|

|

|

|

|||||

|

|

|

As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the electrical systems industry, including Methode Electronics (NYSE:MEI) and its peers.

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

The 13 electrical systems stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 2.9% while next quarter’s revenue guidance was 2.4% below.

In light of this news, share prices of the companies have held steady as they are up 4.6% on average since the latest earnings results.

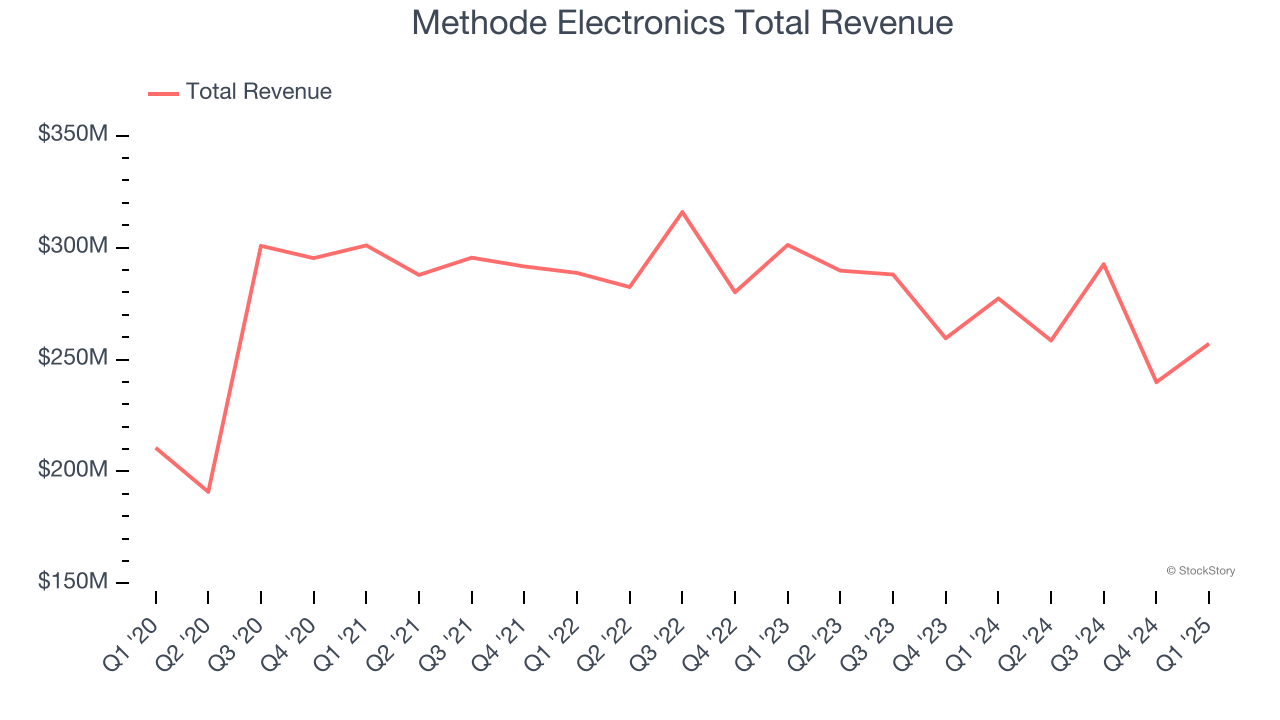

Founded in 1946, Methode Electronics (NYSE:MEI) is a global supplier of custom-engineered solutions for Original Equipment Manufacturers (OEMs).

Methode Electronics reported revenues of $257.1 million, down 7.3% year on year. This print exceeded analysts’ expectations by 12.4%. Despite the top-line beat, it was still a softer quarter for the company with full-year revenue guidance missing analysts’ expectations.

Management CommentsPresident and Chief Executive Officer Jon DeGaynor said, “The Methode transformation journey made further progress in the quarter, as we focused on improving execution to drive long-term value. We have built a new management team and set records for the quarter and the year in data center power product sales, with the year finishing at over $80 million. The year also provided a series of challenges both exogenous and endogenous. We experienced a significant ramp down in expected demand from one of our largest EV customers and delays with other EV customers. In fact, we finished the year with a challenging exercise to write down inventory primarily related to materials for reduced, delayed or canceled programs. While the team made clear strides in improving operational execution, the results were masked by factors that were either outside our immediate control or residual in nature which led to a larger than expected net loss for the quarter.”

Methode Electronics delivered the weakest full-year guidance update of the whole group. Unsurprisingly, the stock is down 27.6% since reporting and currently trades at $7.44.

Read our full report on Methode Electronics here, it’s free.

Enhancing commercial environments, LSI (NASDAQ:LYTS) provides lighting and display solutions for businesses and retailers.

LSI reported revenues of $155.1 million, up 20.2% year on year, outperforming analysts’ expectations by 11.6%. The business had an incredible quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 24.3% since reporting. It currently trades at $23.99.

Is now the time to buy LSI? Access our full analysis of the earnings results here, it’s free.

Credited with introducing the first automatic washing machine, Whirlpool (NYSE:WHR) is a manufacturer of a variety of home appliances.

Whirlpool reported revenues of $3.77 billion, down 5.4% year on year, falling short of analysts’ expectations by 3%. It was a softer quarter as it posted full-year EPS guidance missing analysts’ expectations significantly and a significant miss of analysts’ adjusted operating income estimates.

As expected, the stock is down 2.5% since the results and currently trades at $95.40.

Read our full analysis of Whirlpool’s results here.

One of the pioneers of smart lights, Acuity (NYSE:AYI) designs and manufactures light fixtures and building management systems used in various industries.

Acuity Brands reported revenues of $1.18 billion, up 21.7% year on year. This print topped analysts’ expectations by 3.1%. Overall, it was an exceptional quarter as it also logged a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ adjusted operating income estimates.

The stock is up 17.5% since reporting and currently trades at $337.47.

Read our full, actionable report on Acuity Brands here, it’s free.

Originally a metal-working shop supporting local petrochemical facilities, Powell (NYSE:POWL) has grown from a small Houston manufacturer to a global provider of electrical systems.

Powell reported revenues of $286.3 million, flat year on year. This number came in 5.1% below analysts' expectations. Overall, it was a mixed quarter for the company.

The stock is up 15.6% since reporting and currently trades at $274.50.

Read our full, actionable report on Powell here, it’s free.

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jun-25 | |

| Jun-25 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-17 | |

| Jun-10 | |

| May-01 | |

| Apr-29 | |

| Mar-18 | |

| Mar-09 | |

| Mar-07 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite