|

|

|

|

|||||

|

|

|

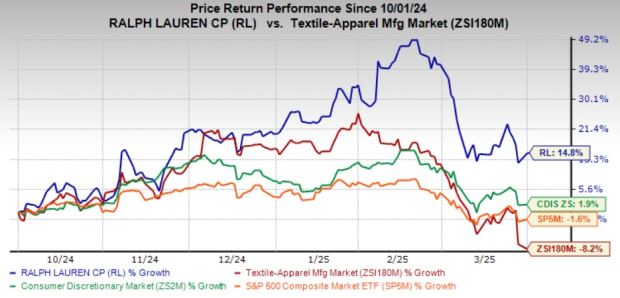

Ralph Lauren Corporation RL has gained 14.8% in the past six months against the industry’s 8.2% decline. It has outperformed the broader sector grwoth of 1.9% and the S&P 500 index's decline of 1.6%.

Ralph Lauren is undergoing significant changes that are influencing its stock performance. The company is demonstrating strong brand and product momentum by executing its long-term strategy across geographies, channels and categories. By expanding brand assortments, introducing innovative products and optimizing distribution channels, Ralph Lauren is well-positioned for sustained growth.

The company's focus on premiumization and brand elevation has resonated well with consumers, leading to increased demand for its core and emerging categories. Strategic investments in digital transformation and direct-to-consumer initiatives have further strengthened its market presence, enhancing customer engagement and driving higher-margin sales.

Ralph Lauren continues to make strong progress on its strategic initiatives to enhance business performance. The company is on track to exceed its sales and profit goals under the Next Great Chapter: Accelerate Plan. This plan aims to streamline operations, upgrade technology and enhance the customer experience.

Ralph Lauren is advancing its digital and omnichannel expansion by investing in mobile, online shopping and fulfillment services. The company’s digital business, including its own websites, department store partnerships, online retailers and social commerce, continues to experience strong growth. RL added nearly two million new consumers to its direct-to-consumer (DTC) business in the third quarter of fiscal 2025, marking steady year-over-year growth. This growth was largely driven by younger, high-value customers who are less price-sensitive, reinforcing the brand’s appeal to the next generation.

Social media engagement continues to grow, with an expanding follower base across platforms like TikTok, Threads, Instagram, Line and Douyin. The brand’s strategic focus on digital storytelling and personalized customer experiences has helped drive deeper engagement with global audiences. By leveraging data analytics and AI-driven insights, Ralph Lauren is enhancing its ability to connect with customers, further strengthening brand loyalty and driving conversion rates.

In the fiscal third quarter, Ralph Lauren achieved significant digital sales growth across key regions, with notable increases in Europe and Asia. The company is experiencing strong DTC comparable store sales growth while expanding its connected ecosystems in major markets. Strong brand positioning and sustained demand for core and seasonal products have driven higher full-price sales and increased average unit retail prices, surpassing expectations.

Ralph Lauren delivered a strong performance across the retail and wholesale channels, surpassing expectations. North America saw steady retail growth, supported by brick-and-mortar strength and digital enhancements, while wholesale revenues improved with strong full-price sell-through. Europe experienced even greater momentum, driven by robust consumer demand and brand elevation efforts. In Asia, significant growth was led by strong digital and in-store sales in key markets like China. Across all regions, the company’s focus on brand storytelling, premium assortments, disciplined inventory management and digital investments continues to drive sustained success.

Ralph Lauren’s fiscal third-quarter results highlighted stronger-than-expected holiday sales as a key driver of higher revenue growth, leading to a more optimistic outlook for fiscal 2025. Driven by positive factors such as brand elevation, strong consumer demand and disciplined execution, the company now expects annual revenue growth to exceed initial projections. Operating margins are also set to expand, supported by higher gross margins and improved cost efficiencies.

For fiscal 2025, the company expects revenue growth (at cc) of 6-7% year over year, compared with the prior estimate of 3-4% growth. Operating margin is likely to expand around 120-160 bps in cc on higher gross margins of about 130 to 170 bps.

For the fiscal fourth quarter, management anticipates revenues to grow nearly 6-7% on a cc basis. Operating margin is expected to expand around 120-140 bps in cc, driven by gross margin expansion of 80-120 bps and slight operating expense leverage. Wholesale is projected to continue its positive trajectory, with North America sell-in aligning more closely with sell-out, and Europe wholesale receipts shifting to the second half of fiscal 2025.

Reflecting optimism around Ralph Lauren, analysts have revised their EPS estimates upward. Over the past 60 days, EPS estimates for the current quarter and fiscal year have increased by 2.6% and 4.8% each to $12.01 and $13.62, respectively. These estimates suggest growth rates of 16.5% and 13.5% year over year, respectively.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Investors may find Ralph Lauren stock appealing, backed by its strong momentum and favorable market sentiment. The company’s emphasis on brand elevation and strategic investments has driven increased consumer demand across various channels. With upwardly revised earnings expectations and a positive growth outlook, Ralph Lauren stands out as an attractive option for those seeking long-term returns. The stock currently holds a Zacks Rank #2 (Buy).

We have highlighted three other top-ranked stocks, namely, V.F. Corporation VFC, Gildan Activewear GIL, and G-III Apparel Group, Ltd. GIII.

V.F. Corp engages in the design, procurement, marketing and distribution of branded lifestyle apparel, footwear and accessories for men, women and children in the Americas, Europe and the Asia-Pacific. It carries a Zacks Rank #2 at present. VFC delivered an earnings surprise of 82.4% in the last reported quarter. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The consensus estimate for V.F. Corp’s current-quarter EPS indicates growth of 53.1% from the year-ago levels.

Gildan Activewear, a manufacturer of premium-quality branded basic activewear, carries a Zacks Rank of 2 at present. GIL has a trailing four-quarter earnings surprise of 5.3%, on average.

The consensus estimate for Gildan Activewear’s current financial-year EPS indicates growth of 16% from the year-ago figure.

G-III Apparel is a manufacturer, designer and distributor of apparel and accessories under licensed brands, owned brands and private label brands. It carries a Zacks Rank #2 at present.

The Zacks Consensus Estimate for GIII’s fiscal 2025 earnings and revenues implies declines of 4.5% and 1.2%, respectively, from the year-ago actuals. GIII delivered a trailing four-quarter average earnings surprise of 117.8%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite