|

|

|

|

|||||

|

|

|

DigitalOcean has gotten torched over the last six months - since February 2025, its stock price has dropped 34.1% to $30.76 per share. This may have investors wondering how to approach the situation.

Is now the time to buy DigitalOcean, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we don't have much confidence in DigitalOcean. Here are three reasons why you should be careful with DOCN and a stock we'd rather own.

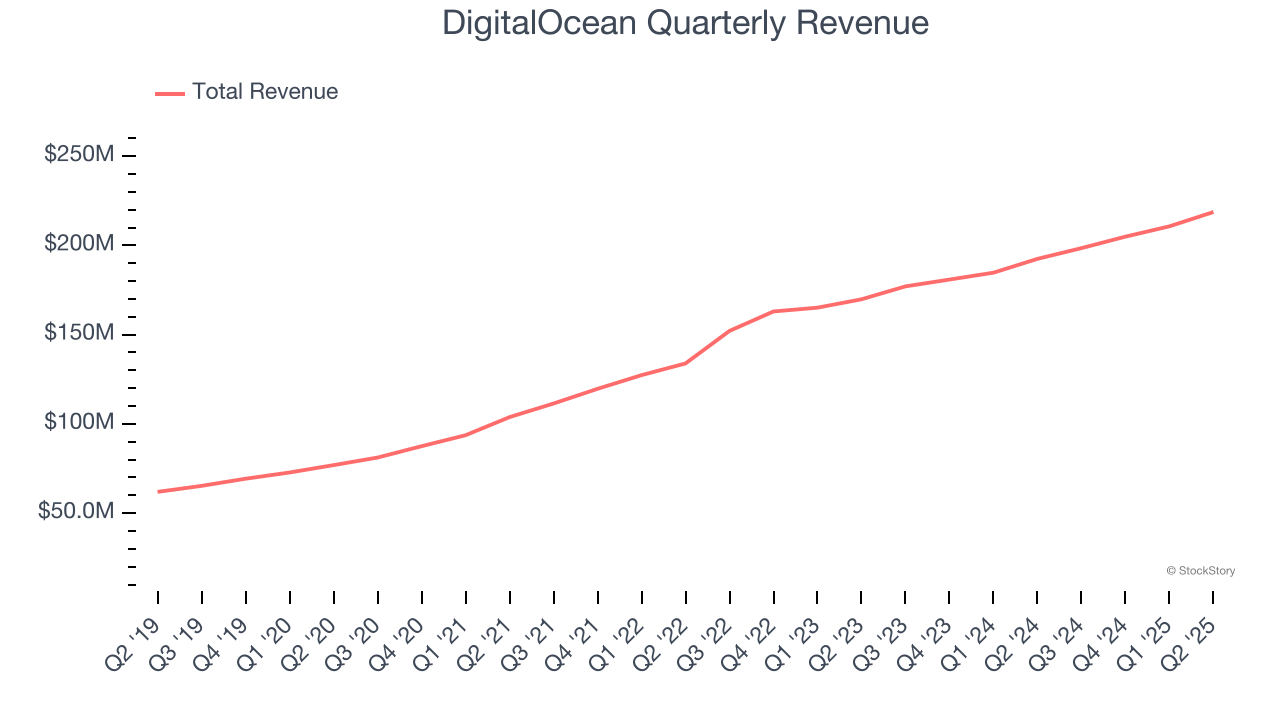

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, DigitalOcean grew its sales at a 19.2% annual rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

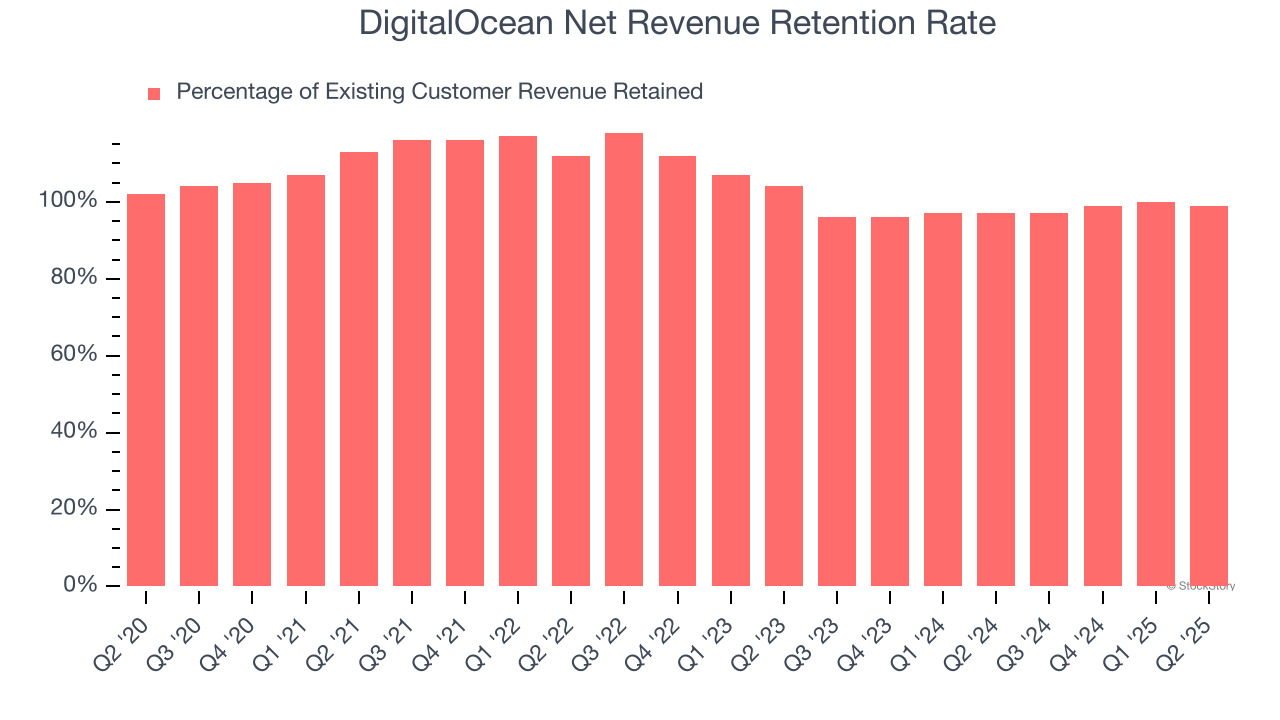

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

DigitalOcean’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 98.8% in Q2. This means DigitalOcean’s revenue would’ve decreased by 1.2% over the last 12 months if it didn’t win any new customers.

DigitalOcean has a weak net retention rate, signaling that some customers aren’t satisfied with its products, leading to lost contracts and revenue streams.

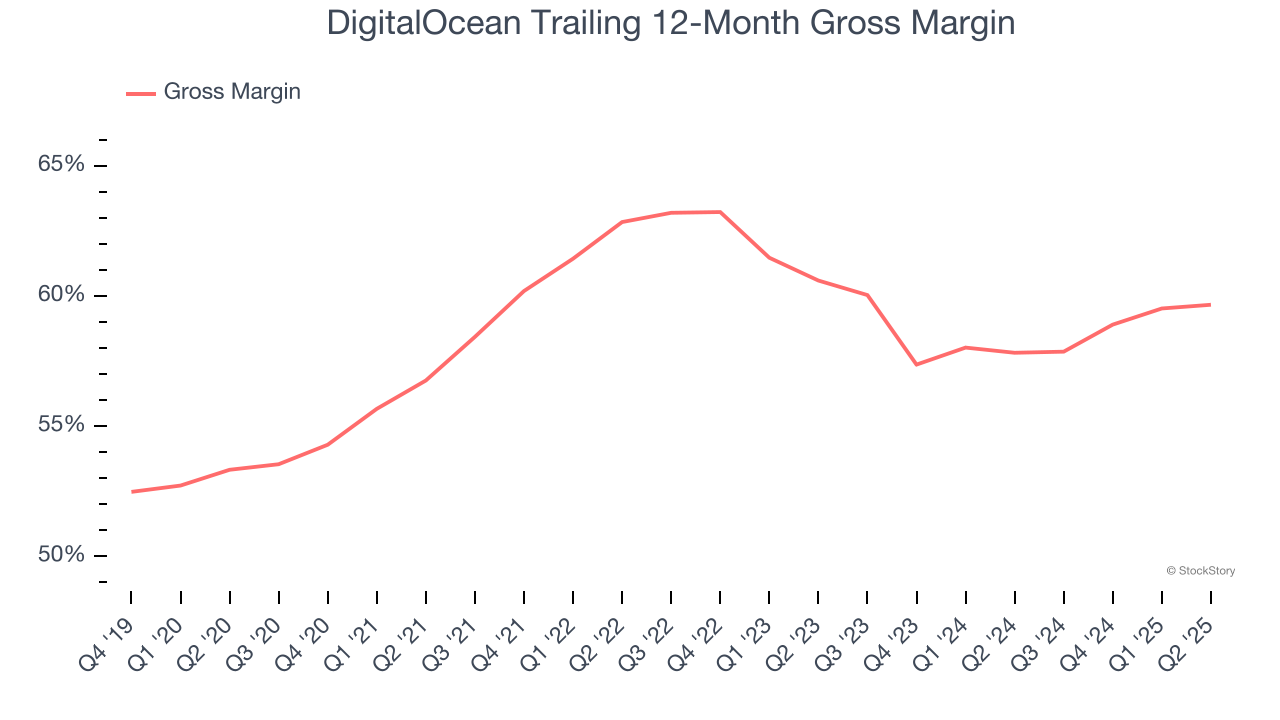

For software companies like DigitalOcean, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

DigitalOcean’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 59.7% gross margin over the last year. Said differently, DigitalOcean had to pay a chunky $40.33 to its service providers for every $100 in revenue.

DigitalOcean isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 3.2× forward price-to-sales (or $30.76 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better stocks to buy right now. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 3 hours | |

| 11 hours | |

| Mar-25 | |

| Mar-24 | |

| Mar-10 | |

| Mar-03 | |

| Mar-02 | |

| Feb-28 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite