|

|

|

|

|||||

|

|

|

Getting people to switch banks isn't easy, but SoFi Technologies has been adding millions of new customers annually.

With its own technology platform, SoFi can avoid software vendors that chew up its competitors' profits.

SoFi's lending portfolio has an acceptable level of delinquency now, but we don't know how it will perform in a recession.

Shares of all-digital bank SoFi Technologies (NASDAQ: SOFI) have delivered some big gains lately. From April 4 through the morning of Aug. 11, the stock shot 139% higher.

A rapidly growing user base is the main reason SoFi stock keeps producing big gains, but it isn't the only one. There are several good reasons to be enamored with SoFi stock right now.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Finding excuses to be excited about SoFi's future is easy, but there are also a couple of good reasons to be cautious about buying the stock. Let's look at three reasons to be enthusiastic about the up-and-coming bank before looking at a couple of reasons to remain cautious.

Image source: Getty Images.

SoFi's bears like to remind investors that consumer banking changes very little over time. While the same basic banking principles apply regardless of the underlying technology, SoFi is attracting new customers at a pace that suggests it has built a unique experience that resonates with American consumers.

SoFi began refinancing student loans in 2012, and didn't launch SoFi Money, the operation that includes basic checking and savings accounts, until 2019. SoFi Technologies acquired a banking license in 2022 and ended that year with 5.3 million members using 7.9 million products. By the end of this June, its business grew to 11.7 million members using 17.1 million products.

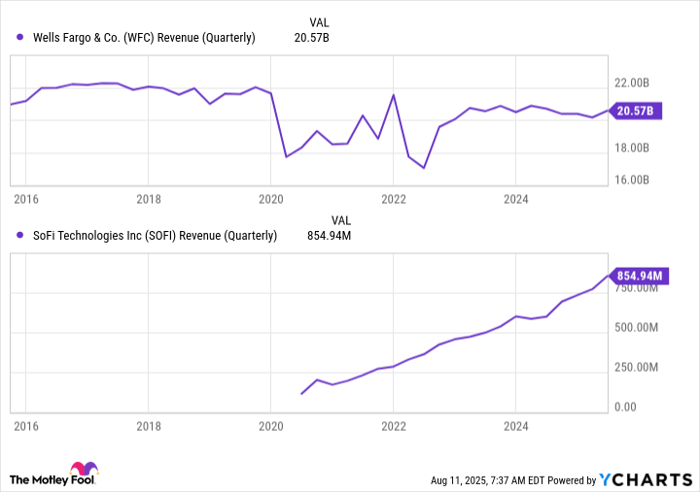

To put a little perspective on how difficult it is to get people to switch banks, consider Wells Fargo. In 2017, it admitted to creating millions of bogus credit card, checking, and other types of accounts for customers without their consent.

In the years since, Wells Fargo hasn't been as transparent about customer account numbers as SoFi Technologies is now. The publicly traded bank still has to report top-line revenue figures, though. Looking at this metric, the fake account scandal didn't even register.

WFC Revenue (Quarterly) data by YCharts

Many SoFi customers will start with one product, such as a personal loan or checking account. Once they become members, though, getting them to engage with another product like a mortgage, stock brokerage account, or credit card has been relatively easy. In the second quarter alone, SoFi added 1.3 million new products, which worked out to 1.5 products per new customer added during the period.

Investors can likely look forward to more new customers coming on board in the years ahead. Brand awareness recently reached an all-time high, but 91.5% of Americans still haven't heard about SoFi Technologies.

In 2020, SoFi acquired Galileo, the technology platform that provides payment processing and other technology support for SoFi's customer-facing applications.

Now that SoFi has its own banking charter, it probably isn't fair to call it a financial technology stock. That said, it's wholly owned technology platform sports more customers than most businesses in the financial technology space. H&R Block, Toast, Eli Lilly, and more than 100 other partners rely on Galileo to manage 158 million accounts for their customers.

The Galileo business isn't just a way for SoFi to lower its own technology expenses. Second-quarter revenue from the segment rose to $110 million, and plenty of that revenue hits the bottom line. Over the past year, more than 30% of technology segment revenue has been recorded as profit.

The last time I purchased SoFi Technologies shares, they were trading at around 2 times the bank's tangible book value. I'd gladly buy more at this valuation, but it's not an option. The stock has been trading at an extremely high 5.5 times its tangible book value.

Well-established consumer banks rarely trade above 2 times their tangible book value. If SoFi's rapid expansion loses steam over the next few years, its valuation could quickly resemble its more-established peers. Although it looks like rapid growth can continue for several more years, this isn't a risk I'm willing to take.

SoFi is building up its mortgage business, but it mostly relies on unsecured personal loans and student loans for revenue. Credit performance has been pretty good so far. The bank's net charge-off percentage on personal loans fell to 4.5% in the second quarter, or just 2.8% if you account for the delinquent loans it's been able to sell.

Like Upstart, SoFi Technologies uses its own system to evaluate individual credit risk. Less reliance on third parties like Fair Isaac, the company that sells access to FICO scores, is great for profitability, but this bank hasn't had a real chance to prove itself yet. Americans haven't experienced a long recession in over a decade.

It isn't SoFi's fault that the U.S. economy has been generally strong for an unusually long time. That said, you probably shouldn't buy any up-and-coming lender at a valuation that is more than double that of its established peers unless you're twice as confident about its future credit performance. Over time, I think SoFi can prove itself. For now, it presents more risk than most investors should feel comfortable accepting.

Before you buy stock in SoFi Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SoFi Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $653,427!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,119,863!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 11, 2025

Wells Fargo is an advertising partner of Motley Fool Money. Cory Renauer has positions in SoFi Technologies. The Motley Fool has positions in and recommends Toast and Upstart. The Motley Fool recommends Fair Isaac. The Motley Fool has a disclosure policy.

| 6 hours | |

| Jul-17 | |

| Jul-14 | |

| Jul-08 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jul-06 | |

| Jul-01 | |

| Jul-01 | |

| Jul-01 | |

| Jun-30 | |

| Jun-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite