|

|

|

|

|||||

|

|

|

PubMatic has gotten torched over the last six months - since February 2025, its stock price has dropped 43.6% to $8.19 per share. This may have investors wondering how to approach the situation.

Is there a buying opportunity in PubMatic, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Despite the more favorable entry price, we're swiping left on PubMatic for now. Here are three reasons why you should be careful with PUBM and a stock we'd rather own.

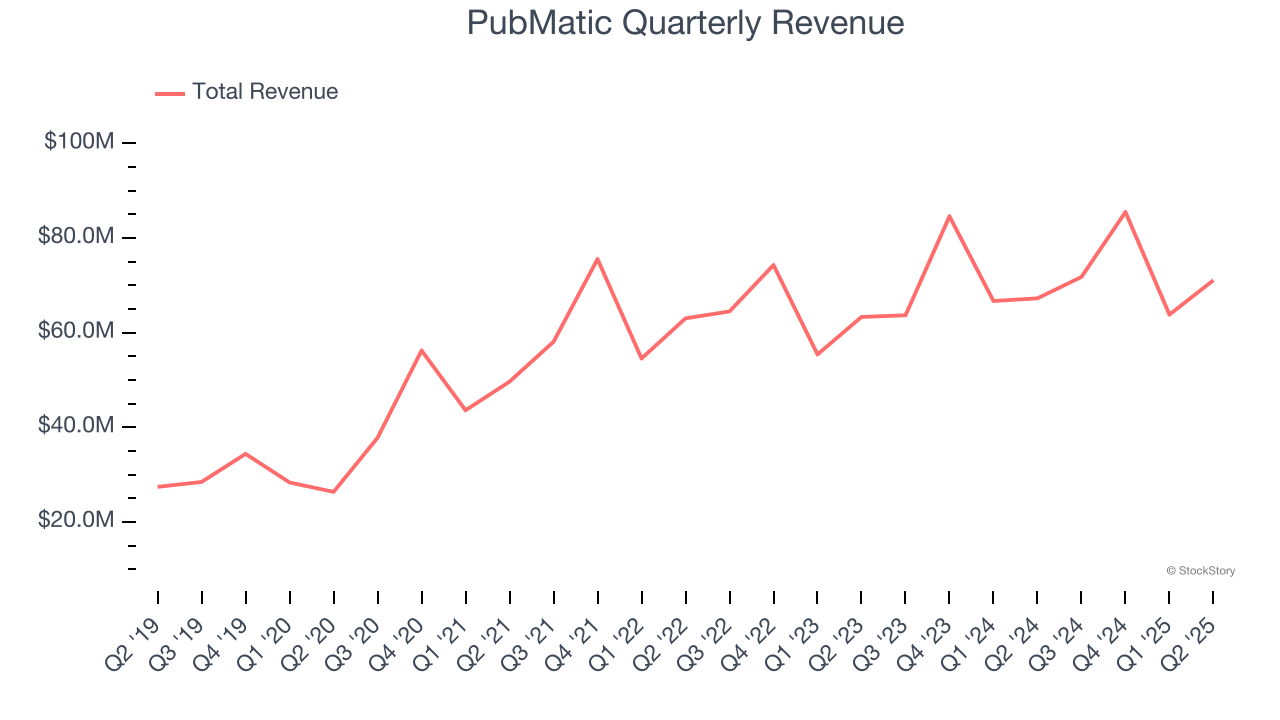

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, PubMatic’s sales grew at a weak 5.2% compounded annual growth rate over the last three years. This fell short of our benchmark for the software sector.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect PubMatic’s revenue to drop by 8%, a decrease from This projection doesn't excite us and suggests its products and services will see some demand headwinds.

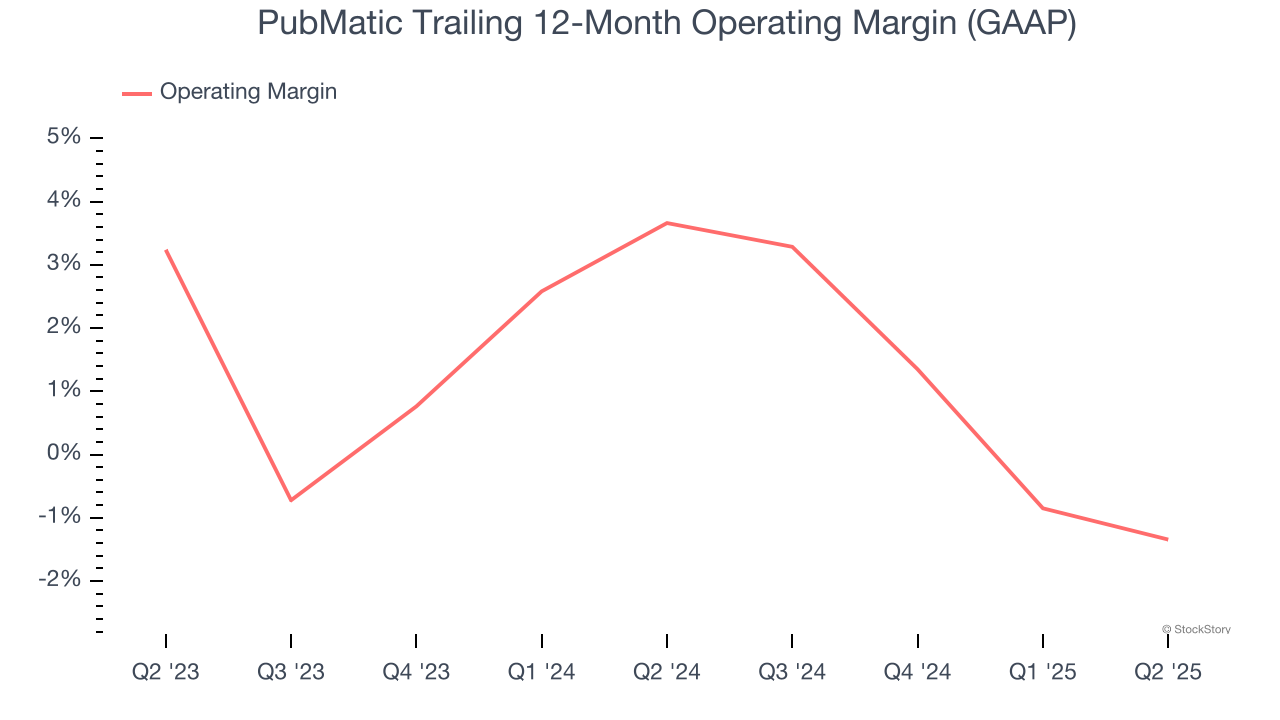

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Analyzing the trend in its profitability, PubMatic’s operating margin decreased by 5 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. PubMatic’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was negative 1.3%.

We cheer for all companies solving complex business issues, but in the case of PubMatic, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 1.4× forward price-to-sales (or $8.19 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are better investments elsewhere. We’d recommend looking at the Amazon and PayPal of Latin America.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Mar-31 | |

| Mar-30 | |

| Mar-25 | |

| Mar-17 | |

| Mar-12 | |

| Mar-09 | |

| Mar-09 | |

| Mar-03 | |

| Feb-28 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite