|

|

|

|

|||||

|

|

|

Eaton is a large and diversified industrial company focused on power management.

The company has been making corporate moves to hone its focus on electricity.

Eaton is well-positioned for an increasingly electric future, but Wall Street seems well aware of that fact.

I bought Eaton (NYSE: ETN) while it was still working on integrating its acquisition of Cooper Industries. That was the largest deal in the company's history and materially shifted the industrial giant's business focus. Now, more than a decade after that transformational deal, is Eaton worth buying?

The $13 billion acquisition of Cooper in late 2012 was huge for Eaton. Not just in what it did for the business, but simply in the scale of the transaction. It required years of effort to fully integrate Cooper into Eaton. And, while Eaton was working on that effort, the Board of Directors chose to hold the dividend static for a spell after a long history of regular dividend increases.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

I bought Eaton during that period because I believed the strategic benefit of buying Cooper would allow the company to, eventually, start growing the dividend again. That came to pass, with Eaton's dividend back in growth mode. The industrial giant's most recent dividend increase, made in March 2025, was a hefty 11%.

The company is performing very well, as you might expect from that sizable dividend hike. In the second quarter of 2025, Eaton had record earnings, with adjusted earnings rising 8% year over year. It had record segment margins, at 23.9%. And it posted solid organic sales growth of 8%. Buying Cooper and jettisoning some less desirable operations thereafter have clearly worked out well for the company and investors who were willing to step in while Eaton was unloved.

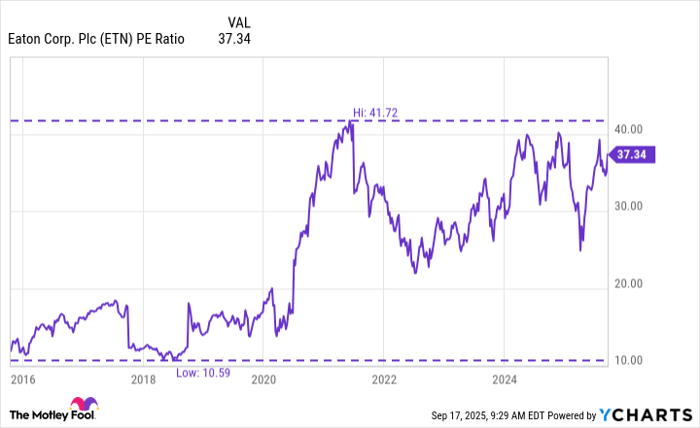

Data by YCharts.

Don't hit the buy button just yet, though. Back when I bought Eaton, the mood around the stock was dour at best. Today, given the business performance, the stock is well-loved. To put some numbers on that, the price-to-earnings ratio has gone from around 10.5x when I bought Eaton to roughly 37x today. That puts the valuation far closer to the peak level of nearly 42x over that span than the low end, where I bought it.

Then there's the dividend yield, which is a tiny 1.1% today. That's lower than the roughly 1.3% yield of the average industrial stock. It is even lower than the 1.2% yield of the average stock in the S&P 500 (SNPINDEX: ^GSPC). At first glance, the yield comparison here would suggest that Eaton isn't materially out of line with the market's valuation. That's actually true. The problem is that the S&P 500 index itself looks expensive right now, with a lofty P/E ratio of nearly 28x, and it is trading near all-time highs.

I would not likely buy Eaton today given the stock's valuation. That said, I tend to follow along with Warren Buffett's investment approach of buying and holding good companies so you can benefit from their growth over time. Thus, I have no intention of selling Eaton. And while I recognize that the price tag being placed on Eaton today is high, I'm happily letting the dividend reinvest. This simple approach isn't ideal from a valuation perspective, but it allows me to compound my investment in this strongly performing business without having to think about it.

Eaton is a situation in which the words of Buffett mentor Benjamin Graham are important to remember. Graham, a value investor, noted that even a great business can be a bad investment if you pay too much for it. I didn't pay too much when I bought Eaton, but if you buy it today, it looks like you are at risk of turning a great business into a bad investment. Be patient and put Eaton on your wish list; there's likely to be a drawdown sooner or later that will bring the valuation back to more attractive levels.

Before you buy stock in Eaton Plc, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Eaton Plc wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $651,345!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,080,327!*

Now, it’s worth noting Stock Advisor’s total average return is 1,058% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 15, 2025

Reuben Gregg Brewer has positions in Eaton Plc. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

| Feb-15 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite