|

|

|

|

|||||

|

|

|

Comerica has been treading water for the past six months, recording a small return of 2.7% while holding steady at $68.89.

Is now the time to buy Comerica, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We're cautious about Comerica. Here are three reasons why there are better opportunities than CMA and a stock we'd rather own.

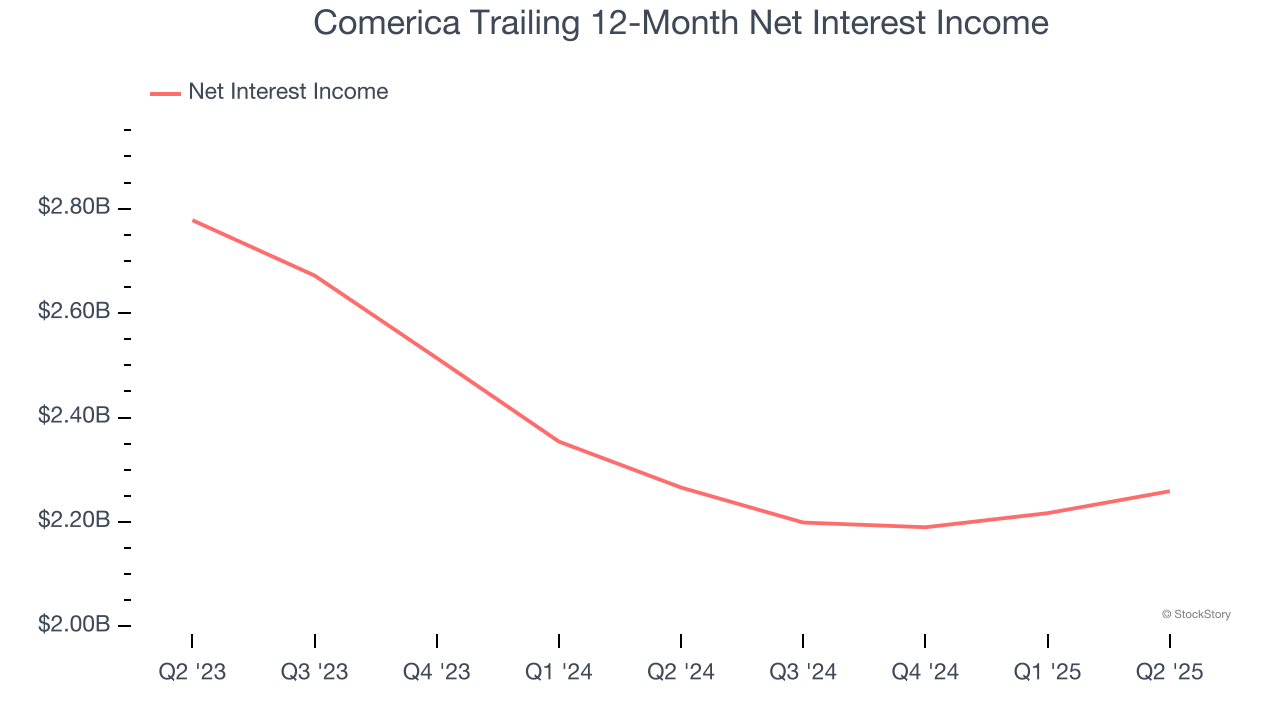

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

Comerica’s net interest income has grown at a 3.2% annualized rate over the last five years, worse than the broader banking industry.

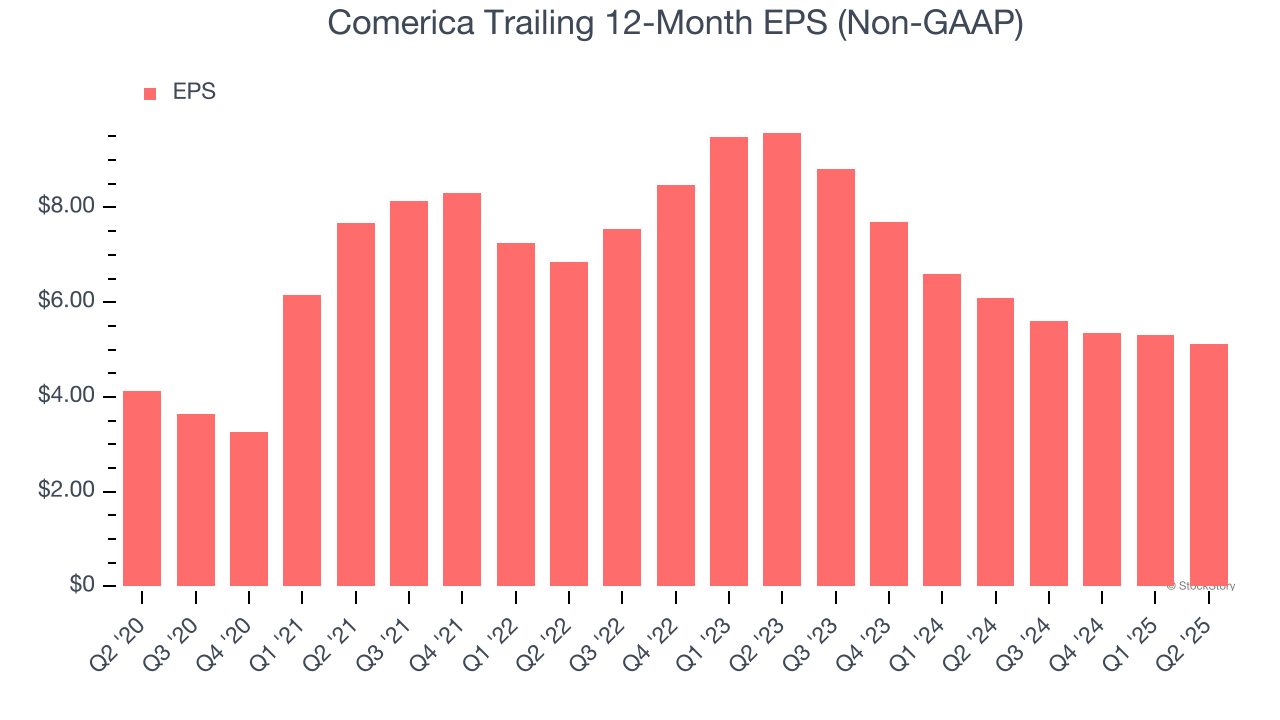

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Comerica’s EPS grew at an unimpressive 4.4% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.2% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

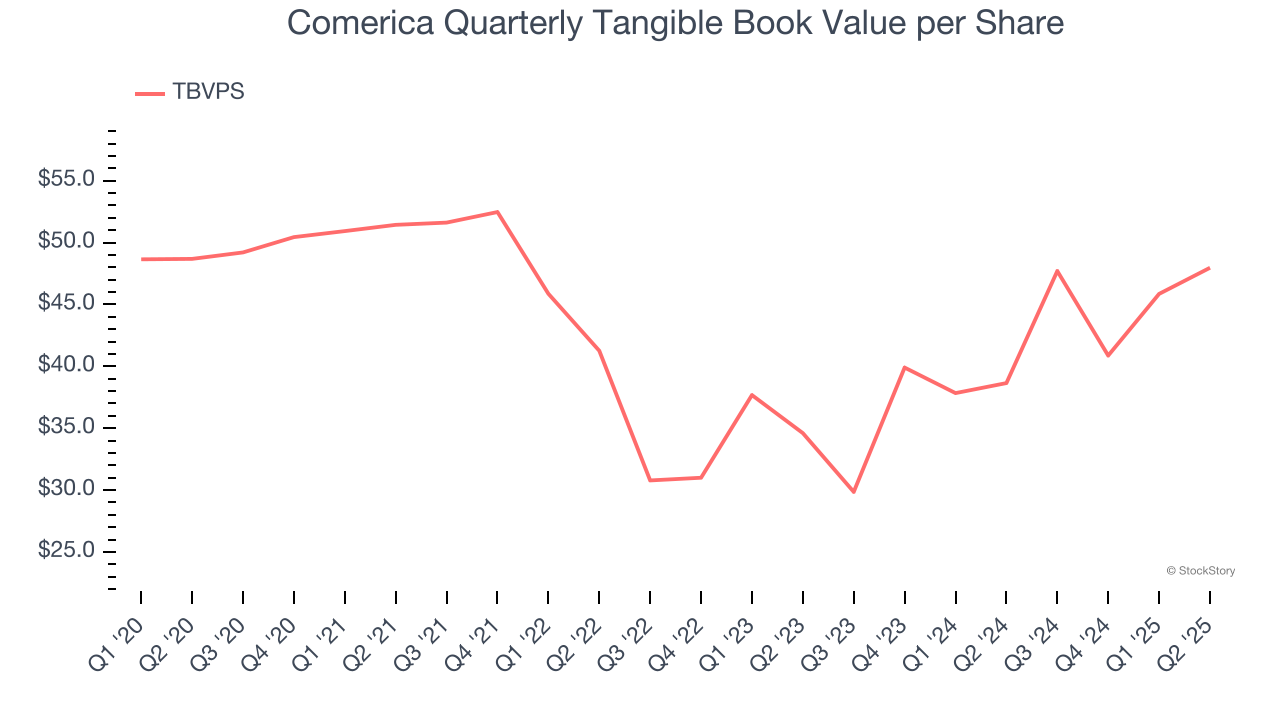

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Although Comerica’s TBVPS was flat over the last five years. the good news is that its growth has recently accelerated as TBVPS grew at an excellent 17.7% annual clip over the past two years (from $34.61 to $47.97 per share).

Comerica isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 1.3× forward P/B (or $68.89 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d recommend looking at one of our top digital advertising picks.

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Feb-09 | |

| Feb-02 |

Fifth Third finalizes purchase of Comerica: What it means for customers

Detroit Free Press

|

| Feb-02 |

Fifth Third Bank acquires Comerica. CEO talks bank consolidations

Yahoo Finance Video

|

| Feb-02 | |

| Feb-02 |

Fifth Third deal finalized, makes it nation's 9th largest

Cincinnati.com | The Enquirer

|

| Feb-02 | |

| Feb-02 |

Fifth Third closes Comerica acquisition in under four months

American Banker

|

| Jan-28 | |

| Jan-28 | |

| Jan-27 | |

| Jan-27 | |

| Jan-23 | |

| Jan-22 |

Davos, Intel Earnings, Inflation Data: Still to Come This Week

The Wall Street Journal

|

| Jan-22 |

Musk at Davos, Intel Earnings, Inflation Gauge: Still to Come This Week

The Wall Street Journal

|

| Jan-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite