|

|

|

|

|||||

|

|

|

This month's rebound in Albany International AIN stock could be short-lived, and it may be time to fade the recent rally as the trend of declining earnings estimate revisions suggests that the textiles and materials processing company is not out of the woods yet after facing a number of headwinds in recent years.

Although AIN has spiked +15% in August, Albany International stock is still down 20% year to date and has a grizzly -32% performance in the last three years.

Albany International also appears to be burning through cash at a very fast rate, which is concerning for its operational and financial outlook as well.

Most recently missing its Q2 EPS expectations by 22% in late July, Albany International has raised concerns about its operational efficiency and forecasting accuracy as rising costs and strategic investments have squeezed profit margins, especially in its engineered composites segment. The issue here is that Albany International is also competing in a high-stakes arena of aerospace and advanced materials manufacturing with specialized defense companies such as Ducommun DCO and Hexcel Corporation HXL.

Furthermore, supply chain disruptions have taken a toll on the company’s operations, limiting production as a supplier of fabric for paper and industrial applications and ultimately impacting delivery timelines.

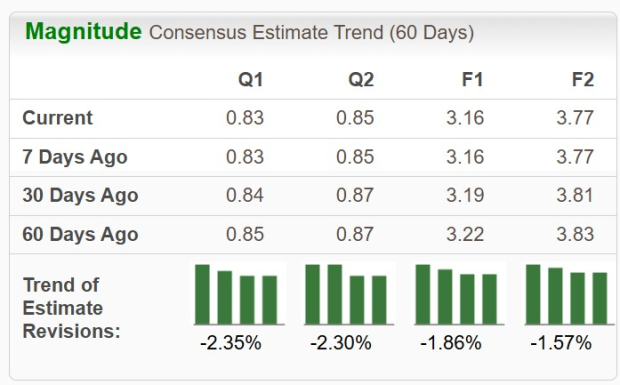

Taking away excitement for a continued rebound in Albany International stock is that fiscal 2025 and FY26 EPS estimates have trended lower in the last 60 days, dipping nearly 2% and 1.6%, respectively.

What may be most concerning to investors is that Albany International has burned through more than half of its liquidity in the last five years, with its cash & equivalents dropping from over $300 million in 2021 to $107 million at the end of Q2 2025.

For now, it may certainly be best to fade the recent rally or avoid Albany International’s stock. Addressing the elephant in the room, Albany International’s growth is respectable, but nothing to necessarily brag about for a company that investors are paying over $60 a share for.

To that point, Albany International has struggled to climb past annual sales of $1 billion or produce full-year EPS of over $4.00, and this is after a drop from a 52-week high of over $90 a share, which may have raised questions about the company’s valuation outside of its operational efficiency.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-23 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite