|

|

|

|

|||||

|

|

|

Over the last six months, IDEX’s shares have sunk to $164.17, producing a disappointing 11.8% loss - a stark contrast to the S&P 500’s 15.7% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in IDEX, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons there are better opportunities than IEX and a stock we'd rather own.

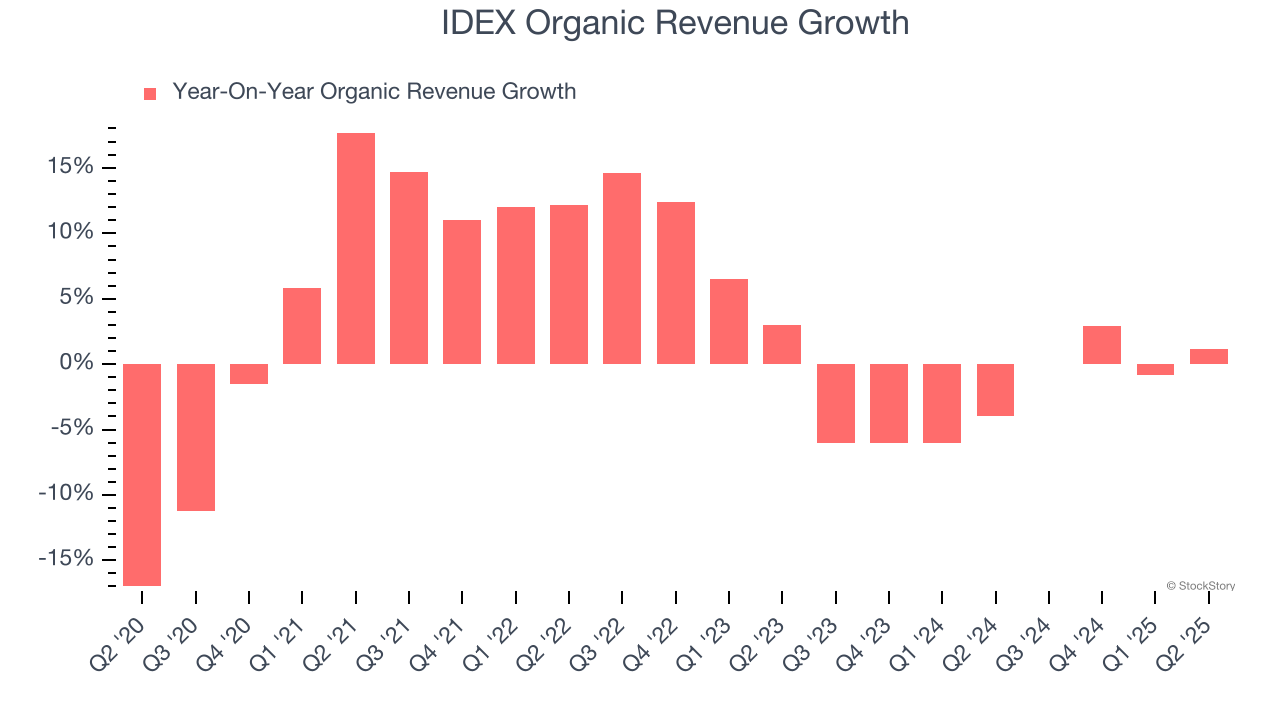

Investors interested in Gas and Liquid Handling companies should track organic revenue in addition to reported revenue. This metric gives visibility into IDEX’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, IDEX’s organic revenue averaged 2.3% year-on-year declines. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests IDEX might have to lean into acquisitions to grow, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

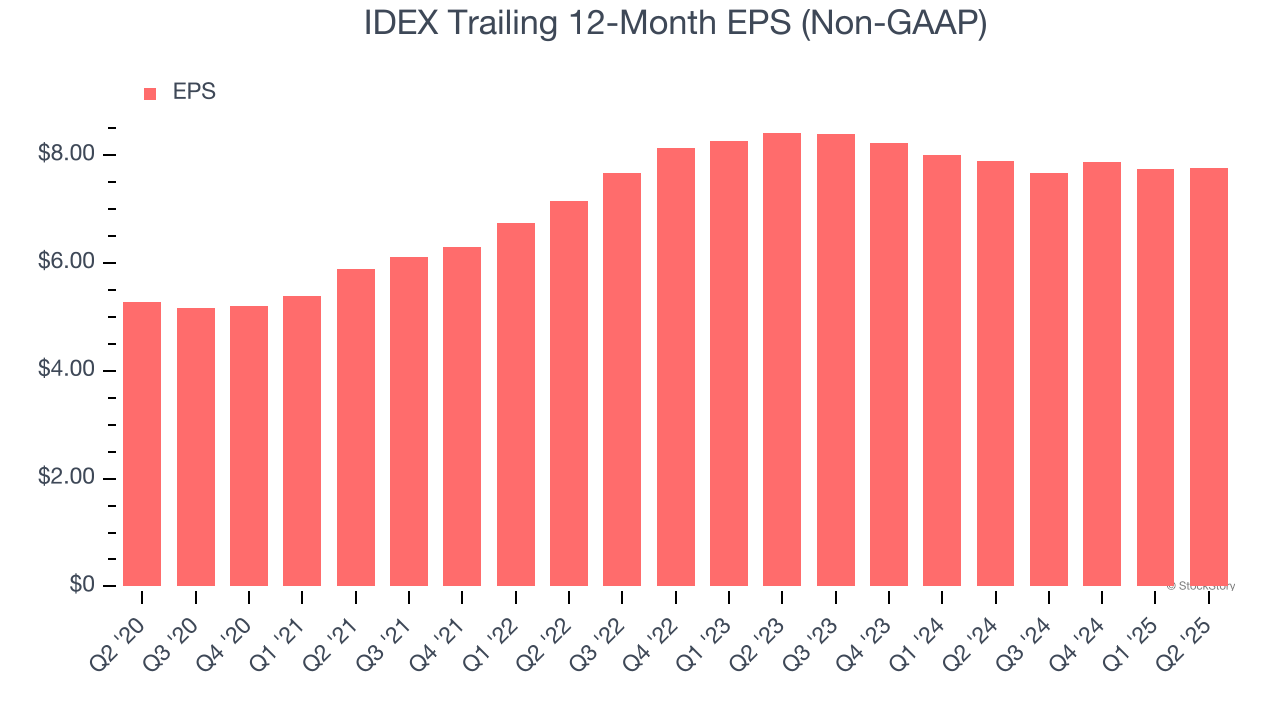

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for IDEX, its EPS declined by 4% annually over the last two years while its revenue was flat. This tells us the company struggled to adjust to choppy demand.

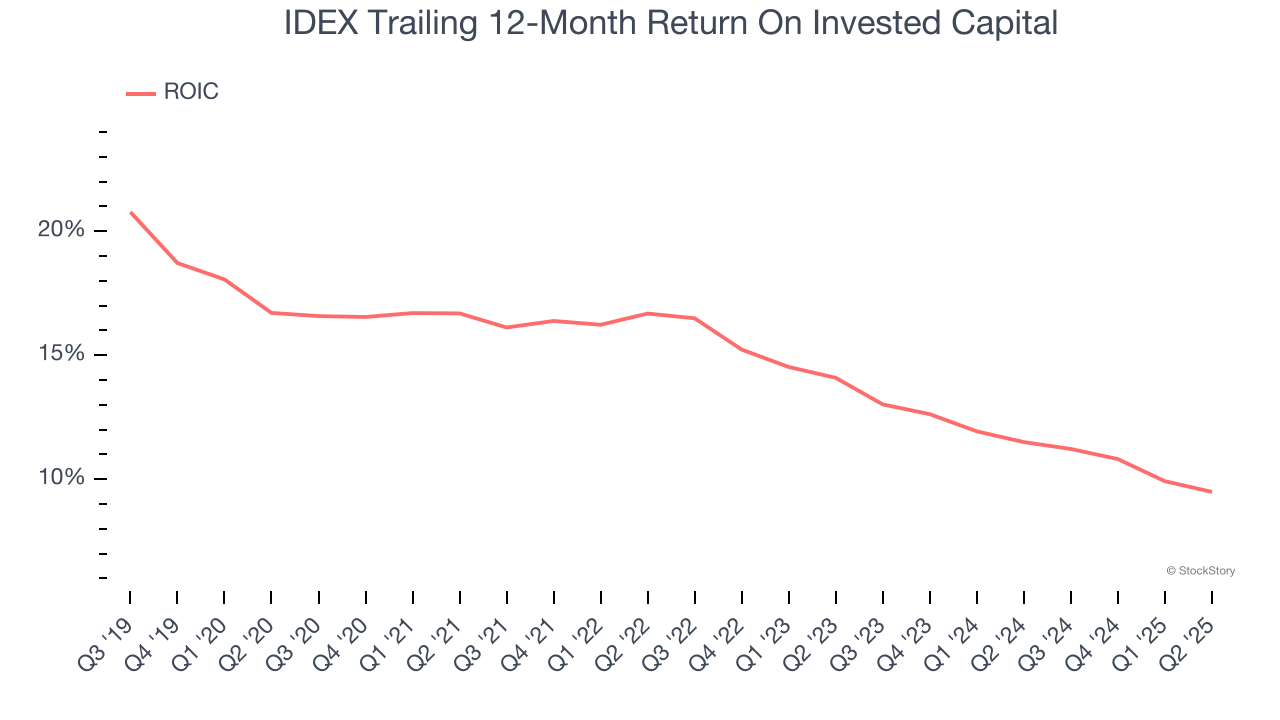

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, IDEX’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

IDEX falls short of our quality standards. After the recent drawdown, the stock trades at 19.2× forward P/E (or $164.17 per share). This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-20 | |

| Jul-06 | |

| Jun-29 | |

| Jun-17 | |

| May-06 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-17 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite