|

|

|

|

|||||

|

|

|

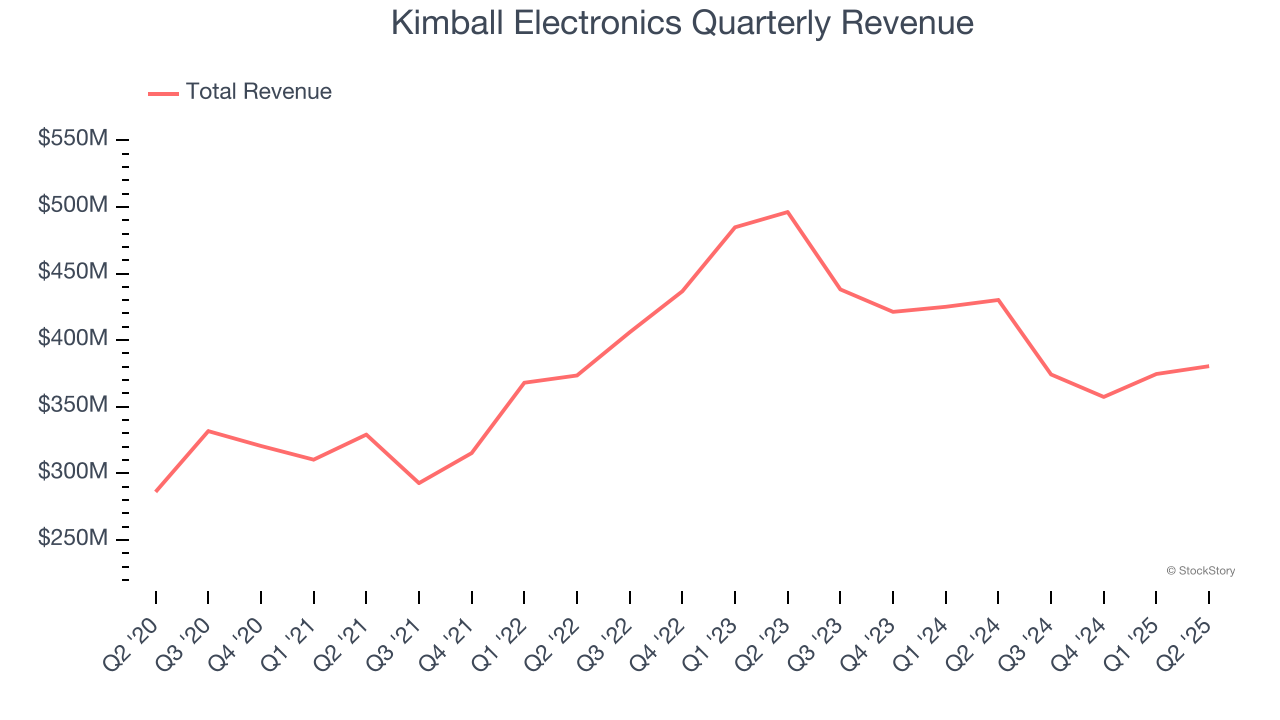

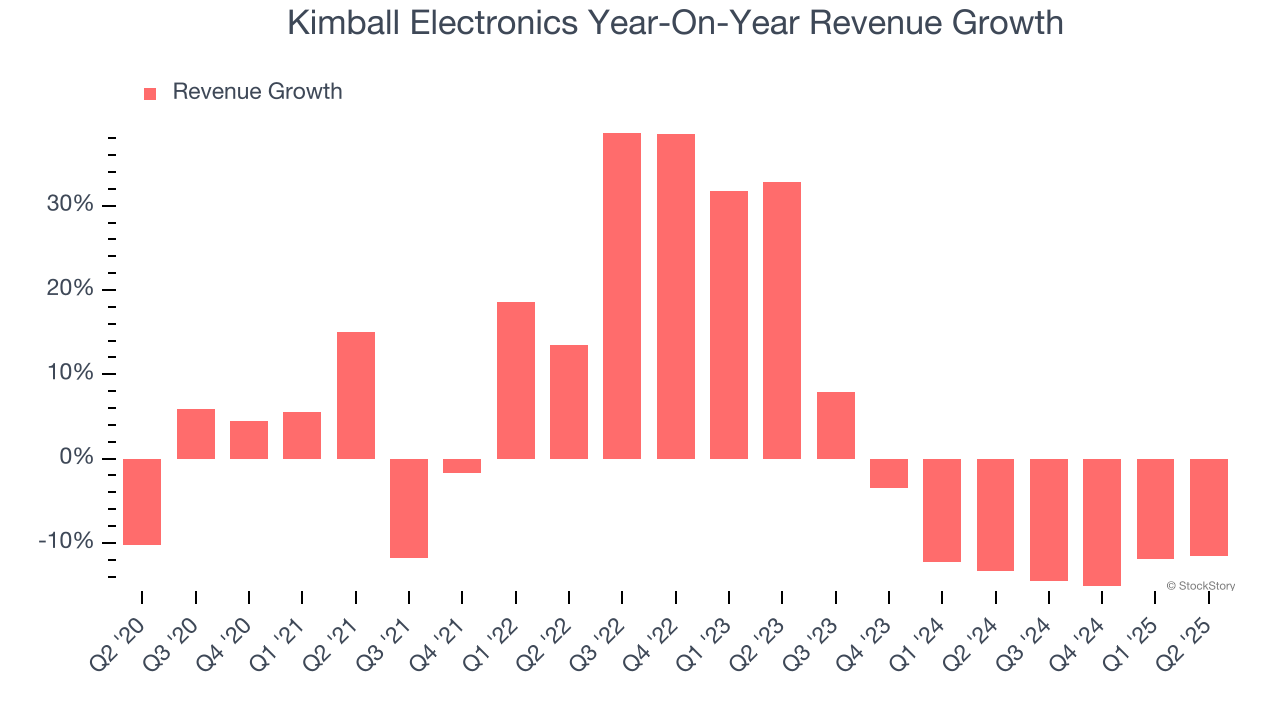

Global electronics contract manufacturer Kimball Electronics (NYSE:KE) beat Wall Street’s revenue expectations in Q2 CY2025, but sales fell by 11.6% year on year to $380.5 million. The company expects the full year’s revenue to be around $1.4 billion, close to analysts’ estimates. Its non-GAAP profit of $0.34 per share was 83.8% above analysts’ consensus estimates.

Is now the time to buy Kimball Electronics? Find out by accessing our full research report, it’s free.

Commenting on today’s announcement, Richard D. Phillips, Chief Executive Officer, stated, “I’m encouraged by the results for the fourth quarter and solid finish to the fiscal year. Q4 came in better than expected, as sales increased sequentially, margins improved, and working capital management drove our sixth consecutive quarter of positive cash flow which was used to pay down debt. Our balance sheet is now in a position of competitive strength with ample liquidity to weather an unpredictable environment, while providing dry powder for opportunistic investments.”

Founded in 1961, Kimball Electronics (NYSE:KE) is a global contract manufacturer specializing in electronics and manufacturing solutions for automotive, medical, and industrial markets.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Kimball Electronics grew its sales at a sluggish 4.4% compounded annual growth rate. This was below our standard for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Kimball Electronics’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 9.7% annually. Kimball Electronics isn’t alone in its struggles as the Electrical Systems industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, Kimball Electronics’s revenue fell by 11.6% year on year to $380.5 million but beat Wall Street’s estimates by 14.2%.

Looking ahead, sell-side analysts expect revenue to decline by 6.3% over the next 12 months. Although this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

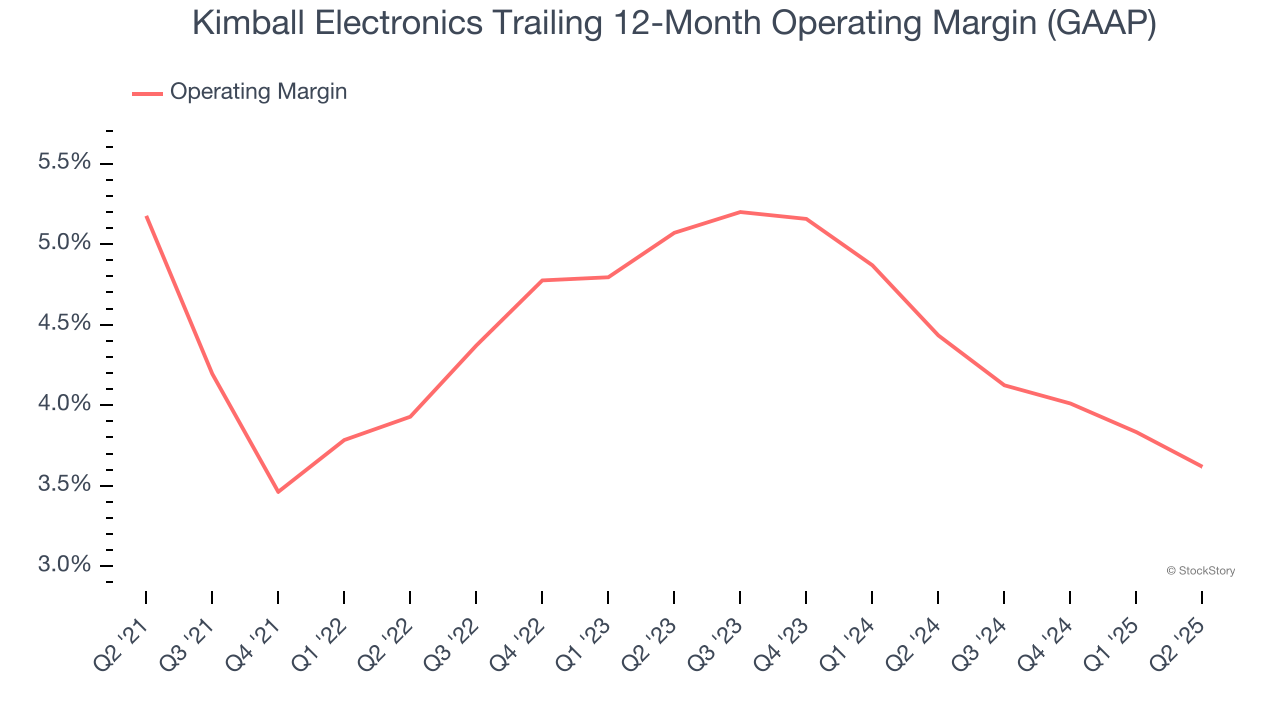

Kimball Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.5% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Kimball Electronics’s operating margin decreased by 1.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Kimball Electronics’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q2, Kimball Electronics generated an operating margin profit margin of 4.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

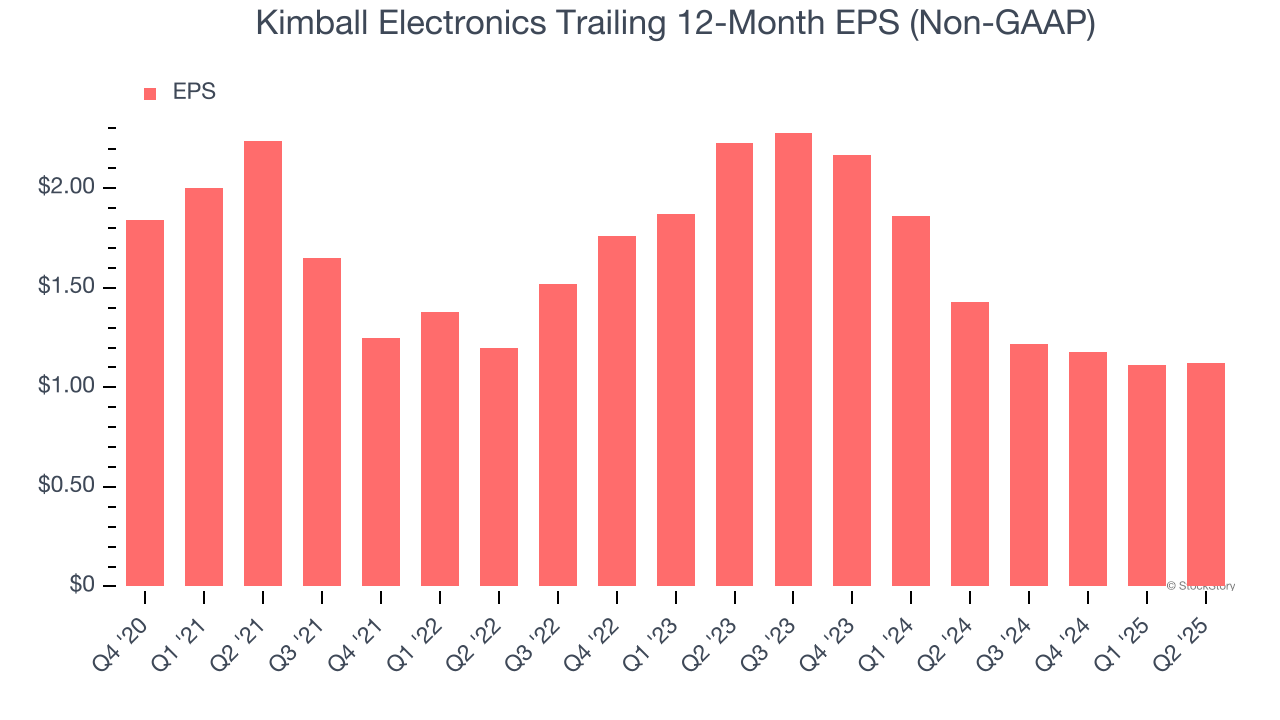

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Kimball Electronics’s flat EPS over the last five years was below its 4.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Kimball Electronics’s earnings to better understand the drivers of its performance. As we mentioned earlier, Kimball Electronics’s operating margin was flat this quarter but declined by 1.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Kimball Electronics’s two-year annual EPS declines of 29.1% were bad and lower than its two-year revenue losses.

In Q2, Kimball Electronics reported adjusted EPS of $0.34, up from $0.33 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Kimball Electronics’s full-year EPS of $1.12 to shrink by 10.3%.

It was good to see Kimball Electronics beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 13.3% to $23.80 immediately after reporting.

Kimball Electronics put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Jul-29 | |

| Jul-15 | |

| Jul-01 | |

| May-19 | |

| May-06 | |

| May-05 | |

| May-05 | |

| Apr-22 | |

| Mar-19 | |

| Mar-10 | |

| Mar-05 | |

| Feb-11 | |

| Feb-05 | |

| Feb-05 | |

| Feb-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite