|

|

|

|

|||||

|

|

|

Zumiez Inc. ZUMZ reported second-quarter fiscal 2025 results, wherein the top line surpassed the Zacks Consensus Estimate and improved year over year. The bottom line beat the estimate and declined year over year. However, comparable sales (comps) improved year over year.

The fiscal second-quarter results reflect continued resilience in its North America business and strong momentum from private label expansion. As a result, shares of this leading global lifestyle retailer increased 14.9% in the after-market trading session yesterday.

Zumiez Inc. price-consensus-eps-surprise-chart | Zumiez Inc. Quote

ZUMZ posted a quarterly loss of 6 cents per share, narrower than the Zacks Consensus Estimate of a loss of 11 cents. However, the bottom line was wider than a loss of 4 cents in the year-earlier quarter.

Total net sales of $214.3 million surpassed the Zacks Consensus Estimate of $211 million and increased 1.9% from $210.2 million in the prior-year quarter. This growth was largely driven by the strong performance in the North America business, which remained robust despite growing macroeconomic uncertainty, influenced by global trade policy developments.

Comps rose 2.5% year over year, marking the fifth consecutive quarter of growth. The Zacks Consensus Estimate for comps growth was pegged at 1% for the quarter under review. The overall increase in comps was primarily driven by higher dollars per transaction, partially offset by a decline in the number of transactions. The rise in dollars per transaction was fueled by an increase in average unit retail, while units per transaction declined slightly.

From a regional perspective, North America’s net sales were $180 million, up 2.1% year over year. Other international sales, comprising Europe and Australia, were $34.2 million, up 1% year over year. Excluding the foreign currency translation impacts, North America’s net sales increased 2.1%, while other international net sales declined 4.2% from the prior-year quarter.

Comps in North America rose 4.2%, marking the sixth consecutive quarter of growth, while international comps declined 5.5% in the quarter under review.

Among product categories, the women’s category saw the highest comps increase, followed by hardgoods and accessories. Conversely, footwear was the largest negative comps category, followed by men’s.

Gross profit jumped 5.9% year over year to $76 million, whereas the gross margin expanded 130 bps to 35.5%. This rise was mainly due to a 60-basis-point improvement in the product margin and another 60-basis-point benefit from leveraging store occupancy costs, supported by higher sales and the closure of underperforming stores.

Selling, general and administrative (SG&A) costs of $75.9 million increased 5.2% from $72.2 million in the prior-year quarter. As a percentage of sales, SG&A was 35.4%, up 100 basis points from the year-ago quarter.

This increase was driven by a 40-basis-point rise in corporate costs, a 30-basis-point increase from an unanticipated legal settlement and a 20-basis-point increase from annual incentive compensation. It also reflected a 20-basis-point increase from higher store wages, a 20-basis-point increase in non-store SG&A wage costs and a 30-basis-point increase from smaller items such as impairment charges, training and other miscellaneous costs. These increases were partially offset by a 60 basis-point benefit from lower non-wage store operating expenses.

Zumiez reported an operating income of $0.1 million versus an operating loss of $0.4 million in the year-ago quarter.

As of Aug. 2, 2025, cash and current marketable securities totaled $106.7 million, down from $127 million as of Aug. 3, 2024. The decrease was primarily due to $38.3 million in share repurchases and $14.1 million in capital expenditure, partially offset by $26.6 million in cash provided by operating activities and the release of $3 million in restricted cash. The company had no debt at the end of the fiscal second quarter.

Total shareholders’ equity was $292.4 million. In the quarter, the company repurchased 0.6 million shares at an average price of $13.10 per share (including commissions) for a total of $7.8 million. As of Aug. 2, 2025, $7.2 million remained under the $15-million repurchase authorization approved by the board on June 4, 2025.

The company ended the fiscal second quarter with $157.7 million in inventory, down 0.6% from the year-ago quarter (or down 1.7% on a constant-currency basis).

As of Aug. 30, 2025, Zumiez operated 730 stores, including 570 in the United States, 46 in Canada, 86 in Europe and 28 in Australia. Management continues to expect six store openings in fiscal 2025, comprising five in North America and one in Australia. They also plan to close 20 stores in fiscal 2025, including up to 17 in the United States, two in Canada, and one in Europe.

Net sales for the 30 days ended Sept. 1, 2025, increased 10.6% from the comparable period ended Sept. 2, 2024. Comps rose 11.2% year over year. From a regional perspective, North America net sales increased 11.7%, whereas the other international business grew 2.3%. Excluding the impacts of foreign currency translation, North America net sales still increased 11.7%, while other international net sales declined 2.1% from the prior-year period.

Comps in North America grew 13% during the period, whereas comps in the other international segment declined 3.2%. By category, women’s was the strongest performing in terms of comps, followed by men’s, accessories, footwear and hardgoods, with all categories delivering positive results overall.

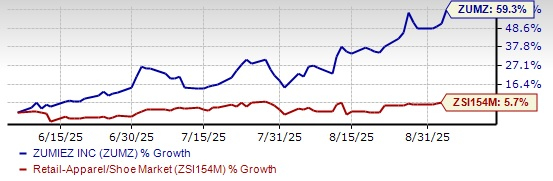

ZUMZ Stock Past 3-Month Performance

For the third quarter of fiscal 2025, the company expects total sales between $232 million and $237 million, indicating year-over-year growth. Comps growth is anticipated to be 5.5-7.5%.

The product margin is projected to increase from that reported in the third quarter of fiscal 2024. Consolidated operating income for the quarter is expected between 2.3% and 3.3% of sales. Earnings per share are expected to be 19 cents to 29 cents, whereas it reported 6 cents in the prior-year period.

For fiscal 2025, Zumiez anticipates 3-4% year-over-year sales growth despite the closure of 33 stores in fiscal 2024 and 20 store closures planned in fiscal 2025, which combined are estimated to have a negative impact on sales of $14 million for fiscal 2025.

The company anticipates modest year-over-year growth in the product margin in fiscal 2025, on top of the 70 bps improvement in fiscal 2024. The additional gross margin leverage is expected to come through other expense categories, such as occupancy, distribution and logistics.

SG&A costs, excluding the one-time legal charges, are expected to remain relatively flat as a percentage of sales compared with fiscal 2024. This outlook reflects continued discipline in expense management, while also supporting investments in key long-term strategic initiatives. Together, these actions are anticipated to drive year-over-year improvement in operating margins and net income, returning the company to profitability in fiscal 2025.

Capital expenditure for fiscal 2025 is expected between $11 million and $13 million, whereas it reported $15 million in fiscal 2024. Shares of this Zacks Rank #1 (Strong Buy) company have soared 59.3% in the past three months against the industry’s growth of 5.7%.

Some other top-ranked stocks are Levi Strauss & Co. LEVI, Genesco Inc. GCO and The TJX Companies, Inc. TJX.

Levi Strauss designs and markets jeans, casual wear and related accessories. It sports a Zacks Rank of 1 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Levi Strauss’ current financial-year earnings indicates growth of 4% from the year-ago actual. LEVI delivered a trailing four-quarter average earnings surprise of 25.9%.

Genesco is a Nashville-based specialty retail and branded company that sells footwear and accessories in retail stores. It currently flaunts a Zacks Rank of 1.

The Zacks Consensus Estimate for GCO’s fiscal 2026 earnings and sales implies growth of 67% and 3%, respectively, from the year-ago actuals. Genesco delivered a trailing four-quarter average earnings surprise of 28.1%.

The TJX Companies is a leading off-price retailer of apparel and home fashions. It carries a Zacks Rank #2 (Buy) at present.

The Zacks Consensus Estimate for The TJX Companies’ current fiscal-year earnings and sales indicates growth of 7% and 5.4%, respectively, from the year-ago actuals. TJX delivered a trailing four-quarter average earnings surprise of 5.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-19 | |

| Jul-16 | |

| Jul-16 | |

| Jul-14 | |

| Jul-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite