|

|

|

|

|||||

|

|

|

JD.com's JD core retail business is powering ahead, reaffirming its role as the company’s key growth engine. JD Retail's revenues rose 20.6% year over year to RMB 310.1 billion, contributing the bulk of the total company's revenues. Profitability also improved, with operating margin rising to 4.5% from 3.9%, its best sequential performance. Broad-based category strength underpinned this growth: electronics and home appliances gained 23%, general merchandise advanced 16% year over year and supermarkets delivered a sixth straight quarter of double-digit gains.

Behind this momentum is JD’s supply chain strength. Investments in automation, logistics efficiency and fulfillment upgrades are driving scale and profitability. Active customer counts and shopping frequency jumped more than 40% yearly, reflecting stronger retention and cross-category purchases. Promotional events like the 618 Festival, paired with differentiated supermarket offerings, continue to boost both engagement and supplier partnerships.

JD is also investing in future growth. Its “One Step Ahead” upgrade program supports 3C manufacturers and promotes emerging categories like AI glasses and intelligent robots. Meanwhile, JD MALL has expanded to 24 stores, combining offline retail with digital experiences to strengthen omnichannel reach. These steps help the company stay flexible with consumer needs while boosting its brand.

The Zacks Consensus Estimate projects JD.com’s revenue growth of 14.04% in 2025 and 5.15% in 2026. This outlook is further reinforced by Grand View Research, which forecasts China’s smart retail market to expand at a robust 31.9% compound annual growth rate through 2033 — pointing to a critical long-term growth driver for JD.

Still, challenges persist. Intense competition, rising marketing expenses and heavy investments in non-retail ventures remain a drag on margins.

Sea Limited’s SE e-commerce platform Shopee is expanding rapidly, with second-quarter 2025 e-commerce revenues up 33.7% year over year and GMV (Gross Merchandise Value) rising 28%. SE’s marketplace model avoids heavy inventory costs, offering scalability and flexibility versus JD’s asset-heavy logistics. With strengths in fintech and gaming, SE drives cross-platform synergies while maintaining e-commerce leadership in Asia and Brazil. Though JD excels in logistics and quality control, SE’s faster growth in emerging markets makes it a formidable retail competitor.

Alibaba BABA is JD.com’s toughest rival in China’s retail segment, leveraging its massive scale, Taobao/Tmall dominance and marketplace model. Alibaba benefits from lower inventory costs, wider merchant reach and strong international platforms like Lazada, AliExpress and Trendyol. With over half of China’s online retail sales and Taobao driving 80% of revenues, Alibaba maintains superior margin flexibility and cross-business synergies. While JD excels in logistics and authenticity, Alibaba’s diversified ecosystem and faster scalability secure its retail edge.

Shares of JD.com have declined 2.9% year to date against the Zacks Internet - Commerce industry’s return of 12.5%.

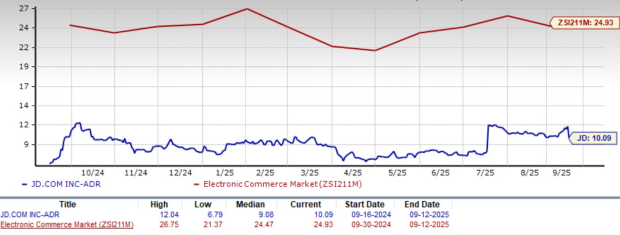

From a valuation standpoint, JD.com is trading at a forward 12-month price-to-earnings ratio of 10.09X, lower than the industry’s 24.93X. JD carries a Value Score of A.

The Zacks Consensus Estimate for JD’s full-year 2025 revenues is pegged at $183.33 billion, indicating 14.04% year-over-year growth. The consensus mark for 2025 earnings is pegged at $2.68 per share, which increased 7.6% over the past 30 days. The earnings figure suggests a 37.09% decline over the figure reported in 2024.

JD.com currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 hours | |

| 9 hours | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite