|

|

|

|

|||||

|

|

|

Chewy, Inc. (CHWY) reported second-quarter fiscal 2025 results, wherein both top and bottom lines beat the Zacks Consensus Estimate and increased year over year. Management raised and narrowed its fiscal 2025 net sales outlook.

The company delivered top-line growth that exceeded the high end of the guidance, supported by market share gains and the strong performance of its Autoship program in consumables and health categories.

Chewy posted adjusted earnings of 33 cents per share, which beat the Zacks Consensus Estimate of 14 cents. The figure increased 37.5% from the prior-year period.

Chewy price-consensus-eps-surprise-chart | Chewy Quote

The company reported net sales of $3,104.2 million, surpassing the Zacks Consensus Estimate of $3,082 million. The figure increased 8.6% from $2,858.6 million posted in the year-ago period. This growth was driven by the continued strength of the Autoship program, particularly in consumables and health categories. Autoship customer sales rose nearly 14.9% year over year to a record $2.58 billion, accounting for 83% of total quarterly net sales.

Hardgoods sales grew 15.2% year over year to $346.1 million, supported by structural volume growth. Consumable sales grew 6.6% year over year to $2.15 billion. The Zacks Consensus Estimate was pegged at $328 million for Hardgoods net sales and $2.14 billion for Consumables net sales for the fiscal second quarter.

The company ended the fiscal second quarter with 20.9 million active customers, a 4.5% increase year over year. Chewy’s net sales per active customer reached $591, reflecting a 4.6% year-over-year increase.

Chewy’s gross profit increased 11.7% year over year to $942.2 million. The gross margin increased 90 basis points (bps) to 30.4% compared with 29.5% in the second quarter of fiscal 2024. This expansion was fueled by growth in the sponsored ads business and a stronger mix of premium categories, while pricing and promotional activity remained disciplined and had minimal impact on margins.

SG&A expenses rose 8.2% year over year to $671.9 million in the fiscal second quarter. As a percentage of net sales, SG&A expenses decreased 10 bps year over year to 21.6%. Advertising and marketing expenses for the fiscal second quarter totaled $200.6 million, up 5.3% year over year.

Adjusted EBITDA was $183.3 million, an increase of 26.5% from $144.9 million reported in the year-ago quarter. The adjusted EBITDA margin increased 80 bps year over year to 5.9%.

The company ended the quarter with $591.8 million in cash and cash equivalents, remained debt-free and reported total liquidity of approximately $1.4 billion. Total shareholders’ equity was $389.9 million.

In the fiscal second quarter, the company reported free cash flow of $105.9 million, with $133.9 million in net cash provided by operating activities and $28 million in capital expenditures.

The company repurchased approximately 3 million shares for a total of $125 million. As of the end of the quarter, $359.8 million of repurchase capacity remained available under the current authorization.

For the third quarter of fiscal 2025, Chewy expects net sales to be between $3.07 billion and $3.10 billion, representing year-over-year growth of approximately 7% to 8%. Adjusted earnings per share are anticipated to range from 28 cents to 33 cents.

For fiscal 2025, Chewy now expects net sales to be between $12.5 billion and $12.6 billion, representing approximately 7% to 8% year-over-year growth, excluding the impact of the 53rd week in fiscal 2024. This outlook is up from the previous guidance of $12.3 billion to $12.5 billion, which implied 6% to 7% growth.

The company is maintaining its adjusted EBITDA margin guidance between 5.4% and 5.7%. The midpoint of this range represents approximately 75 basis points of year-over-year expansion. Approximately 60% of this expansion is expected to come from improvements in gross margin.

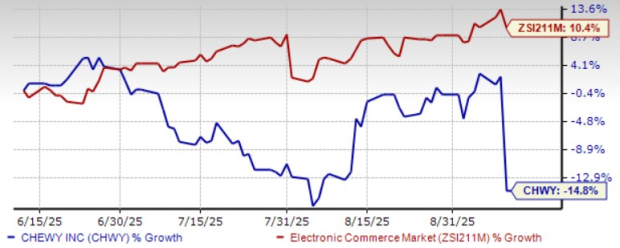

This Zacks Rank #4 (Sell) stock has lost 14.8% in the past three months against the industry’s growth of 10.4%.

Central Garden & Pet (CENT), one of the leading companies in the U.S. pet supplies and lawn and garden supplies space, sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Central Garden & Pet delivered a trailing four-quarter earnings surprise of 209.3%, on average. The Zacks Consensus Estimate for CENT’s current fiscal-year earnings indicates increases of 22%, from the year-ago period’s reported levels.

Petco Health and Wellness Company, Inc. (WOOF) operates as a health and wellness company that focuses on enhancing the lives of pets, pet parents and its Petco partners. It currently flaunts a Zacks Rank #1. WOOF delivered a trailing four-quarter earnings surprise of 170.8%, on average.

The Zacks Consensus Estimate for Petco Health and Wellness Company’s current fiscal-year earnings indicates growth of 237.5%, from the year-ago reported numbers.

Urban Outfitters Inc. (URBN) is a lifestyle specialty retailer that offers fashion apparel and accessories, footwear, home decor and gift products. It currently carries a Zacks Rank #2 (Buy). URBN delivered a trailing four-quarter average earnings surprise of 24.8%.

The Zacks Consensus Estimate for Urban Outfitters’ current fiscal-year earnings and sales implies growth of 26.4% and 9.2%, respectively, from the year-ago actuals.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-16 | |

| Jul-13 | |

| Jun-23 | |

| Jun-14 | |

| Jun-12 | |

| Jun-12 | |

| Jun-11 | |

| Jun-11 | |

| Jun-11 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite