|

|

|

|

|||||

|

|

|

AIG has been treading water for the past six months, holding steady at $83. The stock also fell short of the S&P 500’s 8.8% gain during that period.

Is now the time to buy AIG, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We don't have much confidence in AIG. Here are three reasons you should be careful with AIG and a stock we'd rather own.

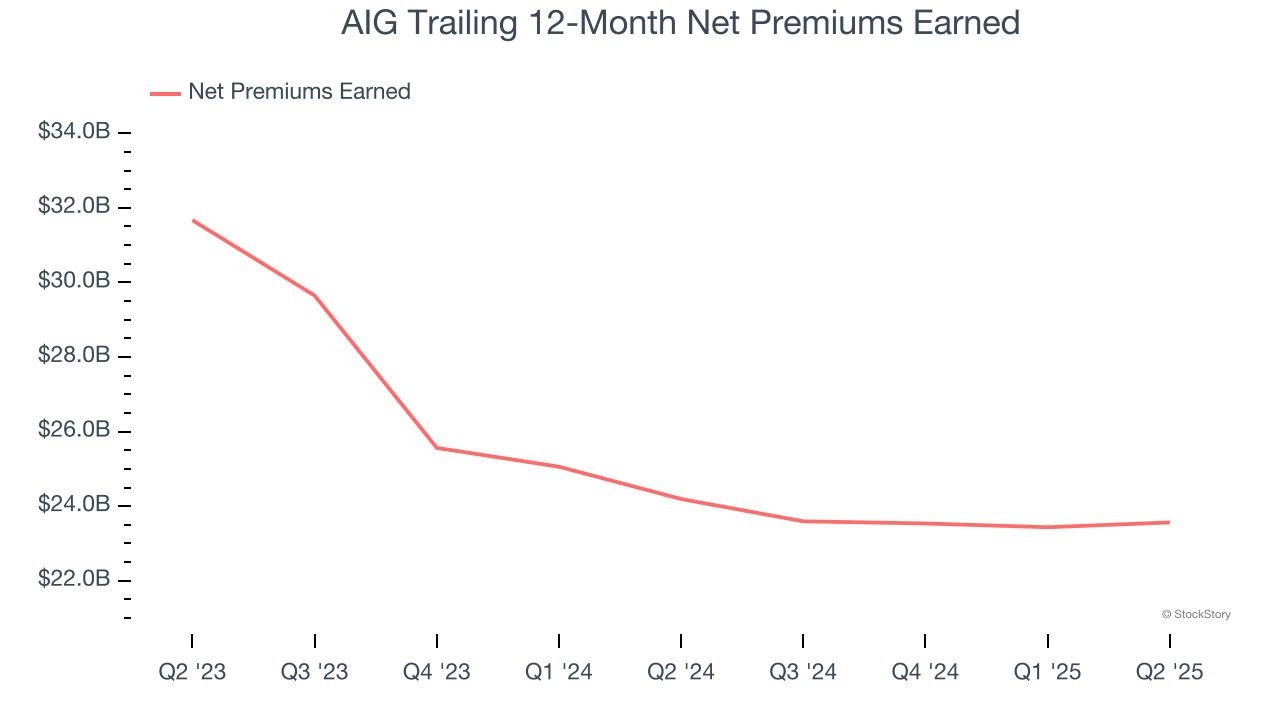

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

AIG’s net premiums earned has declined by 6.6% annually over the last five years, much worse than the broader insurance industry. A silver lining is that policy underwriting outperformed its other business lines.

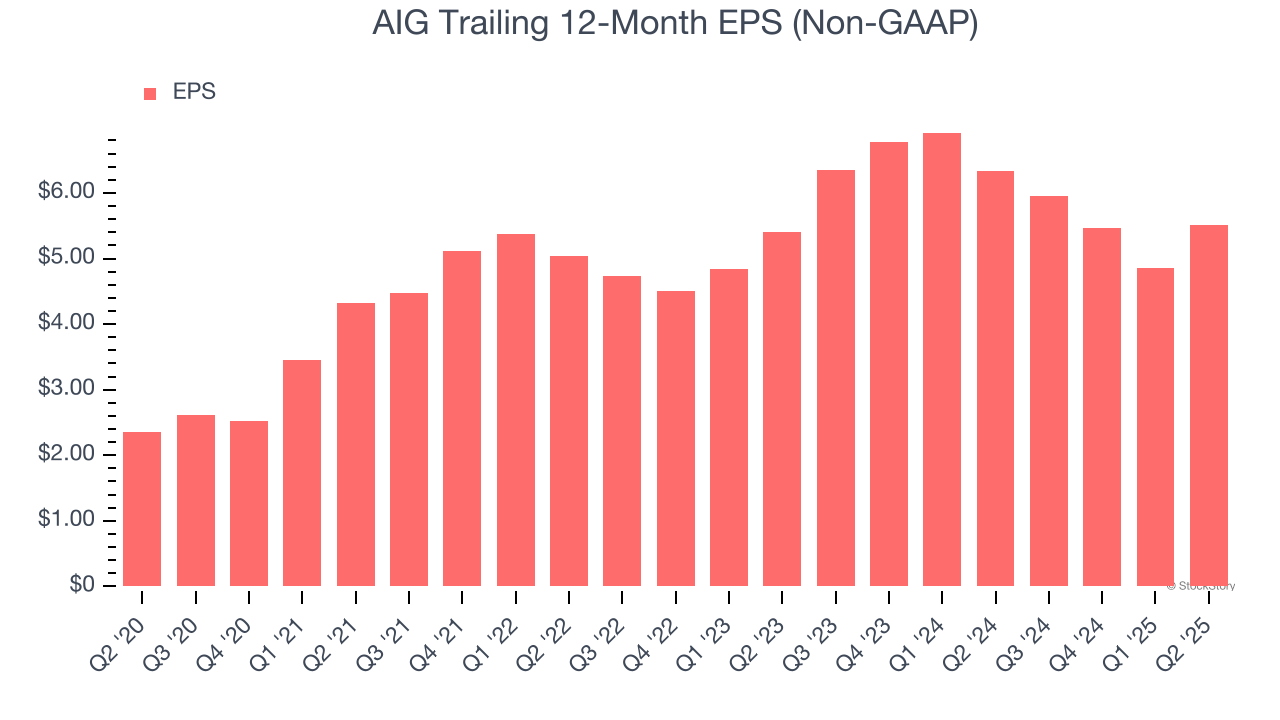

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

AIG’s EPS grew at a weak 1% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 15.2% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

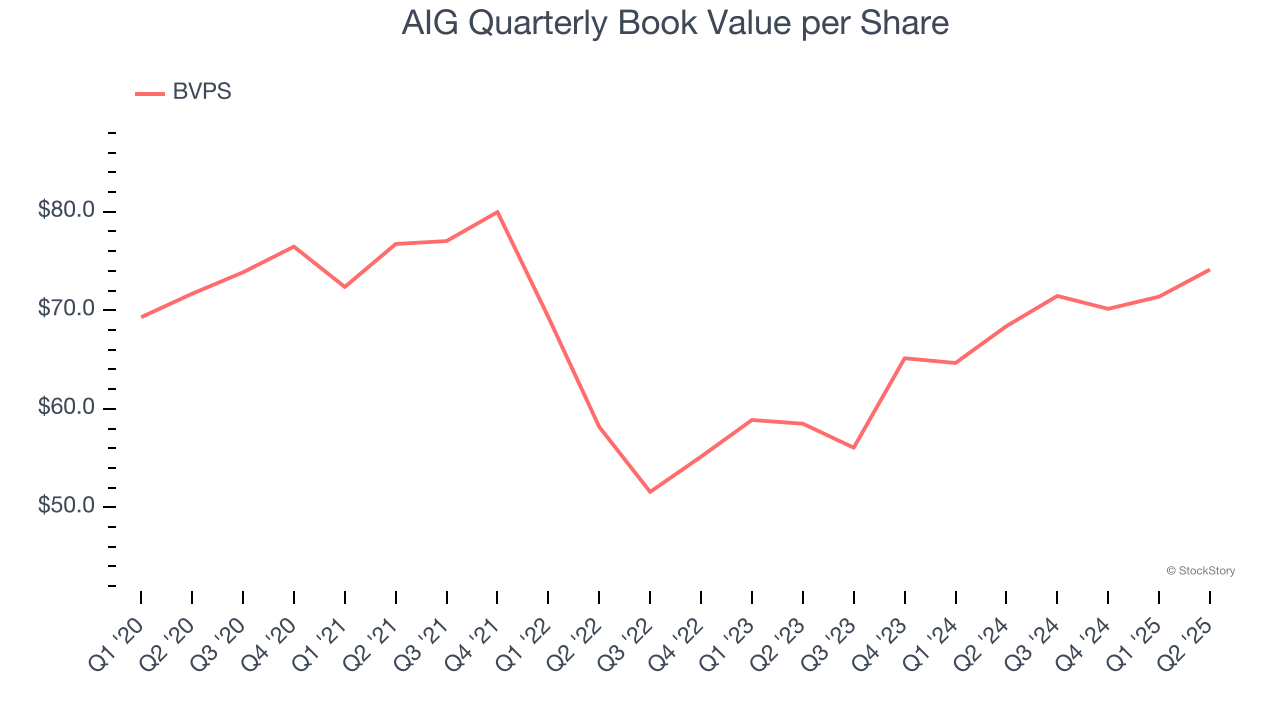

For insurers, book value per share (BVPS) is a vital measure of financial health, representing the total assets available to shareholders after accounting for all liabilities, including policyholder reserves and claims obligations.

Although AIG’s BVPS was flat over the last five years. the good news is that its growth has recently accelerated as BVPS grew at a decent 12.6% annual clip over the past two years (from $58.49 to $74.14 per share).

AIG falls short of our quality standards. With its shares lagging the market recently, the stock trades at 1.1× forward P/B (or $83 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better investments elsewhere. We’d recommend looking at one of our top software and edge computing picks.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Mar-09 |

Nvidia-Tied AI Stocks Vertiv, Lumentum, Coherent To Join S&P 500 Index

AIG

Investor's Business Daily

|

| Mar-07 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-03 | |

| Mar-03 | |

| Feb-27 | |

| Feb-24 | |

| Feb-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite