surprise-chart | Under Armour, Inc. Quote

The Baltimore, MD-based company reported adjusted earnings of 2 cents per share, which missed the Zacks Consensus Estimate of 3 cents. The reported figure increased from adjusted earnings of 1 cent per share in the year-ago period.

Meanwhile, net revenues of $1,134.1 million beat the Zacks Consensus Estimate of $1,132 million but decreased 4.2% from the prior-year quarter. The metric declined 4% on a currency-neutral basis.

Wholesale revenues fell 4.6% year over year to $649.1 million, while direct-to-consumer revenues declined 3.5% to $463.5 million. Revenues from company-owned and operated stores increased 1%, whereas e-commerce revenues dropped 12% and accounted for 31% of the total direct-to-consumer business for the quarter.

By product category, Apparel revenues declined 1.5% year over year to $746.6 million, beating the Zacks Consensus Estimate of $729.4 million. Footwear revenues decreased 14.3% to $265.9 million, missing the consensus estimate of $286.4 million. Revenues from the Accessories category rose 8.1% to $100.1 million, beating the consensus estimate of $92.4 million. Meanwhile, Licensing revenues improved 12.4% to $24.4 million, marginally missing the consensus estimate of $24.5 million.

Revenues from North America declined 5.5% to $670.3 million, missing the Zacks Consensus Estimate of $675.6 million. Meanwhile, revenues from the international business decreased 1.4% (down 2% on a currency-neutral basis) to $466.6 million.

Within the international segment, revenues from Europe, the Middle East and Africa (“EMEA”) increased 9.6% year over year to $248.6 million, beating the consensus estimate of $244.4 million. Revenues from the Asia-Pacific dropped 10.1% to $163.4 million, surpassing the consensus estimate of $153.6 million. Latin America saw a 15.3% decline to $54.6 million, lagging the consensus estimate of $57.6 million.

Under Armour reported gross profit of $546.5 million, down 2.9% year over year. The company’s gross margin expanded 70 basis points to 48.2% from the prior-year period. This was driven mainly by favorable foreign exchange rates, improved pricing and a stronger product mix. These gains were partially offset by an unfavorable channel mix and increased supply-chain costs compared with the prior year.

Adjusted selling, general and administrative expenses decreased 5.9% year over year to $522.1 million, excluding roughly $8.3 million in transformation costs associated with the fiscal 2025 restructuring plan.

Adjusted operating income was $24.4 million, up from $8 million reported in the year-ago period.

UAA ended the quarter with cash and cash equivalents of $911 million, which includes $400 million in senior notes issued during the quarter. The company plans to use the net proceeds, along with funds from the revolving credit facility and existing cash, to redeem, repurchase, or otherwise retire its $600 million senior notes maturing in June 2026. As of quarter-end, there were no borrowings outstanding under the $1.1 billion revolving credit facility.

The company ended the quarter with long-term debt (net of current maturities) of $389.5 million and total stockholders' equity of $1.87 billion.

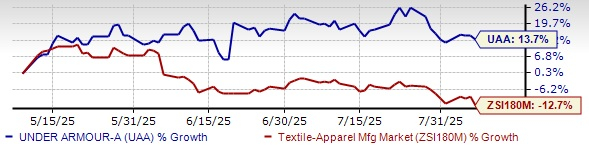

UAA Stock Past 3-Month Performance

Looking ahead to the second quarter of fiscal 2026, this Zacks Rank #4 (Sell) company continues to navigate a challenging macroeconomic and trade environment, including potential demand and cost impacts from tariffs.

Revenues are expected to decline 6-7% compared with the same period in fiscal 2025. This outlook indicates a low-double-digit decrease in North America, high-single-digit growth in EMEA, and a low-teens decline in Asia-Pacific.

The gross margin is predicted to contract 340-360 basis points, primarily due to supply-chain headwinds from anticipated tariff impacts and an unfavorable channel mix. These pressures are expected to be partially offset by favorable foreign exchange and pricing benefits.

Selling, general and administrative expenses are expected to increase at a low-double-digit rate. Excluding transformation costs related to the fiscal 2025 Restructuring Plan, adjusted SG&A is expected to rise at a high-single-digit rate, driven mainly by higher marketing investments as the company laps a timing shift that concentrated most of last year’s spend in the second half.

Operating income is forecasted to range from a $10 million loss to breakeven, with adjusted operating income, excluding restructuring and transformation charges, estimated between $30 million and $40 million. Loss per share is expected to be between 7 cents and 8 cents, while adjusted earnings per share are anticipated to be in the range of 1 cent to 2 cents.

The company has gained 13.7% in the past three months against the industry’s decline of 12.7%.

Some better-ranked stocks are Levi Strauss & Co. LEVI, Wolverine World Wide, Inc. WWW and Stitch Fix SFIX.

Levi designs and markets jeans, casual wear and related accessories for men, women and children. It flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Levi’s current fiscal-year earnings indicates growth of 4% from the year-ago actual. LEVI delivered a trailing four-quarter average earnings surprise of 25.9%.

Wolverine is engaged in the designing, manufacturing and distribution of a wide variety of casual as well as active apparel and footwear. It currently sports a Zacks Rank of 1.

The Zacks Consensus Estimate for Wolverine’s current financial-year earnings and sales indicates growth of 20.9% and 4.6%, respectively, from the year-ago actuals. WWW delivered a trailing four-quarter average earnings surprise of 39.1%.

Stitch Fix delivers customized shipments of apparel, shoes and accessories for women, men and kids. It has a Zacks Rank #2 (Buy) at present.

The Zacks Consensus Estimate for Stitch Fix’s fiscal 2025 earnings indicates an upsurge of 71.7% from the reported level of fiscal 2024. SFIX delivered a trailing four-quarter average earnings surprise of 51.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-07 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite