|

|

|

|

|||||

|

|

|

OppFi Inc. OPFI shares have skyrocketed 139.2 % in a year. This outstanding growth exceeds the 14.1% rise of its industry and the 18.4% rally in the Zacks S&P 500 Composite.

OPFI performed better than its industry peers PayPal’s PYPL 6.7% fall and Repay’s RPAY 28% decline.

The year-to-date price performance also shows that OPFI has outperformed PayPal and Repay. While OppFi has gained 33%, PayPal and Repay have lost 23.1% and 25.8%, respectively.

OPFI’s price performance may compel investors to buy the stock. However, we must assess the reasons behind such exponential growth and then conclude whether or not it is fruitful to ride the rally.

OPFI leverages its bank-partner model for its offerings to everyday American users. Using this strategy, the company targets the demographic that comes under the umbrella of the Fair Issac Corporation score range below 650. This population often lacks traditional lending options, thus making OPFI an underserved-friendly company. Banking on this approach, the company expands its market and provides its services to customers who cannot access credit easily.

The company needs to tackle the inherent risks of default. Hence, it has implemented robust AI and machine learning models to screen and serve customers quickly. This solution has not only reduced the risks but also improved the pace of OPFI’s services, evidenced by the loan auto-approval rate of 80% during the June quarter of this year compared with 76% in the previous-year quarter. This mechanism has not only aided customer satisfaction but also contributed to the 2.4% year-over-year decline in OPFI’s operating expenses in the second quarter of 2025.

The company witnessed consistently strong customer satisfaction, evidenced by a Net Promoter Score (NPS) of 79, a testament to its successful customer-centric approach. Management is bullish on its customer-first strategy, thus taking chances on raising its 2025 revenue and adjusted net income guidance. Management expects revenues of $578-$605 million compared with the preceding quarter’s view of $563-$594 million. Adjusted net income is likely to be $125-$130 million compared with the previous quarter’s view of $106-$113 million.

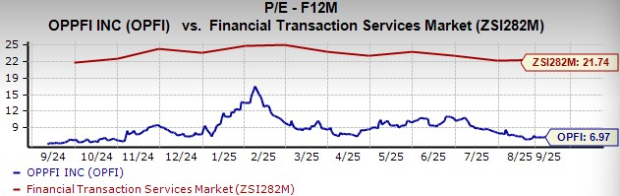

OppFi’s discounted valuation can raise investor attention. The stock is priced at 6.97 times forward 12-month earnings per share, significantly lower than the industry’s average of 21.74 times. The stock looks fairly cheap in terms of the trailing 12-month EV-to-EBITDA ratio, with OPFI trading at 4.56 times, below the industry’s average of 13 times.

In terms of liquidity, OppFi’s current ratio in the second quarter of 2025 was 1.72, improving from the year-ago quarter’s 1.57, facilitated by an increase in accounts receivable. It is also impressive that OPFI’s current ratio outpaces the industry average of 1.17. Furthermore, we expect the company to cover its short-term obligations efficiently as the metric exceeds 1.

The Zacks Consensus Estimate for OPFI’s 2025 revenues is $588.9 million, hinting at 12% year-over-year growth. For 2026, the top line is expected to increase 7%.

The consensus estimate for OPFI’s 2025 earnings per share stands at $1.42, implying a 49.5% year-over-year rise. For 2026, the estimate is pegged at 4.2% growth.

Over the past 60 days, two EPS estimates for 2025 and 2026 have been revised upward with no downward revisions. The Zacks Consensus Estimate for 2025 earnings has risen 15.4%, and the same has grown 5% for 2026. These upward revisions highlight analysts' confidence.

OppFi’s customer-first strategy, led by its bank-partner model, has improved customer-satisfaction level, evidenced by NPS. In doing so, management’s optimism over the company’s long-term growth trajectory has improved. With a strong liquidity position and discounted valuation, this fundamentally strong stock has solidified its position in the market.

Based on its promising growth story, we recommend that investors buy the stock right now. Those interested in testing the waters in the fintech domain should add this stock to their portfolios and ride the rally to reap gains in the long run.

OPFI flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 44 min | |

| 14 hours | |

| 15 hours | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite