|

|

|

|

|||||

|

|

|

AT&T, Inc. T and T-Mobile, US, Inc. TMUS are both dominant players in the telecommunications industry. Operating as one of the largest wireless service providers in North America, AT&T offers a vast array of communication and business solutions that include wireless, local exchange, long-distance, data/broadband and Internet, video, managed networking, wholesale and cloud-based services. T-Mobile, another telecom giant, offers mobile voice, messaging and data services in the postpaid, prepaid and wholesale markets.

Telecom operators are witnessing a surge in data traffic, driven by the growing usage of high data-intensive applications such as cloud, gaming and IoT. The federal initiative of bridging the digital divide in rural and underserved areas in an effort to foster digital inclusivity is also driving growth in the industry. Digital transformation initiatives and the adoption of AI applications by enterprises across industries are also driving growth. However, high capex burden and market saturation remain headwinds.

With deep industry acumen, both AT&T and T-Mobile hold a strong foothold in the highly competitive U.S. telecom sector. Let us analyze the competitive strengths and weaknesses of the companies in depth to understand which is better positioned to maximize gains from the emerging market trends.

AT&T is benefiting from solid wireless traction and customer additions. In the second quarter, the company reported 479,000 post-paid net additions, which include 401,000 postpaid wireless phone additions. Postpaid churn was 1.02%, while postpaid phone-only average revenue per user (ARPU) increased 1.1% year over year to $57.04 due to improved international roaming, pricing actions and a transition to higher-priced unlimited plans.

It is also witnessing healthy traction in the Consumer wireline business. The growth was driven by solid momentum in the fiber broadband business. The company recorded net fiber additions of 243,000, while Internet Air added 203,000 subscribers during the second quarter. The company is steadily expanding its fiber footprint nationwide with a goal of reaching 50 million customer locations by 2030. Its acquisition of Lumen's fiber connectivity business is part of this initiative. However, the company is set to face stiff competition from Verizon Communications, Inc. VZ in this vertical. Verizon is also aggressively expanding its fiber footprint, and its acquisition of Frontier Communications has significantly boosted its fiber broadband portfolio.

Growing competition in a highly saturated U.S. wireless market is weighing on margins. Amid growing competition, greater network capacity, coverage and performance are key factors to drive customer retention and growth in average revenue per user. The company is set to acquire wireless spectrum licenses from EchoStar. The acquisition of EchoStar’s spectrum assets will expand AT&T’s presence across 400 markets across the United States. It is expected to boost the company’s 5G capabilities and close the competitive gap with Verizon and T-Mobile. However, such strategic acquisitions, combined with network densification and expansion initiatives, are leading to a greater capex burden, limiting free cash flow growth to some extent.

T-Mobile continues to boast a leadership position in the 5G market. The company’s 5G network covers 98% of Americans, or 330 million people, in the country. It continues to deploy 5G with the mid-band 2.5 GHz spectrum from Sprint. The 2.5 GHz 5G delivers superfast speeds and extensive coverage with signals that go through walls and trees, unlike 5G networks that are controlled by the mmWave spectrum. This gives the un-carrier a competitive edge over AT&T and Verizon.

The company is benefiting from industry-leading postpaid customer growth. During the second quarter, T-Mobile added 1.7 million postpaid net customers and 318,000 postpaid net accounts. Postpaid phone net customer additions were 830,000. The postpaid phone churn rate was 0.9%. 5G broadband net customer additions were 454,000. Postpaid average revenues per account rose to $149.87 from $142.54 in the year-ago quarter.

The company recently completed the acquisition of US Cellular’s wireless operations. The acquisition has enabled TMUS to expand both its fast-growing home broadband offerings and fixed wireless products through the additional capacity and coverage from the combined spectrum and wireless assets.

T-Mobile has been selected as the official telecommunication service provider for the Los Angeles 2028 Olympics and Paralympic Games. This underscores the growing recognition of TMUS’ industry-leading 5G portfolio for advanced use cases.

However, the company faces intense competition in the telecom market from major companies like AT&T and Verizon. Growing competition with a relatively fixed pool of customers is putting pressure on pricing. To lure customers from competitors, T-Mobile has launched several low-priced service plans for consumers as well as small business entities. Such a strategy is also straining the margin. From a valuation standpoint, T-Mobile appears to be trading at a premium relative to the industry. Owing to the stock’s premium valuation, we believe investors should remain cautious as macroeconomic factors can significantly impact overvalued stocks like TMUS.

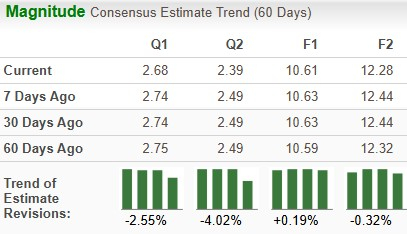

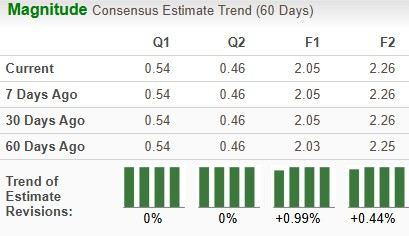

The Zacks Consensus Estimate for T-Mobile’s 2025 sales and EPS implies year-over-year growth of 6.48% and 9.83%, respectively. The EPS estimate for 2025 has improved 0.19% over the past 60 days, while for 2026 it declined 0.32%.

The Zacks Consensus Estimate for AT&T’s 2025 sales indicates growth of 2.16% year over year, while EPS is projected to decline 9.29%. The EPS estimates for 2025 and 2026 have been trending northward over the past 60 days.

Over the past year, T-Mobile has gained 17.4% compared with the industry’s growth of 13%. T has gained 32.8% over the same period.

Going by the price/earnings ratio, T-Mobile’s shares currently trade at 20.50 forward earnings, higher than 13.59 for the industry. AT&T shares currently trade at 13.47 forward earnings.

Both AT&T and T-Mobile carry a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both AT&T and T-Mobile are taking several initiatives to gain a firmer footing in the U.S. telecom sector. T-Mobile’s strong customer engagement in the 5G portfolio is a positive. However, its premium valuation remains a concern. Uptrend in estimate revision in 2025 and downward revision in 2026 showcased mixed investor perception regarding its growth potential. AT&T’s strong foothold in the wireless market, focus on lowering operating costs and improving efficiency are positive factors. Strong focus on fiber expansion and improving 5G capabilities through strategic acquisition is expected to bring long-term benefits. Better price performance over the past year and attractive valuation are positives. Owing to these factors, T appears to be a better investment option at the moment.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 24 min | |

| 24 min | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Elon Musk Wants Starlink To Take On T-Mobile, Verizon, AT&THere's Why That's Easier Said Than Done

TMUS T VZ

Benzinga Prediction Markets

|

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite