|

|

|

|

|||||

|

|

|

Since March 2025, Peoples Bancorp has been in a holding pattern, posting a small return of 1.7% while floating around $30.32. The stock also fell short of the S&P 500’s 15.9% gain during that period.

Is there a buying opportunity in Peoples Bancorp, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

We're swiping left on Peoples Bancorp for now. Here are three reasons why PEBO doesn't excite us and a stock we'd rather own.

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Peoples Bancorp’s net interest income to rise by 1.8%, a deceleration versus its 8.6% annualized growth for the past two years. This projection is below its 8.6% annualized growth rate for the past two years.

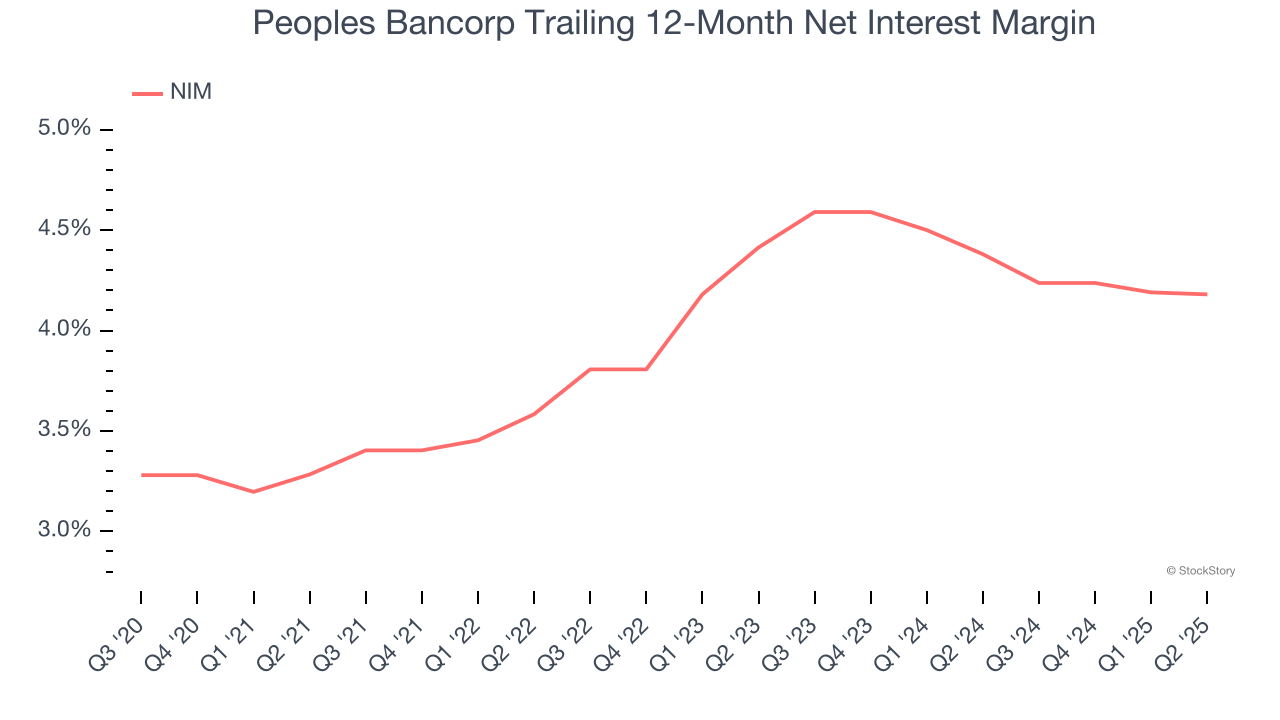

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, Peoples Bancorp’s net interest margin averaged 4.3%. However, its margin contracted by 23.3 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Peoples Bancorp either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

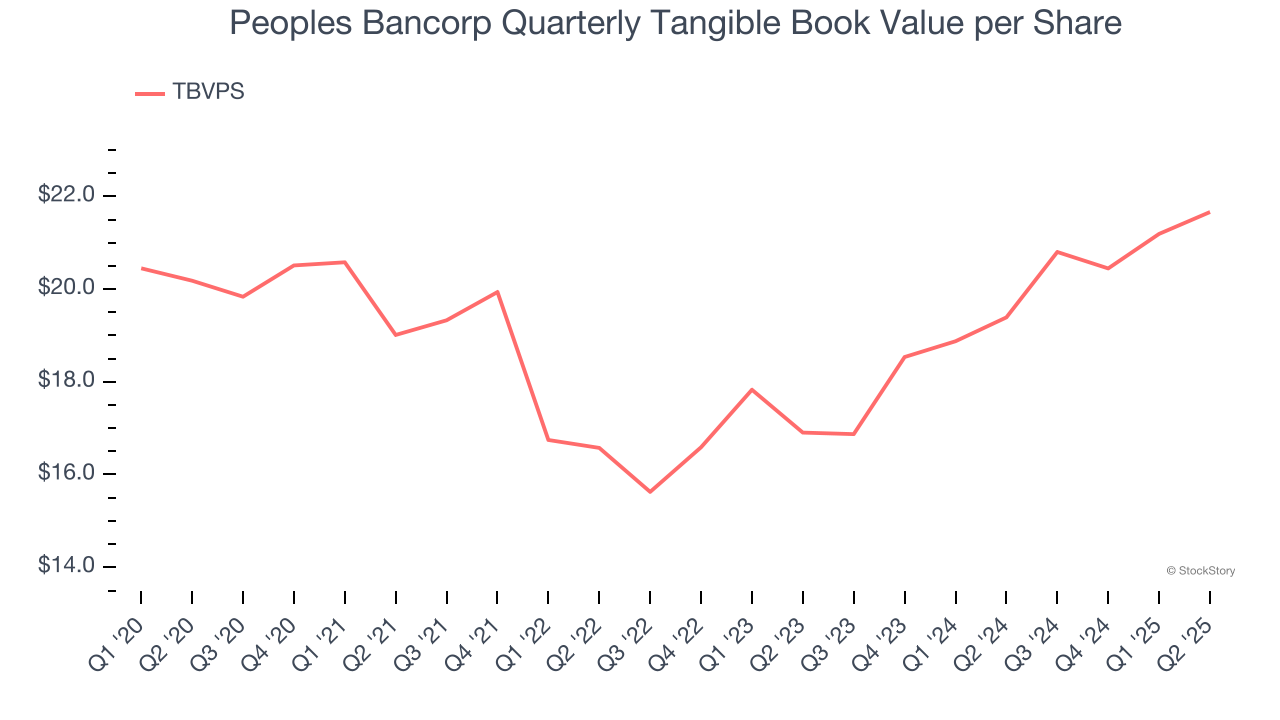

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Although Peoples Bancorp’s TBVPS increased by a meager 1.4% annually over the last five years, the good news is that its growth has recently accelerated as TBVPS grew at a solid 13.2% annual clip over the past two years (from $16.90 to $21.66 per share).

Peoples Bancorp isn’t a terrible business, but it doesn’t pass our bar. With its shares underperforming the market lately, the stock trades at 0.9× forward P/B (or $30.32 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Aug-03 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-15 | |

| Jun-29 | |

| Apr-27 | |

| Apr-22 | |

| Apr-21 | |

| Apr-21 | |

| Apr-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite