|

|

|

|

|||||

|

|

|

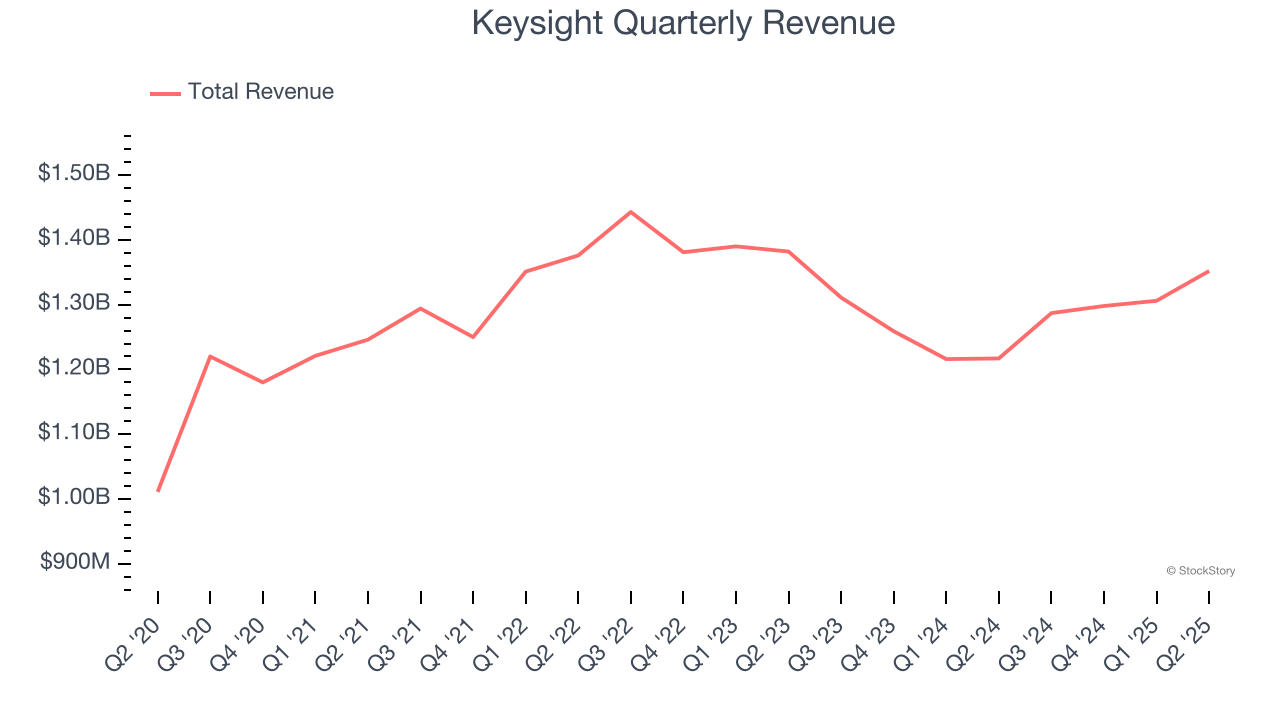

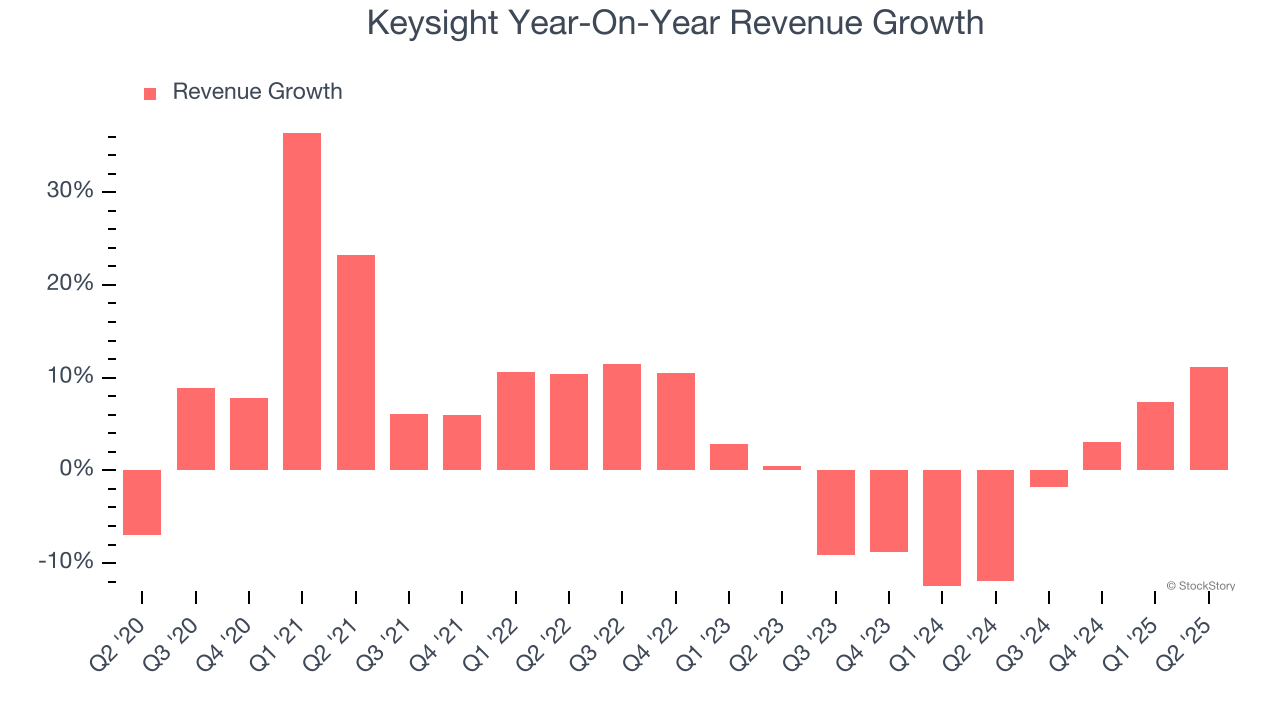

Electronic measurement provider Keysight (NYSE:KEYS) announced better-than-expected revenue in Q2 CY2025, with sales up 11.1% year on year to $1.35 billion. Guidance for next quarter’s revenue was better than expected at $1.38 billion at the midpoint, 0.7% above analysts’ estimates. Its non-GAAP profit of $1.72 per share was 2.9% above analysts’ consensus estimates.

Is now the time to buy Keysight? Find out by accessing our full research report, it’s free.

Spun off from Hewlett-Packard in 2014, Keysight (NYSE:KEYS) offers electronic measurement products for use in various sectors.

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Keysight’s sales grew at a tepid 4.9% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Keysight’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3.2% annually. Keysight isn’t alone in its struggles as the Inspection Instruments industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, Keysight reported year-on-year revenue growth of 11.1%, and its $1.35 billion of revenue exceeded Wall Street’s estimates by 2.7%. Company management is currently guiding for a 7.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.3% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

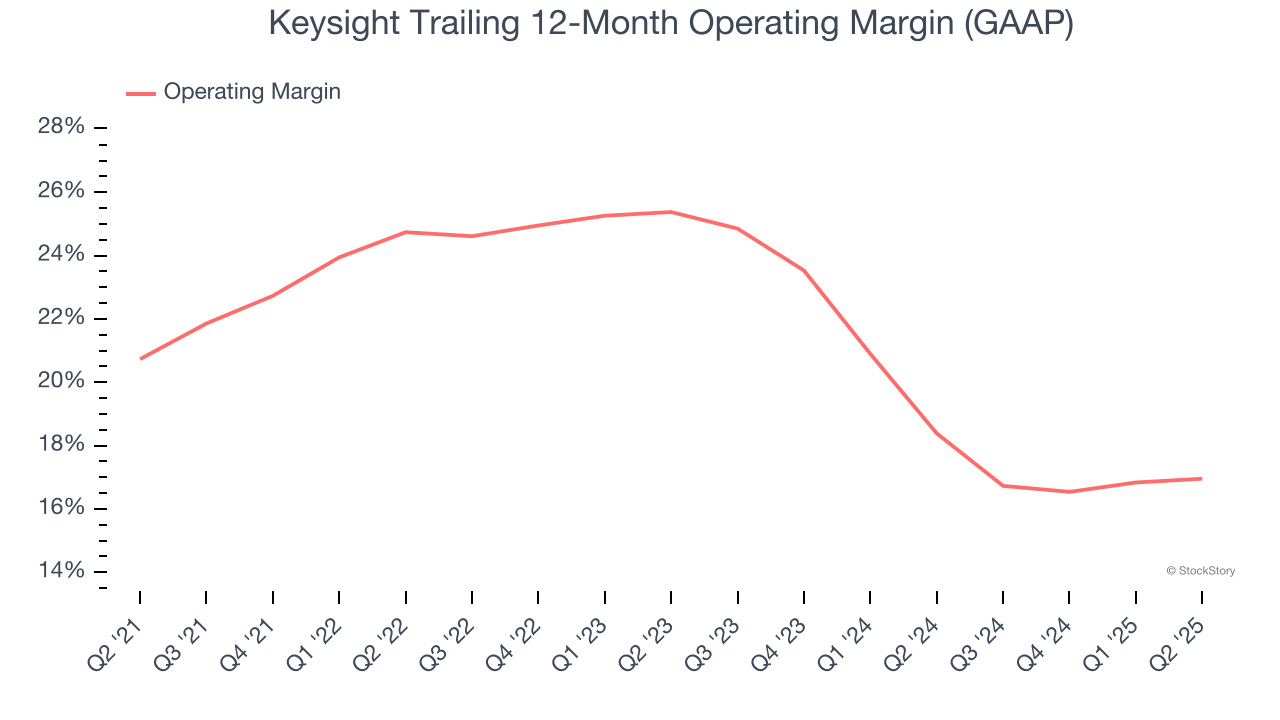

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Keysight has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 21.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Keysight’s operating margin decreased by 3.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Keysight generated an operating margin profit margin of 17.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

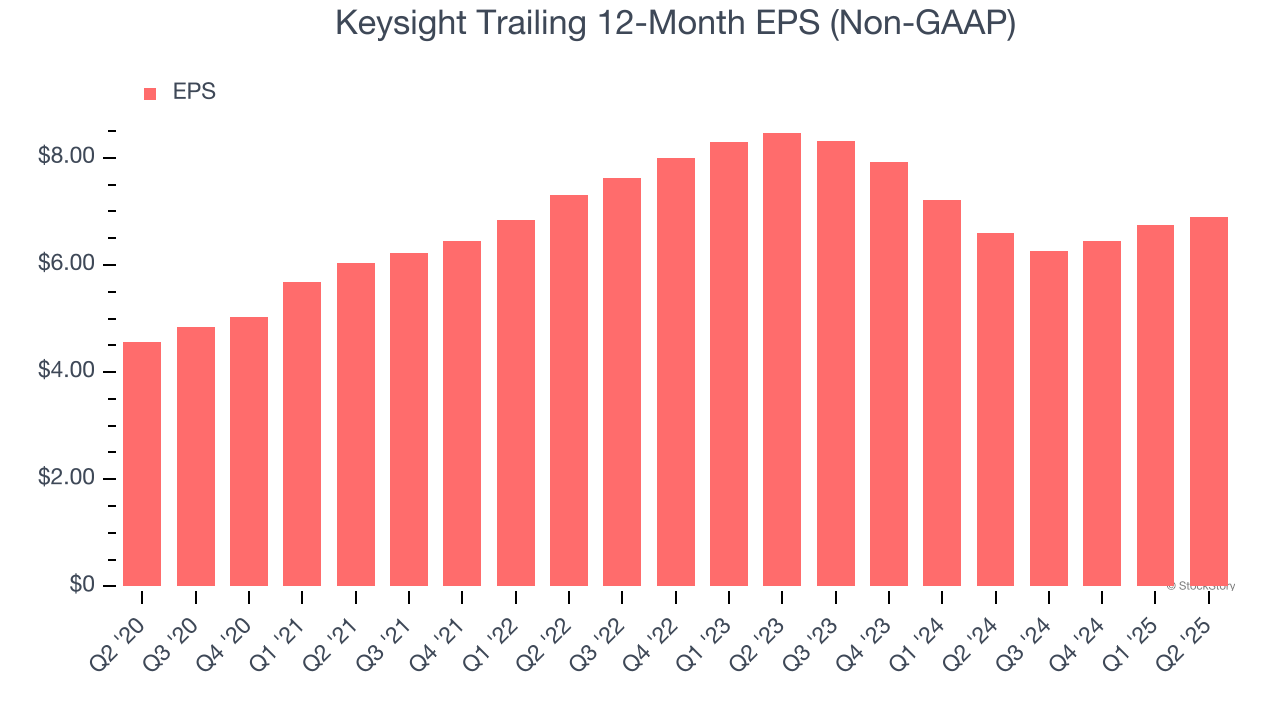

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Keysight’s EPS grew at a decent 8.6% compounded annual growth rate over the last five years, higher than its 4.9% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

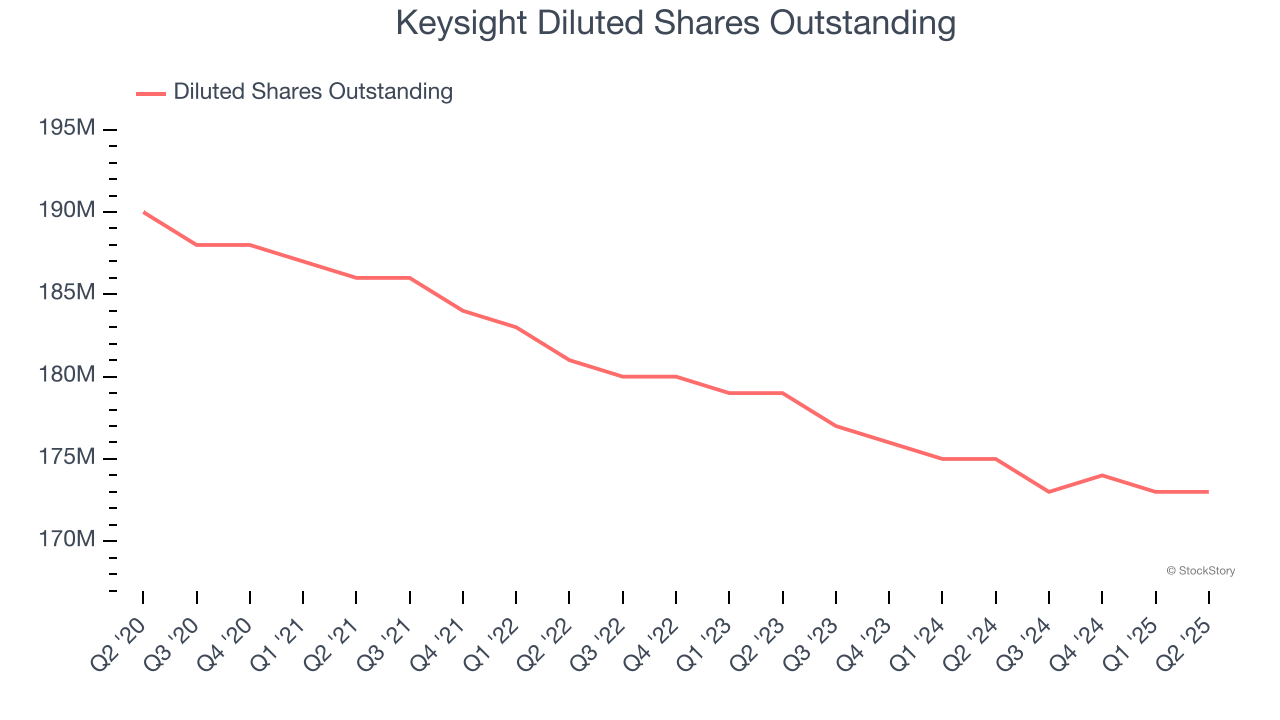

Diving into the nuances of Keysight’s earnings can give us a better understanding of its performance. A five-year view shows that Keysight has repurchased its stock, shrinking its share count by 8.9%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Keysight, its two-year annual EPS declines of 9.8% mark a reversal from its five-year trend. We hope Keysight can return to earnings growth in the future.

In Q2, Keysight reported adjusted EPS of $1.72, up from $1.57 in the same quarter last year. This print beat analysts’ estimates by 2.9%. Over the next 12 months, Wall Street expects Keysight’s full-year EPS of $6.89 to grow 9.1%.

We enjoyed seeing Keysight beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Looking ahead, both revenue and EPS guidance were in line with Wall Street Consensus. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $164 immediately following the results.

Keysight had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| 10 hours | |

| 12 hours | |

| 14 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite