|

|

|

|

|||||

|

|

|

Philip Morris International Inc.’s PM second-quarter 2025 results spotlight the central question for its long-term transformation: Can smoke-free momentum truly outweigh persistent declines in cigarettes? Smoke-free products, led by IQOS heated tobacco, ZYN nicotine pouches and VEEV e-vapor, surged 11.8% in shipment volumes, lifting net revenues by 15.2% and gross profit by 23.3% year over year. These gains pushed smoke-free to 41% of total revenues and 42% of gross profit.

By contrast, cigarette shipments fell 1.5% to 155.2 billion units, pressured by weakness in Turkey and Indonesia. Still, combustibles contribute $6 billion in quarterly revenues, a 2.1% increase year over year. Management expects full-year smoke-free volumes to grow 12-14%, while cigarette volumes drop about 2%.

Smoke-free growth has become the decisive lever for Philip Morris and the latest results show momentum remains firmly on track. IQOS is winning share in key markets, ZYN accelerated in the United States with 26% growth in the second quarter and VEEV shipments more than doubled. Importantly, smoke-free carries structurally higher margins, cushioning the profit impact of falling cigarettes.

The transition indicates a balance between legacy and emerging categories. Combustibles remain a major revenue and cash contributor, while smoke-free continues to expand its share of growth and profitability. The long-term outcome will depend on the extent to which smoke-free expansion balances declines in combustibles.

Altria Group, Inc. MO is leaning heavily on its on! nicotine pouch brand to fuel smoke-free growth. In the second quarter of 2025, on! shipments climbed 26.5% year over year to 52.1 million cans. The brand now holds an 8.7% retail share of the U.S. oral tobacco category, and Altria continues to expand visibility through targeted retail campaigns and experiential marketing. Altria is investing to solidify on!’s role as its primary reduced-risk growth driver.

Turning Point Brands, Inc. TPB is making an aggressive push into modern oral nicotine with its FRE and ALP pouch brands. In the second quarter of 2025, Modern Oral sales reached $30.1 million, up nearly eightfold year over year. Turning Point Brands raised its 2025 Modern Oral revenue target to $100-$110 million. To capture share in the growing smoke-free category, Turning Point Brands emphasized flavor innovation, brand visibility and expanded retail presence as core strategies.

Shares of Philip Morris have gained 6.1% in the past month compared with the industry’s growth of 11.3%.

From a valuation standpoint, PM trades at a forward price-to-earnings ratio of 20.7X, up from the industry’s average of 15.69X.

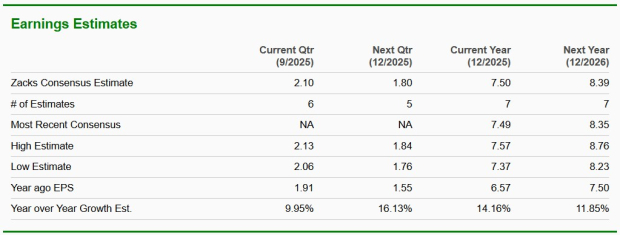

The Zacks Consensus Estimate for PM’s 2025 and 2026 earnings implies year-over-year growth of 14.2% and 11.9%, respectively.

Philip Morris currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-03 | |

| Jul-03 | |

| Jul-02 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite