|

|

|

|

|||||

|

|

|

Over the last six months, Paylocity’s shares have sunk to $181.27, producing a disappointing 11.5% loss - a stark contrast to the S&P 500’s 6.4% gain. This might have investors contemplating their next move.

Is now the time to buy Paylocity, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Even though the stock has become cheaper, we're swiping left on Paylocity for now. Here are two reasons why we avoid PCTY and a stock we'd rather own.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Paylocity’s revenue to rise by 7.6%, a deceleration versus This projection doesn't excite us and implies its products and services will face some demand challenges.

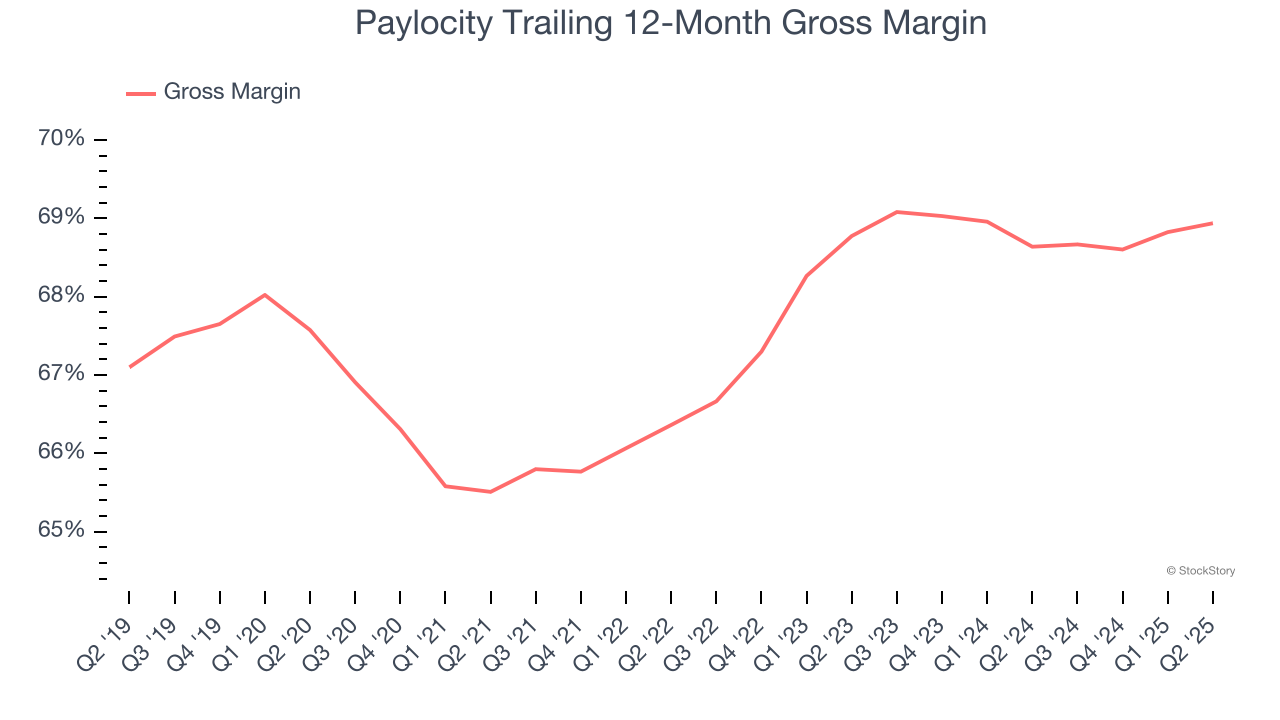

For software companies like Paylocity, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Paylocity’s gross margin is slightly below the average software company, giving it less room than its competitors to invest in areas such as product and sales. As you can see below, it averaged a 68.9% gross margin over the last year. That means Paylocity paid its providers a lot of money ($31.06 for every $100 in revenue) to run its business.

Paylocity isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 5.9× forward price-to-sales (or $181.27 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-21 | |

| Jul-15 | |

| Jul-14 | |

| Jul-09 | |

| Jul-08 | |

| Jul-07 | |

| Jun-10 | |

| May-08 | |

| May-07 | |

| May-07 | |

| Apr-21 | |

| Apr-16 | |

| Apr-07 | |

| Mar-10 | |

| Feb-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite